/NVIDIA%20Corp%20logo%20on%20phone-by%20Evolf%20via%20Shutterstock.jpg)

Even beyond the AI industry, Nvidia (NVDA) has become a bellwether for the market itself in recent times. Based in Santa Clara, California, both the chip major's every move and every statement from management become analyzed by hawk-eyed market participants looking to get an inkling of the health of the overall market as well as where it is headed next.

As Nvidia gets ready to host its upcoming flagship GPU Technology Conference (GTC), the excitement is unsurprisingly palpable. Expectations, speculations, and opinions are widespread as the date of the event approaches. One such opinion comes from Jeff Pu of Chinese brokerage firm GF Securities.

What Does Analyst Jeff Pu Think About Nvidia?

Sounding optimistic about Nvidia and its next conference, Pu noted to clients that the “NVDA share price has underperformed [the PHLX Semiconductor Index ($SOX)] since Nov-2025. Nevertheless, we stay long on the stock, driven by strong near-term quarters, intact Rubin/VR200 progress and improving financial outlook for non-tier-1 CSPs such as OpenAI." The analyst continued, "Additionally, we expect NVDA to launch [an] LPU (language processing unit) in the coming GTC event to strengthen its product portfolio in inferencing and also CPO for scale-out switches and scale-up (50/50 chance).”

“We expect a continued strong demand for Blackwell, resilient H200 and a small volume of Rubin," Pu commented further. "We expect Nvidia to hold Apr-Q [gross margin] of mid-70s, backed by the pass-through of higher memory cost.”

Pu reiterated a “Buy” rating on NVDA stock, while raising his price target to $295. That target indicates potential upside of 50% from current levels.

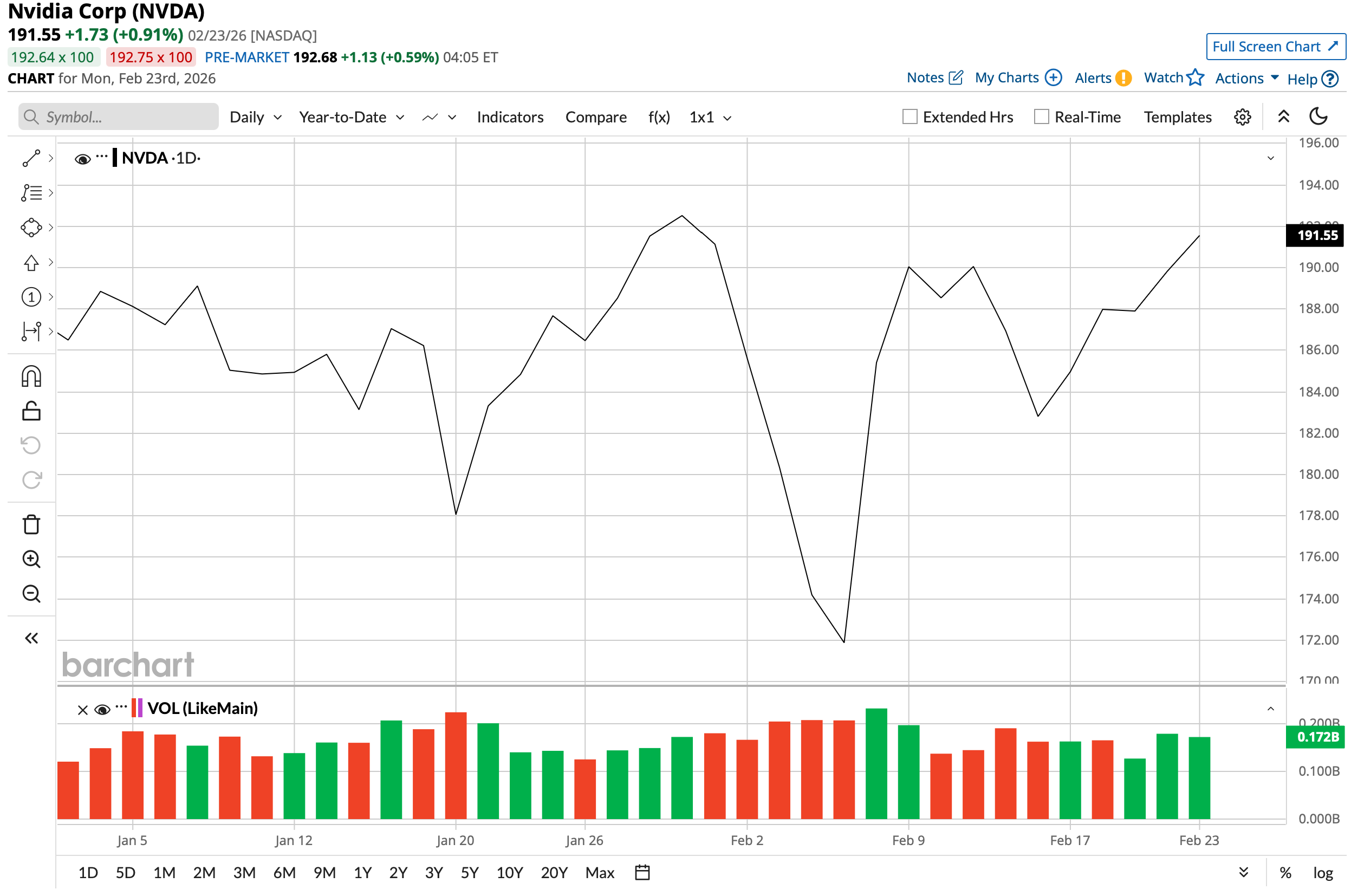

Still, shares of the world's most valuable company in terms of market capitalization ($4.68 trillion) are up a mere 5% on a year-to-date (YTD) basis. That's a far cry from Nvidia's multibagger days when doubling of the stock was a somewhat normal phenomenon.

Can Nvidia regain its mojo, and will the next GTC be a primary driver? Let's take a closer look.

A Look at the Next GTC

Before delving into what the upcoming event may have in store, a glance at Nvidia's last GTC may better set up the context.

The last major GTC was held in 2025 from Oct. 27 to Oct. 29 in Washington, D.C. The most consequential announcement for shareholders was the unveiling of the Blackwell Ultra GPU and the next-generation Rubin architecture. Blackwell Ultra offers a 50% increase in high-bandwidth memory, specifically designed to handle complex reasoning models like DeepSeek. For investors, the "Rubin" roadmap was even more significant, as it confirmed a shift to an annual product release cycle and introduced HBM4 memory integration. These developments solidify Nvidia's moat by providing a clear multi-year growth trajectory, effectively de-risking the stock from fears of a slowed demand scenario after the Hopper series.

Shifting focus to the next GTC to be held in San Jose, California from March 16 to March 19, investors are awaiting more clarity on some specific aspects. Heading into the conference, investor focus has shifted from raw hardware specs to the monetization of "Agentic AI" and the operationalization of AI Factories. The primary catalyst is the expected full-scale launch of the Vera Rubin architecture, which analysts anticipate will utilize HBM4 memory and a 3-nanometer process to deliver a generational leap in inference efficiency.

Management is also likely to emphasize the integration of Groq’s low-latency SRAM IP, a strategic move aimed at cementing Nvidia's dominance in the rapidly growing "reasoning" market. Additionally, significant updates on Physical AI and the Omniverse platform are expected, as the company pivots toward autonomous industrial systems.

Lastly, for shareholders, the key deliverable will be a robust 2026 to 2027 sales outlook that justifies current valuations. If Nvidia successfully demonstrates that its full-stack software moat can maintain mid-70% gross margins despite rising competition, it should provide a fresh tailwind for NVDA stock's next leg higher.

Nvidia's Exceptional Financials

Nvidia delivered yet another strong quarter for the third quarter of fiscal 2026, easily topping both revenue and earnings forecasts while keeping year-over-year (YOY) growth comfortably above 50% on the major lines. While sales reached $57 billion, a 62% jump from the same quarter last year, EPS rose 60% to $1.30, beating the $1.26 consensus estimate. The data center business, clearly the main driver, grew 66% to $51.2 billion.

Cash flow stayed very healthy as well. Operating cash flow climbed to $23.8 billion from $17.6 billion a year earlier, and free cash flow increased by 64% in the same period to $22.1 billion. The company closed the quarter with $60.6 billion in cash, short-term debt under $1 billion, and long-term debt at $7.5 billion, implying that cash was more than eight times the long-term debt amount.

Remarkably, the company has now beaten Street earnings expectations for nine quarters in a row, but the longer-term record is even more striking. Over the past decade, revenue and earnings have compounded at annual rates of 44% and 66%, respectively.

For the December quarter, guidance is set for revenue between $63.7 billion and $66.3 billion, with the Street currently looking for $65.6 billion. Analysts expect EPS at $1.45 and gross margins near 75%. The company is set to report its quarterly results on Feb. 25 after the bell.

What Do Analysts Think About NVDA Stock?

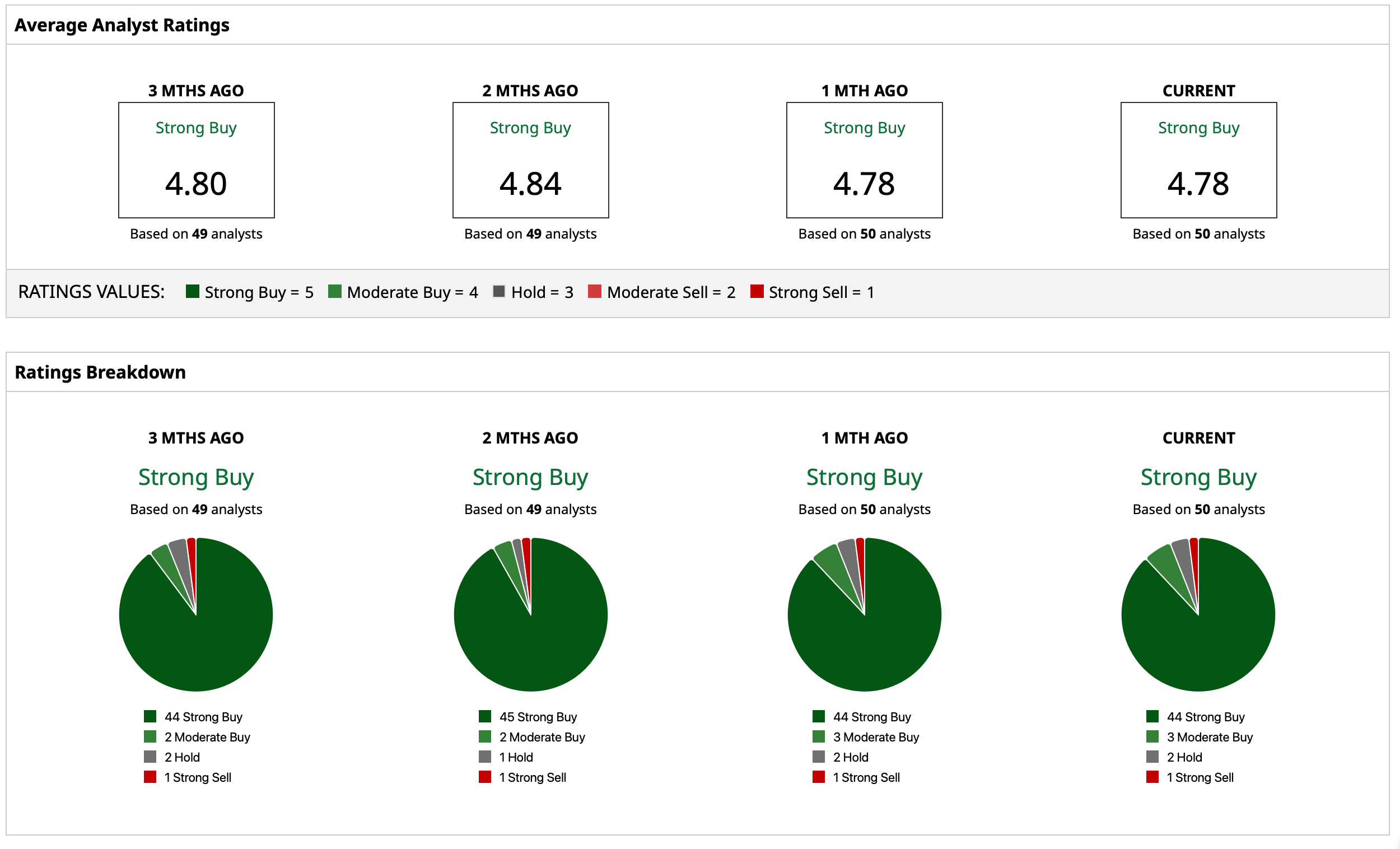

Overall, analysts give NVDA stock a “Strong Buy" consensus rating, with a mean target price of $255.55. This target indicates that the stock still has potential upside of about 30% from current levels. Out of the 50 analysts covering NVDA, 44 have a “Strong Buy” rating, three have a “Moderate Buy” rating, two have a “Hold” rating, and one has a “Strong Sell” rating.

On the date of publication, Pathikrit Bose did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/AI%20(artificial%20intelligence)/AI%20engineer%20working%20on%20laptop%20by%20ART%20STOCK%20CREATIVE%20via%20Shutterstock.jpg)

/A%20corporate%20office%20for%20IBM%20by%20HJBC%20via%20Adobe%20Stock.jpeg)