Identity and access management company Okta (OKTA) dropped 6.4% intraday on Feb. 23, after a 9.2% drop on Feb. 20, after artificial intelligence (AI) firm Anthropic released a new security tool for its Claude model. The AI lab stated that the service can analyze software code for security flaws and recommend fixes.

Software companies have come under fire, with fears of a “software apocalypse,” as AI threatens to replace their usage. With the stock down 20% this year, can Okta emerge triumphant from this storm?

About Okta Stock

Headquartered in San Francisco, California, Okta operates as a leading identity and access management company. It delivers a cloud-based platform that securely connects people to technology through core services like single sign-on, multi-factor authentication, and user lifecycle management.

As a SaaS provider, Okta serves both workforce and customer identity needs, acting as a neutral hub that integrates with thousands of applications to enable seamless access control across cloud, on-premises, and hybrid environments. From its global base, the company supports operations worldwide, enabling secure digital experiences for organizations everywhere. The company has a market capitalization of $12.6 billion.

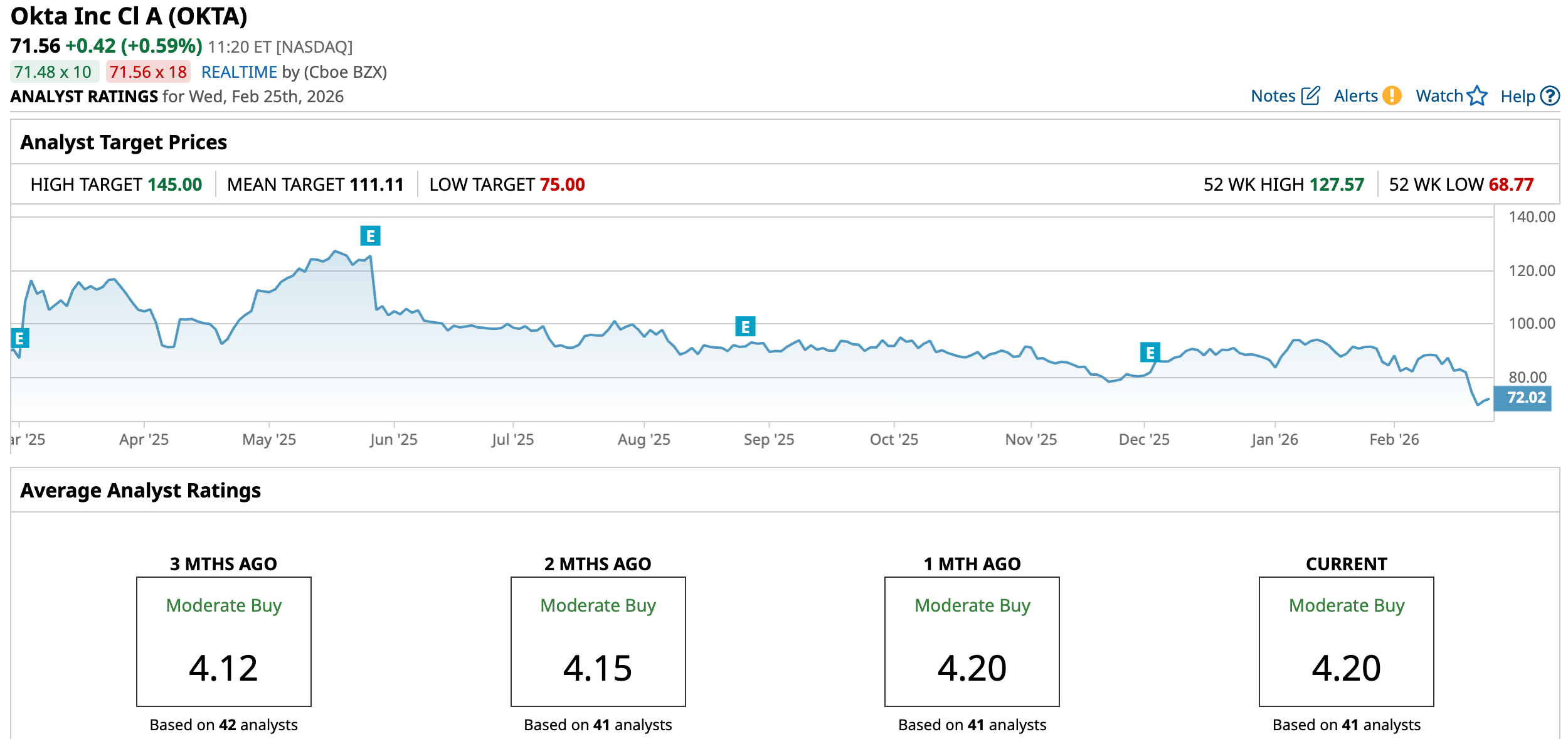

Growth deceleration has raised investor concerns, with slower subscription expansion and subdued current remaining performance obligation (cRPO) guidance. Over the past 52 weeks, Okta’s stock has declined by 19.66%, while it is down 16.99% year-to-date (YTD). It reached a 52-week low of $68.77 on Feb. 23 on AI fears, but is up 4.73% from that level.

On a forward-adjusted basis, Okta’s price-to-earnings ratio of 20.67x is lower than the industry average of 22.41x. Its 14-day RSI stands at 31.77, indicating that it is approaching oversold territory.

Okta Topped Q3 Expectations with Strong Revenue and Profit Gains

Okta reported better-than-expected third-quarter results for fiscal 2026 (quarter ended Oct. 31, 2025). The company’s subscription revenue increased 11.2% year-over-year (YOY) to $724 million, leading to a 11.6% increase in total revenue to $742 million. This figure was also higher than the $730 million that Wall Street analysts had expected.

By the third quarter, customers with an annual contract value exceeding $100,000 had exceeded 5,000. Its cRPO grew by 13% YOY, which is important because it is highly correlated with future subscription revenue. However, Okta’s trailing-12-month dollar-based net retention rate is declining, although it remains at 106% as of Q3.

The double-digit top line growth has also translated into bottom line gains. Okta’s non-GAAP operating margin grew from 21% to 24% annually. Its non-GAAP EPS was $0.82, up 22.4% YOY and above the $0.75 analysts had expected.

Wall Street analysts are optimistic about Okta’s future earnings. They expect the company’s EPS to climb 16% YOY to $0.29 in the fourth quarter of fiscal 2026 (to be reported on Mar. 4, after the market closes). For fiscal 2026, EPS is projected to surge 210% annually to $1.24, followed by a 16.9% growth to $1.45 in fiscal 2027.

What Do Analysts Think About Okta Stock?

Okta has recently received reaffirmations of ratings, as well as price target changes. This month, analysts at Mizuho maintained an “Outperform” rating on the stock but lowered the price target from $110 to $100, citing the multiple compression in the sector. The analysts see some “uncommonly attractive investments in software” for investors willing to be patient, despite the bearish sentiments surrounding the sector.

On the same day, Truist analyst Junaid Siddiqui kept a “Buy” rating on Okta but lowered the firm’s price target from $125 to $115, as part of Truist’s broader view on the software sector. There is likely to be a demarcation between the companies that will survive the AI storm and those at risk. Sharing the same sentiment, Keybanc analyst Eric Heath maintained an “Overweight” rating while lowering the price target from $130 to $115.

A little bit more on the bullish side, last month, analysts at Stephens upgraded the stock from “Equal Weight” to “Overweight,” while raising the price target from $97 to $120. The research firm highlighted a favorable growth outlook for identity security, fueled by enduring trends such as AI and cloud adoption, which are elevating identity as a key strategic focus and signaling a greater confidence in Okta's growth inflection.

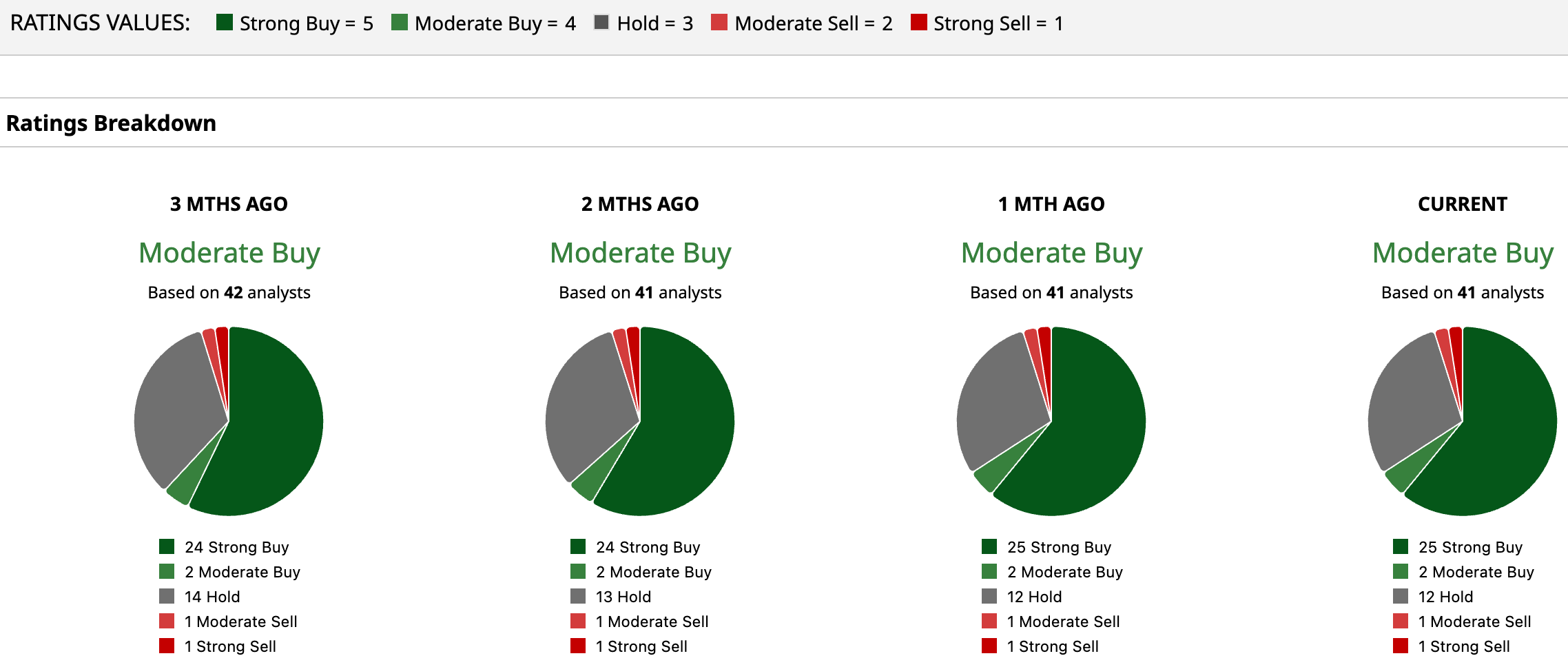

Okta is still favored on Wall Street, with analysts awarding it a consensus “Moderate Buy” rating overall. Of the 41 analysts rating the stock, a majority of 25 analysts have rated it a “Strong Buy,” two analysts suggest a “Moderate Buy,” while 12 analysts are playing it safe with a “Hold” rating, one analyst gave a “Moderate Sell,” and one analyst suggests “Strong Sell.” The consensus price target of $111.65 represents 55.3% upside from current levels. Moreover, the Street-high price target of $145 indicates a 102.6% upside.

Key Takeaways

While the dip in software names has concerned the market, it’s unlikely that software usage will disappear. In fact, about the threat that Anthropic’s new tool poses to cybersecurity firms, Bank of America analysts believe that AI can enhance efficiency in targeted workflows, such as code scanning. But it currently lacks the necessary visibility, control, and reliability to supplant comprehensive end-to-end security platforms. Although there’s an expectation of a slight slowdown, Okta’s fundamentals do not necessarily show signs of immediate alarm. Therefore, the stock might still be worth watching.

On the date of publication, Anushka Dutta did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20close-up%20of%20an%20AMD%20office%20by%20gehapromo%20via%20Adobe%20Stock.jpeg)