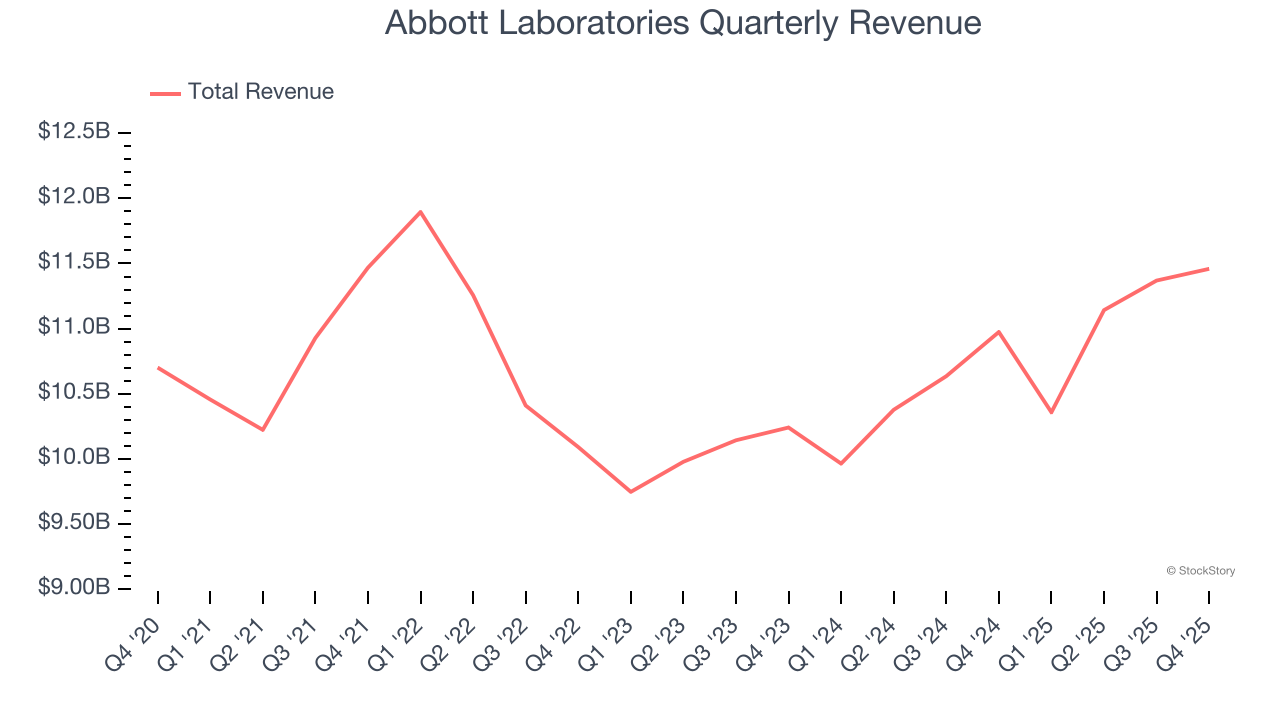

Healthcare product and device company Abbott Laboratories (NYSE:ABT) fell short of the markets revenue expectations in Q4 CY2025 as sales rose 4.4% year on year to $11.46 billion. Its non-GAAP profit of $1.50 per share was in line with analysts’ consensus estimates.

Is now the time to buy Abbott Laboratories? Find out by accessing our full research report, it’s free.

Abbott Laboratories (ABT) Q4 CY2025 Highlights:

- Revenue: $11.46 billion vs analyst estimates of $11.8 billion (4.4% year-on-year growth, 2.9% miss)

- Adjusted EPS: $1.50 vs analyst estimates of $1.49 (in line)

- Adjusted EPS guidance for the upcoming financial year 2026 is $5.68 at the midpoint, in line with analyst estimates

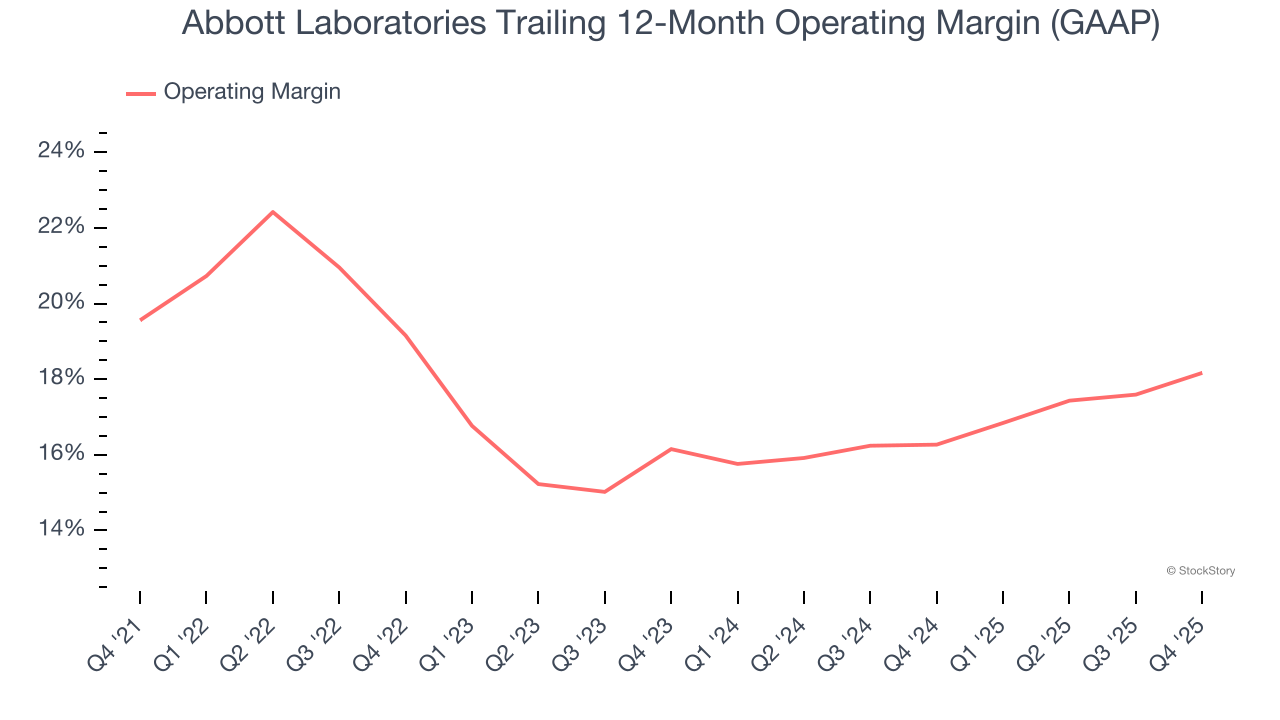

- Operating Margin: 19.6%, up from 17.4% in the same quarter last year

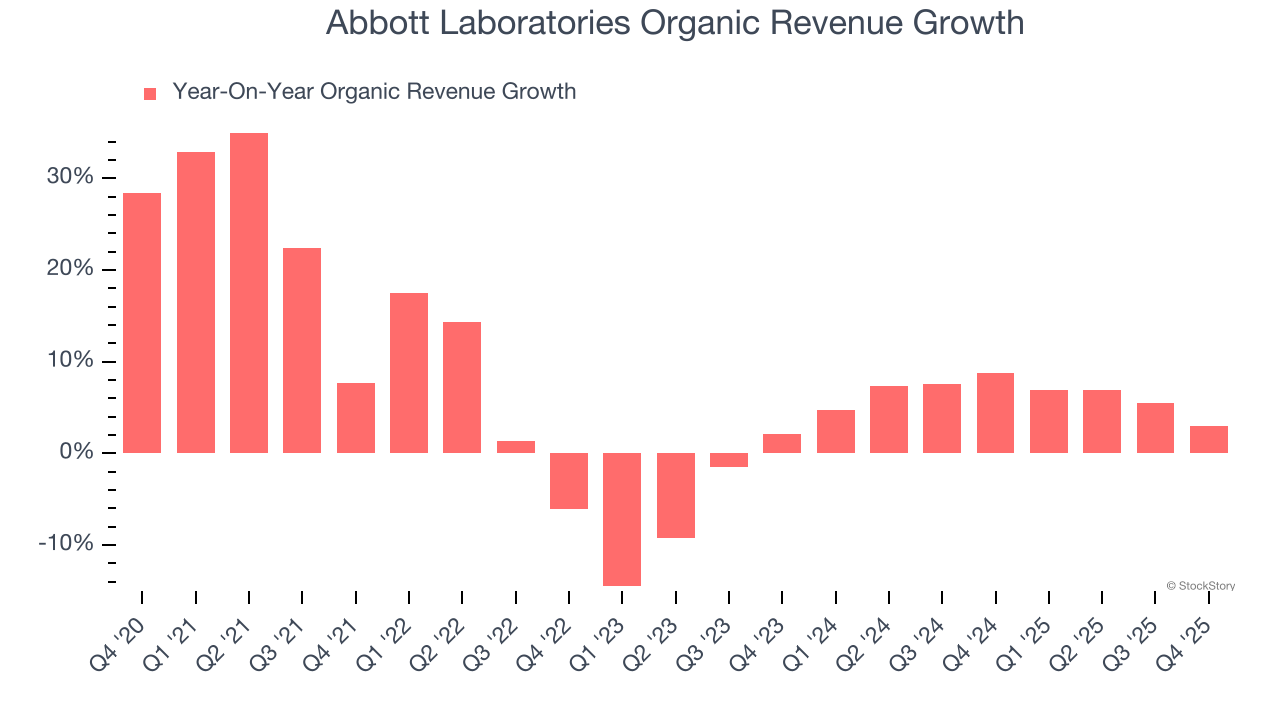

- Organic Revenue rose 3% year on year (miss)

- Market Capitalization: $209.9 billion

"In 2025, we expanded margins and achieved double-digit earnings per share growth, our new product pipeline was highly productive, and we took important strategic steps to shape the company for the future," said Robert B. Ford, chairman and chief executive officer, Abbott.

Company Overview

With roots dating back to 1888 when founder Dr. Wallace Abbott began producing precise, dosage-form medications, Abbott Laboratories (NYSE:ABT) develops and sells a diverse range of healthcare products including medical devices, diagnostics, nutrition products, and branded generic pharmaceuticals.

Revenue Growth

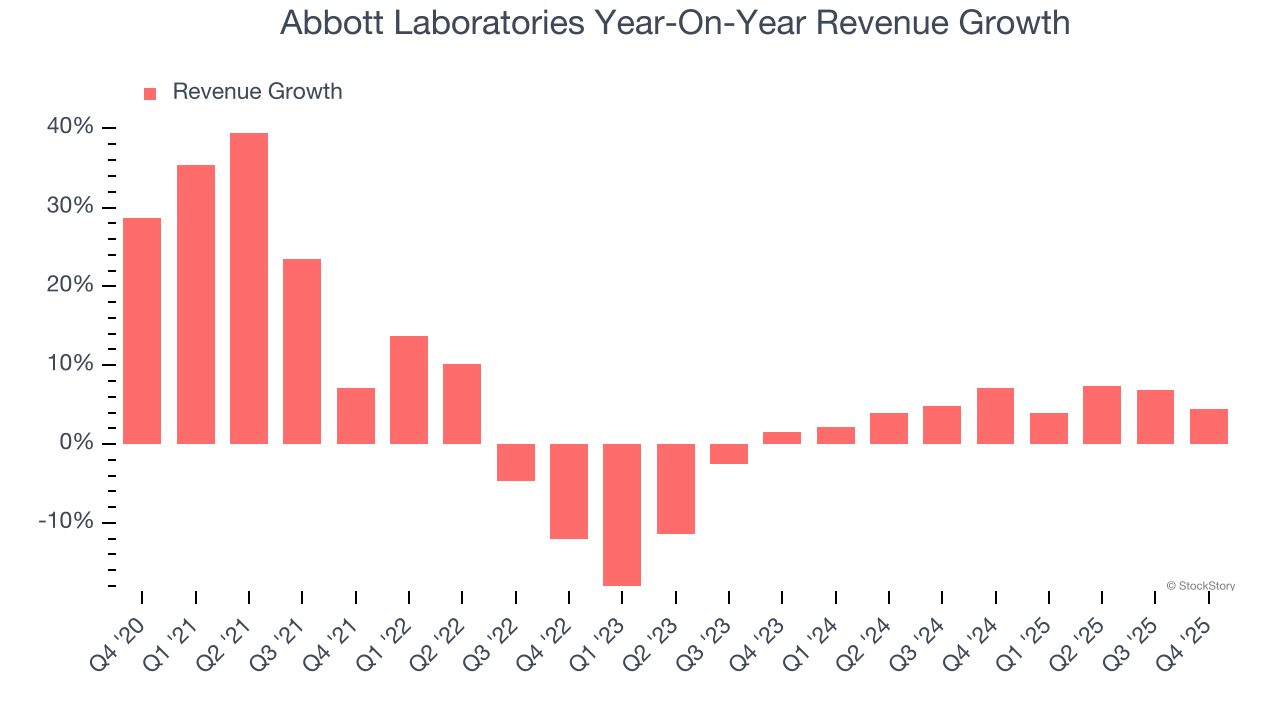

A company’s long-term performance is an indicator of its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Regrettably, Abbott Laboratories’s sales grew at a mediocre 5.1% compounded annual growth rate over the last five years. This wasn’t a great result compared to the rest of the healthcare sector, but there are still things to like about Abbott Laboratories.

Long-term growth is the most important, but within healthcare, a half-decade historical view may miss new innovations or demand cycles. Abbott Laboratories’s annualized revenue growth of 5.1% over the last two years aligns with its five-year trend, suggesting its demand was consistently weak.

We can dig further into the company’s sales dynamics by analyzing its organic revenue, which strips out one-time events like acquisitions and currency fluctuations that don’t accurately reflect its fundamentals. Over the last two years, Abbott Laboratories’s organic revenue averaged 6.4% year-on-year growth. Because this number aligns with its two-year revenue growth, we can see the company’s core operations (not acquisitions and divestitures) drove most of its results.

This quarter, Abbott Laboratories’s revenue grew by 4.4% year on year to $11.46 billion, falling short of Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 8.8% over the next 12 months, an improvement versus the last two years. This projection is particularly noteworthy for a company of its scale and implies its newer products and services will fuel better top-line performance.

Microsoft, Alphabet, Coca-Cola, Monster Beverage—all began as under-the-radar growth stories riding a massive trend. We’ve identified the next one: a profitable AI semiconductor play Wall Street is still overlooking. Go here for access to our full report.

Operating Margin

Abbott Laboratories has managed its cost base well over the last five years. It demonstrated solid profitability for a healthcare business, producing an average operating margin of 17.9%.

Analyzing the trend in its profitability, Abbott Laboratories’s operating margin decreased by 1.4 percentage points over the last five years, but it rose by 2 percentage points on a two-year basis. We like Abbott Laboratories and hope it can right the ship.

In Q4, Abbott Laboratories generated an operating margin profit margin of 19.6%, up 2.2 percentage points year on year. This increase was a welcome development and shows it was more efficient.

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

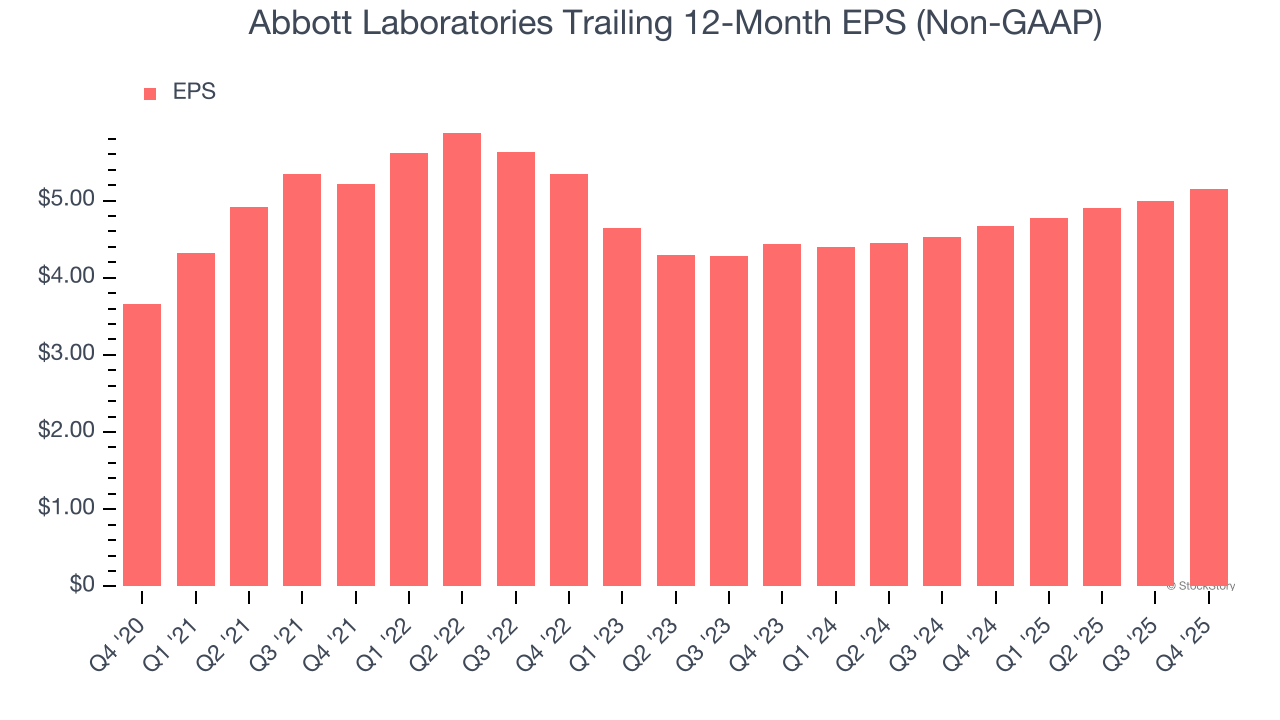

Abbott Laboratories’s EPS grew at a solid 7.1% compounded annual growth rate over the last five years, higher than its 5.1% annualized revenue growth. However, this alone doesn’t tell us much about its business quality because its operating margin didn’t improve.

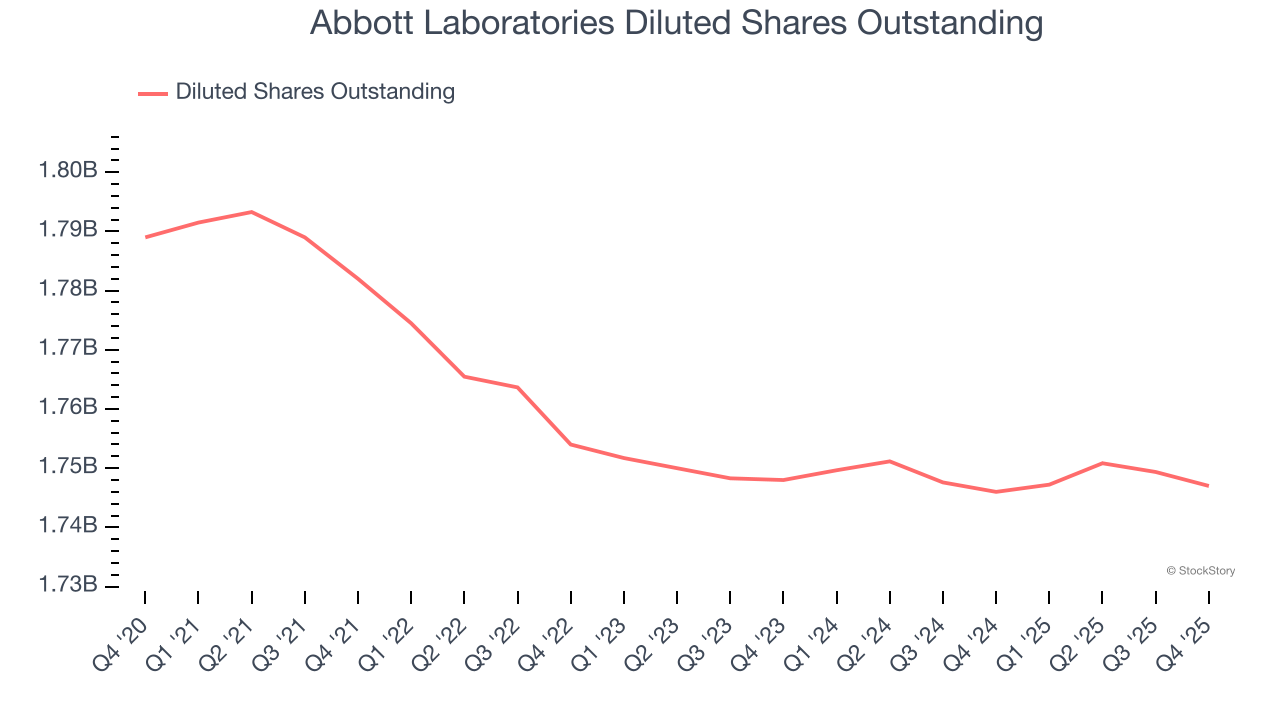

We can take a deeper look into Abbott Laboratories’s earnings to better understand the drivers of its performance. A five-year view shows that Abbott Laboratories has repurchased its stock, shrinking its share count by 2.3%. This tells us its EPS outperformed its revenue not because of increased operational efficiency but financial engineering, as buybacks boost per share earnings.

In Q4, Abbott Laboratories reported adjusted EPS of $1.50, up from $1.34 in the same quarter last year. This print was close to analysts’ estimates. Over the next 12 months, Wall Street expects Abbott Laboratories’s full-year EPS of $5.15 to grow 9.9%.

Key Takeaways from Abbott Laboratories’s Q4 Results

We struggled to find many positives in these results. Its revenue missed and its organic revenue fell short of Wall Street’s estimates. Overall, this was a weaker quarter. The stock traded down 5.5% to $114.10 immediately after reporting.

Abbott Laboratories didn’t show it’s best hand this quarter, but does that create an opportunity to buy the stock right now? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here (it’s free).

/A%20Palantir%20office%20building%20in%20Tokyo_%20Image%20by%20Hiroshi-Mori-Stock%20via%20Shutterstock_.jpg)

/Adobe%20Inc%20logo%20on%20computer-by%20DANIEL%20CONSTANTE%20via%20Shutterstock.jpg)

/Micron%20Technology%20Inc_billboard-by%20Poetra_RH%20via%20Shutterstock.jpg)