/Viatris%20Inc%20logo%20on%20building-by%20SSKH-Pictures%20via%20Shutterstock.jpg)

Canonsburg, Pennsylvania-based Viatris Inc. (VTRS) is a healthcare company that provides a diverse portfolio of branded, generic, and complex medicines to patients. Valued at a market cap of $13.4 billion, the company's product offerings span major therapeutic categories such as cardiovascular, oncology, central nervous system, and infectious disease treatments.

Companies worth $10 billion or more are typically classified as “large-cap stocks,” and Viatris fits the label perfectly, with its market cap exceeding this threshold, underscoring its size, influence, and dominance within the drug manufacturers - specialty & generic industry. The company leverages a wide manufacturing and distribution network, emphasizing access to affordable medicines, operational efficiency, and sustainable cash flow generation.

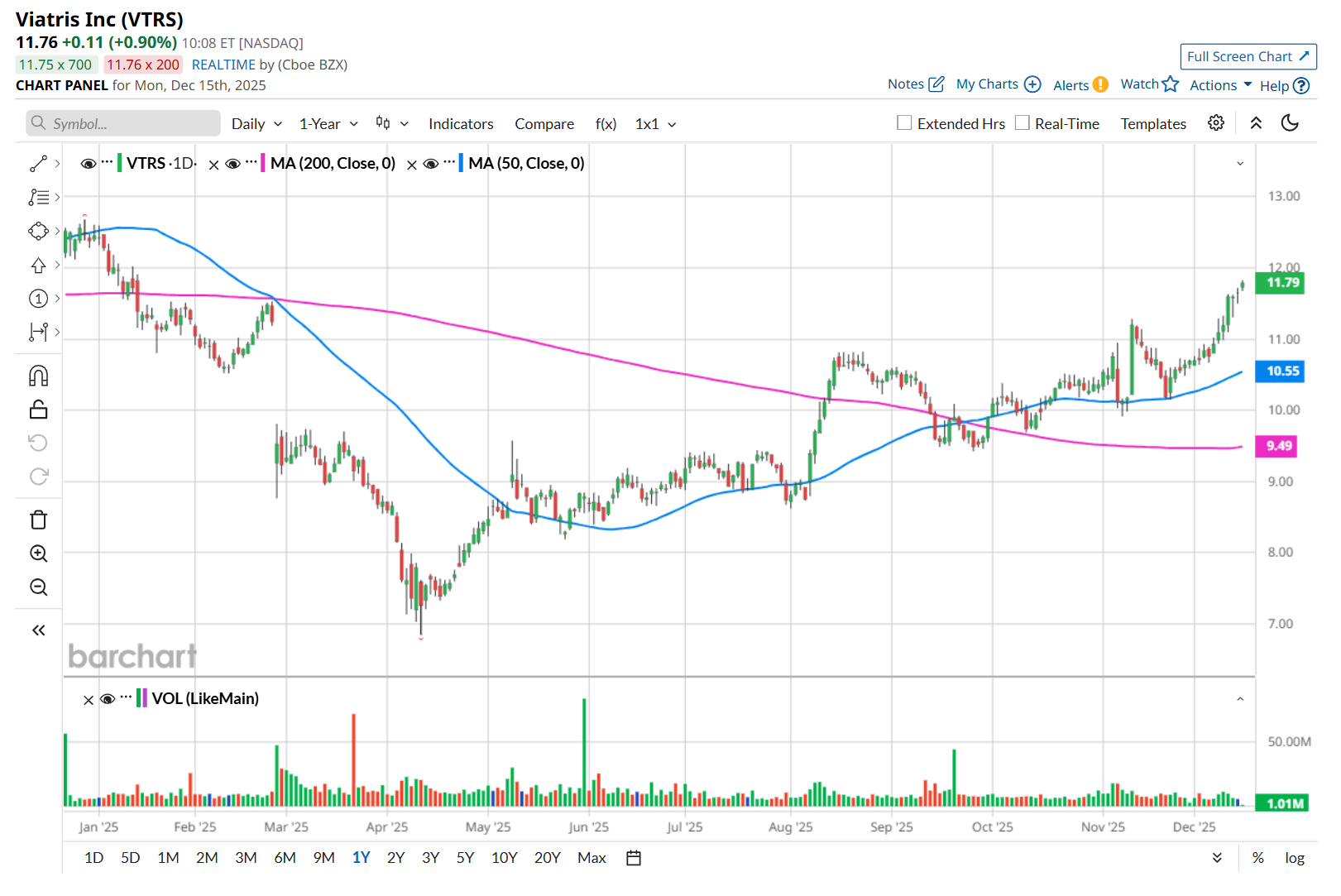

This healthcare company is currently trading 7.7% below its 52-week high of $12.78, reached on Dec. 16, 2024. Shares of Viatris have soared 22.9% over the past three months, outperforming the Dow Jones Industrial Average’s ($DOWI) 5.7% rise during the same time frame.

However, in the longer term, VTRS has declined 6.6% over the past 52 weeks, trailing behind DOWI’s 10.7% uptick over the same time frame. Moreover, on a YTD basis, shares of VTRS are down 5.3%, compared to DOWI’s 14% return.

To confirm its recent bullish trend, Viatris has been trading above its 200-day moving average since late September and has remained above its 50-day moving average since mid-October.

On Nov. 6, shares of Viatris plunged almost 6% after its Q3 earnings release, despite delivering better-than-expected results. The company’s total revenue increased marginally year-over-year to $3.8 billion, surpassing consensus estimates by 3%. Meanwhile, its adjusted EPS of $0.67 declined 10.7% from the year-ago quarter, but topped analyst expectations of $0.63.

VTRS has significantly lagged behind its rival, Teva Pharmaceutical Industries Limited (TEVA), which soared 83.3% over the past 52 weeks and 37.2% on a YTD basis.

Looking at VTRS’ recent outperformance, analysts remain moderately optimistic about its prospects. The stock has a consensus rating of "Moderate Buy” from the 10 analysts covering it, and the mean price target of $12.47, suggests a 6.6% premium to its current price levels.

On the date of publication, Neharika Jain did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/An%20Intel%20sign%20out%20front%20of%20a%20corporate%20office%20by%20wolterke%20via%20Adobe%20Stock.jpeg)

/Alibaba%20by%20testing%20via%20Shutterstock.jpg)

/Alphabet%20(Google)%20Image%20by%20Markus%20Mainka%20via%20Shutterstock.jpg)