Headquartered in Northbrook, Illinois, CF Industries Holdings, Inc. (CF) manufactures hydrogen and nitrogen products, centering its strategy on decarbonizing ammonia production to support low-carbon solutions for energy, fertilizer, emissions control, and industrial applications.

With a market capitalization of nearly $12.4 billion, well above the $10 billion “large-cap” threshold, CF Industries leverages its scale through manufacturing assets in the United States, Canada, and the United Kingdom, complemented by an extensive North American storage, transportation, distribution, and logistics network.

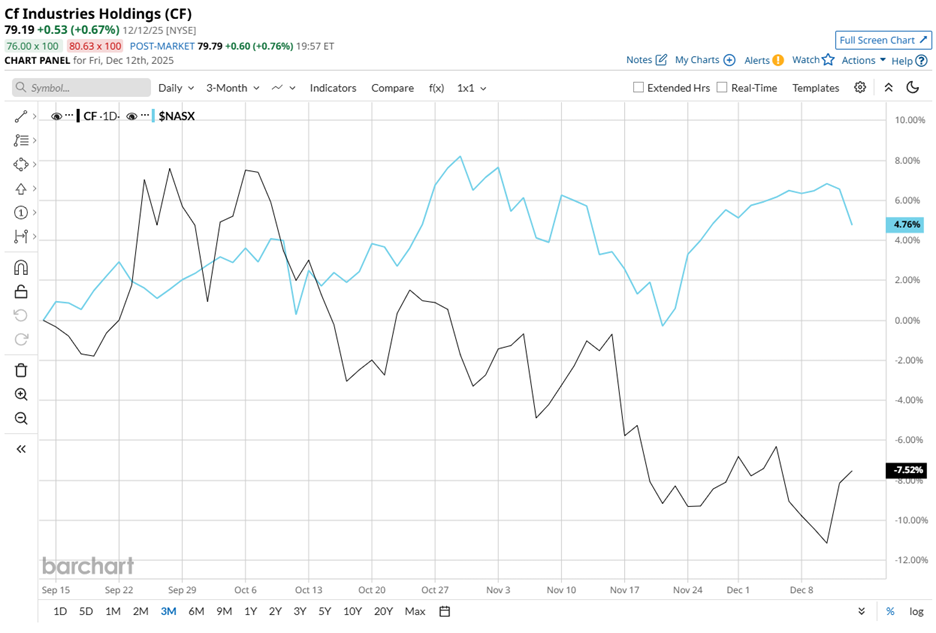

Despite the industrial footprint, CF’s share price tells a more volatile story. The stock trades 24.2% below its June peak of $104.45 and has declined almost 7.5% over the past three months. Over the same period, the Nasdaq Composite ($NASX) advanced 4.8%, highlighting relative underperformance.

Longer-term metrics reinforce the softness. CF’s shares have dropped 12.1% over the past 52 weeks and risen only 7.2% year-to-date (YTD). By contrast, the Nasdaq gained 16.5% over 52 weeks and 20.1% YTD, underscoring a widening performance gap.

Technical indicators echo the pressure. Since mid-Nov, CF stock has consistently traded below its 50-day moving average of $82.97 and its 200-day moving average of $85.05.

Earnings momentum failed to reverse sentiment. On Nov 5, CF Industries released its Q3 2025 results, and the stock fell another 4.2% in the following session despite headline beats. Revenue rose 21.1% year over year to $1.66 billion, matching Street’s estimates, while EPS climbed 41.3% to $2.19, exceeding forecasts of $2.06.

Adjusted EBITDA also increased 30.5% year over year to $667 million, yet investors fixated on softer undercurrents. Markets are staying wary of a tight global nitrogen supply-demand balance, geopolitical risks, and natural gas availability.

Regulatory and operational uncertainties add further weight. CF is facing ambiguity around the European Union’s carbon border adjustment mechanism and its potential cost implications. At the same time, significant maintenance activities curtailed third-quarter production volumes, constraining output and reinforcing concerns about near-term execution.

To put CF’s performance in perspective, its rival CVR Partners, LP (UAN), climbed 26.4% over the past 52 weeks and gained 25.7% YTD, while CF lagged. This creates greater room for upside if CF Industries improves execution and investor sentiment shifts in its favor.

As a result, analysts are maintaining a cautious tone. Among 18 analysts, the consensus rating sits at “Hold,” reflecting balanced expectations. The mean price target of $91.59 implies potential upside of 15.7% from current levels, suggesting measured optimism.

On the date of publication, Aanchal Sugandh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Renewable%20Energy%20by%20Yuri%20Hoya%20via%20Shutterstock.jpg)

/A%20close-up%20of%20a%20General%20Motors%20corporate%20sign%20by%20lindaparton%20via%20Adobe%20Stock.jpeg)