Hertz (HTZ) stock soared nearly 40% on Nov. 4 after the vehicle rental and mobility services giant reported its first profitable quarter in more than two years.

Investors are cheering HTZ primarily because its Q3 earnings release suggests the management’s comprehensive “Back-to-Basics” strategy is beginning to deliver on its promises.

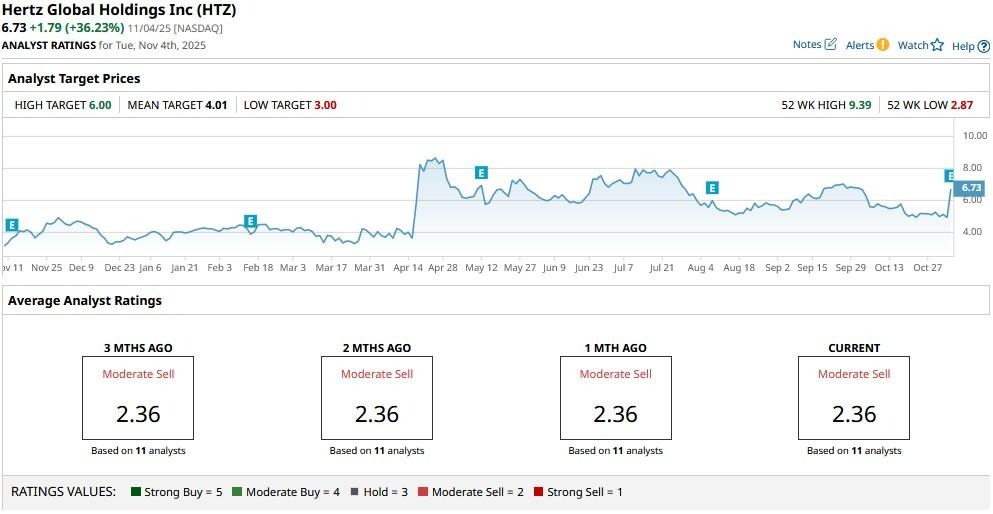

Despite the post-earnings rally, Hertz stock remains down over 35% versus its YTD high in April.

Is Hertz Stock Worth Buying Into the Post-Earnings Strength?

Other than the strong headline numbers, Hertz’ quarterly update had adequate positives to warrant owning the company’s stock heading into 2026.

For example, the Nasdaq-listed firm saw vehicle utilization reach an exceptional 84% in its fiscal Q3, the highest in seven years, driven by improved operational processes and optimized inventory management.

Additionally, depreciation per unit averaged at $273 per month, well within HTZ executives’ target of keeping below $300, and representing a whopping 50% improvement versus a year ago.

More importantly, the company expects to maintain this sub-$300 depreciation level next year as well. Positive free cash flow of $248 million further improves the investment case for HTZ stock.

Where Options Data Suggest HTZ Shares Are Headed Next

Options traders are pricing in continued momentum in Hertz shares after the company’s strong Q3 release.

According to Barchart, contracts expiring in January signal potential for another leg up in HTZ to $7.58. The implied move through the end of next week also currently sits at an exciting 12.14%.

While that indicates significant volatility in the near-term, what it also means is that Hertz could be trading at $6.67 by Nov. 14.

How Wall Street Recommends Playing Hertz Heading into 2026

Heading into Hertz’ earnings release, Wall Street firms had a consensus “Moderate Sell” rating on its stock with a mean target of about $4.

However, the quarterly update could make some analysts upwardly revise their estimates on HTZ stock in the days ahead.

/Intel%20Corp_%20Santa%20Clara%20campus-by%20jejim%20via%20Shutterstock.jpg)

/Nvidia%20logo%20and%20sign%20on%20headquarters%20by%20Michael%20Vi%20via%20Shutterstock.jpg)