/Alphabet%20(Google)%20Image%20by%20Markus%20Mainka%20via%20Shutterstock.jpg)

Alphabet (GOOG) (GOOGL) is scheduled to report its Q2 earnings after market close on July 22 — and the data landscape heading into the print paints a picture of a company operating at an inflection point between explosive growth and unprecedented capital intensity.

The stock closed Friday at about $354, down roughly 3% on news that Google’s Gemini 3.5 Pro AI model has been delayed due to underwhelming internal performance benchmarks — yet shares remain up some 10% year-to-date and 87% over the trailing 12 months.

What to Focus on Alphabet’s Q2 Earnings?

The consensus expectation for Q2 calls for revenue of about $117 billion, representing over 21% year-over-year growth, with earnings per share projected at $2.89.

Google Cloud sales is the most closely watched line item, with Bank of America raising its growth estimate to 70% for the quarter, projecting roughly $22.5 billion in cloud revenue supported by a contracted backlog that nearly doubled sequentially to $462 billion in Q1.

Management has indicated that just over 50% of this backlog converts to revenue within 24 months, providing exceptional forward visibility.

What Options Data Signals Heading into the Q2 Print

The options market is pricing a potential swing of up to 5.56% in either direction by week’s end following the report, with implied volatility running at nearly 60%, miles above realized volatility, indicating the market is bracing for a larger-than-typical move.

Notably, traders are paying about 2x as much for upside calls as for downside protection suggesting a bullish lean.

Prediction markets assign a 96.6% probability that Alphabet delivers another earnings beat, which would mark the fifth consecutive quarter of exceeding consensus estimates.

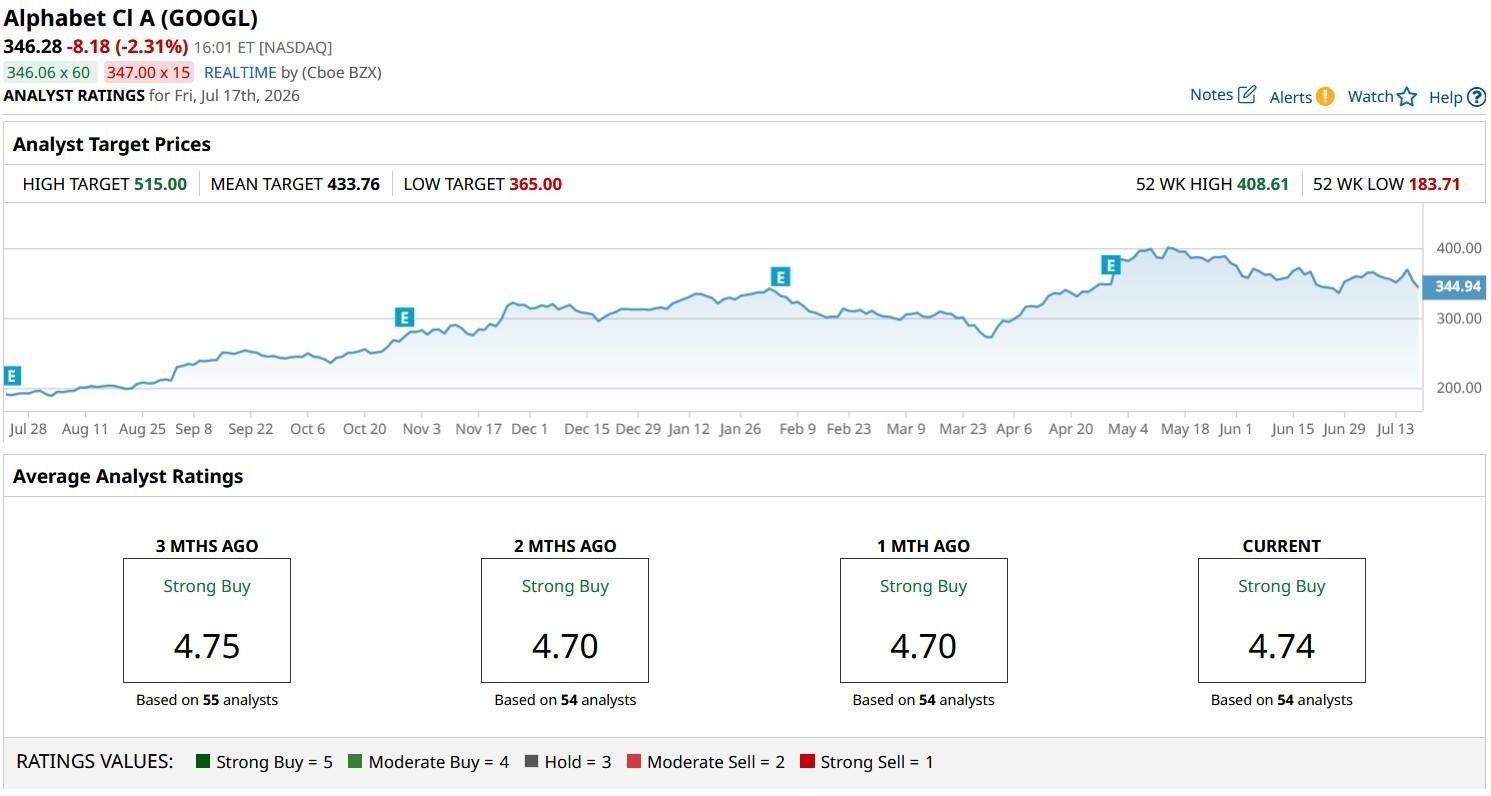

What’s the Consensus Rating on Google Stock?

Wall Street sentiment is overwhelmingly positive, with 49 of 54 analysts rating the stock a “Buy” or “Strong Buy,” zero “Sell” recommendations, and a mean price target near $434, implying roughly 25% upside from current levels.

The most aggressive target on the Street sits at $515, while the lowest is at $365.

BofA maintains a $430 target with an EPS estimate of $8.38, well above the Wall Street consensus of $2.86, largely due to an anticipated $80 billion boost from marking Alphabet’s Anthropic stake to market value following that company’s valuation surge from $380 billion to $965 billion.

How to Play GOOGL Shares At Current Price?

The primary risk factor remains capital intensity. Q1 capex more than doubled year-over-year to $35.67 billion, compressing free cash flow by 46.63%, and full-year 2026 guidance was raised to $180 billion to $190 billion, with management signaling 2027 capex will increase significantly further.

The bull case holds that this spending is demand-validated rather than speculative. Google Cloud is described as “compute constrained,” meaning sales would have been higher had capacity been available, and the $462 billion backlog represents over ten times annual cloud revenue.

High-profile AI talent departures, including Gemini co-lead Noam Shazeer returning to OpenAI and Nobel laureate John Jumper leaving DeepMind for Anthropic, have amplified concerns about Google's competitive position in frontier AI development.

However, these departures have not yet manifested in deteriorating financial metrics, with search revenue growing 19% and AI-powered product revenue growing nearly 800% year-over-year in Q1.

Warren Buffett's personal confirmation that he initiated Berkshire Hathaway's $10 billion Alphabet position provides an additional vote of confidence, though he flagged AI capex as his primary risk concern.

At a forward P/E of nearly 26x with 38.9% return on equity and Google Cloud growing at 63%, outpacing Azure at 40% and AWS at 28%, the valuation disparity between Google’s growth profile and its market multiple remains the central thesis for bulls heading into the July 22 report.

This article was created with the support of automated content tools from our partners at Sigma.AI. Together, our financial data and AI solutions help us to deliver more informed market headline analysis to readers faster than ever.

On the date of publication, Wajeeh Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/An%20image%20of%20the%20Snowflake%20logo%20on%20a%20corporate%20office_%20Image%20by%20Grand%20Warszawski%20via%20Shutterstock_.jpg)

/Netflix%20on%20tv%20with%20remote%20by%20freestocks%20via%20Unsplash.jpg)