/J_P_%20Morgan%20logo%20at%20the%20top%20of%20a%20skyscraper%20By%20Robert.jpeg)

Few things have gotten as much attention on Wall Street as artificial intelligence (AI) over the last six months, but there is another theme that has been quietly developing: record profitability among the largest U.S. banks. Increased market activity, robust demand for loans, and a revival of investment banking have generated massive amounts of capital for banks, creating opportunities for hefty dividends and large-scale share repurchases.

JPMorgan Chase (JPM) is leading the way. After another quarter with record revenues and profits, the bank has decided to increase its quarterly dividend by 10% to $1.65 per share, subject to approval by its board of directors. The decision comes shortly after the success of the Fed's annual “stress test” and shows how healthy the balance sheet of the company is, raising questions about whether JPM stock will keep performing well after reaching all-time highs.

About JPMorgan Chase Stock

JPMorgan is the largest U.S. bank in terms of assets and market capitalization, offering consumer banking, commercial lending, investment banking, markets, wealth management, and asset management services in more than 100 countries. The company is headquartered in New York, New York. Its market capitalization stands at $919 billion, making it one of the most valuable financial firms in the world.

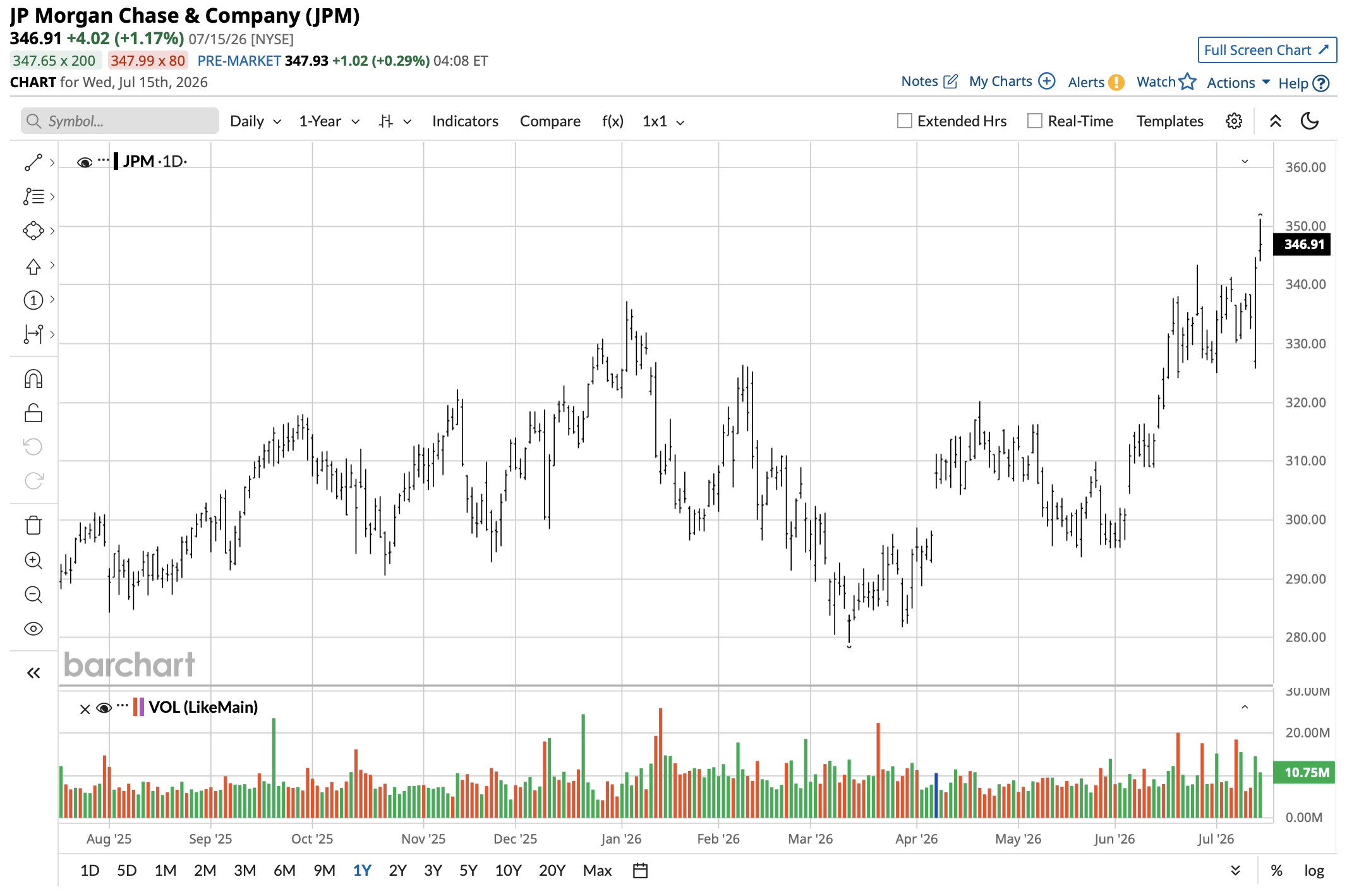

Shares have continued to rally in 2026. JPM stock currently trades near $341, not far from the 52-week high of $351.24, up about 22% from its 52-week low. JPM stock has also performed better than much of the financial sector over the last year, with the firm sporting consistent growth in earnings and profitability.

In terms of valuation, JPM still looks reasonable in spite of its rally. The stock trades at 15.1 times forward earnings and 2.6 times book value, which is appealing for a company with an 18% return on equity (ROE) and margins above 20%. When compared with other high-quality financial stocks, the valuation indicates that investors are willing to pay a premium for JPMorgan's top-notch performance.

The increase in JPMorgan's dividend from $1.50 to $1.65 per share will lift the annualized payout by 10%, but the forward dividend yield will still be 1.9%. While this is quite low in comparison with some regional banks, JPMorgan's dividend history has been characterized not by yield chasing but by earnings growth and prudent capital management.

JPMorgan Beats on Earnings

JPMorgan delivered another great second-quarter report. The bank reported $21.2 billion in net income or $7.70 per share, and $16.9 billion in earnings excluding significant items or $6.14 per share. Revenue reached a record $57.3 billion thanks to strength in almost all lines of business.

The numbers showed great momentum throughout the report. Investment banking fees grew 30% year-over-year (YOY) to the highest level since 2021 amid increased dealmaking. Markets revenue increased 35%, including a remarkable 86% rise in equity trading revenue due to higher client activity. Moreover, average loans were up 10%, deposits were up 7%, assets under management (AUM) reached a record $5.1 trillion, and mobile customers continued increasing.

Perhaps most importantly for shareholders, management highlighted capital strength rather than raised concerns regarding potential future regulatory requirements. The bank's CET1 ratio was at 14.1%, comfortably above minimum regulatory requirement, and the Federal Reserve has affirmed that the Stress Capital Buffer of JPMorgan will remain unchanged at 2.5% until September 2027. This provides a lot of flexibility for future dividends and share repurchases.

The decision regarding the dividend is a perfect example of that. With the official approval of the board, which is expected later this year, JPMorgan will increase its quarterly dividend to $1.65 per share, while also maintaining the buyback program after repurchasing $6.2 billion worth of common stock during Q2.

CEO Jamie Dimon also sounded quite optimistic regarding the economy. Dimon noted continued strength in business investments, AI spending, and hiring, while admitting risks of geopolitical tensions, inflation, and more. However, management stressed that JPMorgan is prepared for a variety of economic scenarios.

What Do Analysts Expect From JPMorgan Stock?

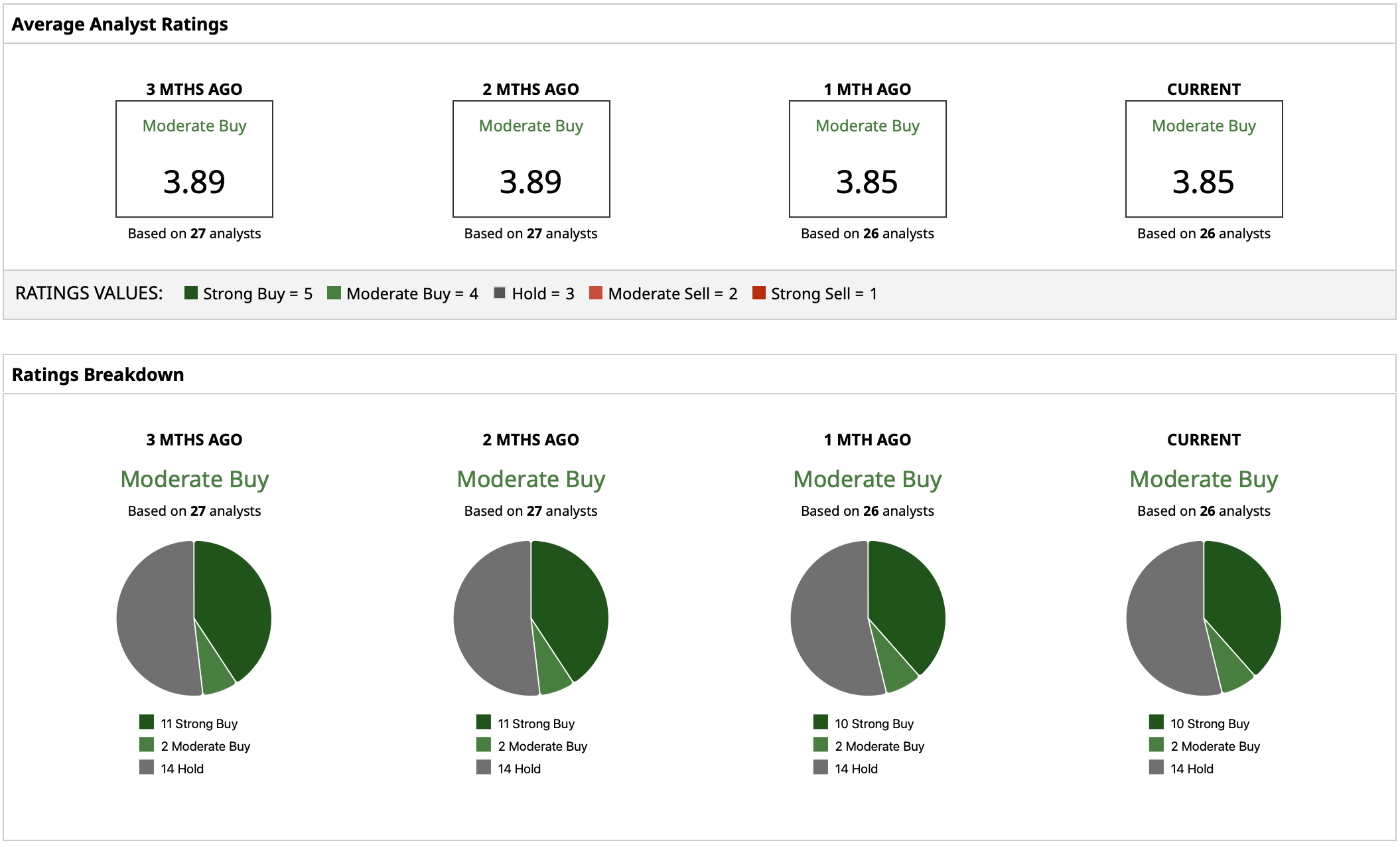

Wall Street remains bullish regarding JPMorgan after its latest results with a consensus “Moderate Buy” rating. Analysts still see the firm as one of the highest-quality franchises in global banking thanks to diversified earnings, superior performance, and a strong balance sheet. The mean price target of $357.39 implies limited potential upside of 5% from current levels, which means that the near-term earnings power of the bank is already baked into the price. However, there is still significant potential upside of 23% from Bank of America Securities' Street-high target of $420, if investment banking activity and capital markets continue to perform well through 2026.

On the date of publication, Yiannis Zourmpanos did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/An%20image%20of%20the%20Snowflake%20logo%20on%20a%20corporate%20office_%20Image%20by%20Grand%20Warszawski%20via%20Shutterstock_.jpg)

/Netflix%20on%20tv%20with%20remote%20by%20freestocks%20via%20Unsplash.jpg)