The narrative pitched by Wall Street underwriters has been irresistible. They said that after years of high interest rates kept the listing window shut, the floodgates were finally bursting open. Investors were told they could finally get direct access to the crown jewels of the venture capital world: advanced manufacturing and next-generation infrastructure.

But now that the initial hype has faded and the first few quarters of public market reality have set in, I decided to look past the promotional press releases and incessant financial TV coverage.

When you look at how the hottest debuts of the past 12 months are actually performing, the scorecard looks more like a warning than a victory. Plus, OpenAI and Anthropic are slowing down their sprints to market.

When giant, highly anticipated companies go public near what looks like a late-stage market cycle, they act as massive liquidity sponges. They raise tens of billions of dollars from eager retail accounts right at the peak of optimism.

Consider Lineage (LINE), which grabbed headlines as the largest IPO of 2024 when it went public at $78 a share. Pitched as a stable, physical moat because it operates as the world’s largest temperature-controlled warehouse network, it enjoyed a massive first-week “pop” as investors rushed in. Fast forward to today, and that enthusiasm has turned cold. The stock has steadily bled away its gains as the market remembers that heavy industrial infrastructure carries massive real-world operating costs that high-multiple tech valuations simply cannot support.

Then, there’s the AI hardware plays that rushed to market to ride Nvidia’s (NVDA) coattails. Cerebras Systems (CBRS) made a thunderous debut earlier this year, pricing its massive multibillion-dollar offering at $185 a share with the pitch that its “wafer-scale” chips could process AI workloads 20 times faster than the market leader. While the stock initially rocketed on pure momentum, the post-IPO reality has become a brutal trading environment. Investors are waking up to the reality that lining up partners is cheap, but executing on capital-intensive hardware manufacturing in a supply-heavy market is an entirely different beast.

Trap Door for Founders, A Financial Trap for the Public

For DIY retail investors, the biggest danger of chasing hot IPOs isn’t just the volatile day-to-day trading. It is how these things play out in the early months post-IPO, as engineered by Wall Street bankers.

When a company goes public, early venture capital backers, founders, and executives are typically bound by a 180-day lockup period. Typically, during these first six months, insiders are contractually banned from selling their shares, creating an artificial scarcity of stock. Because there are relatively few shares available to trade, regular retail demand can easily drive the stock price up into an unsustainable spike.

In the case of SpaceX (SPCX) above, that only lasted a few days.

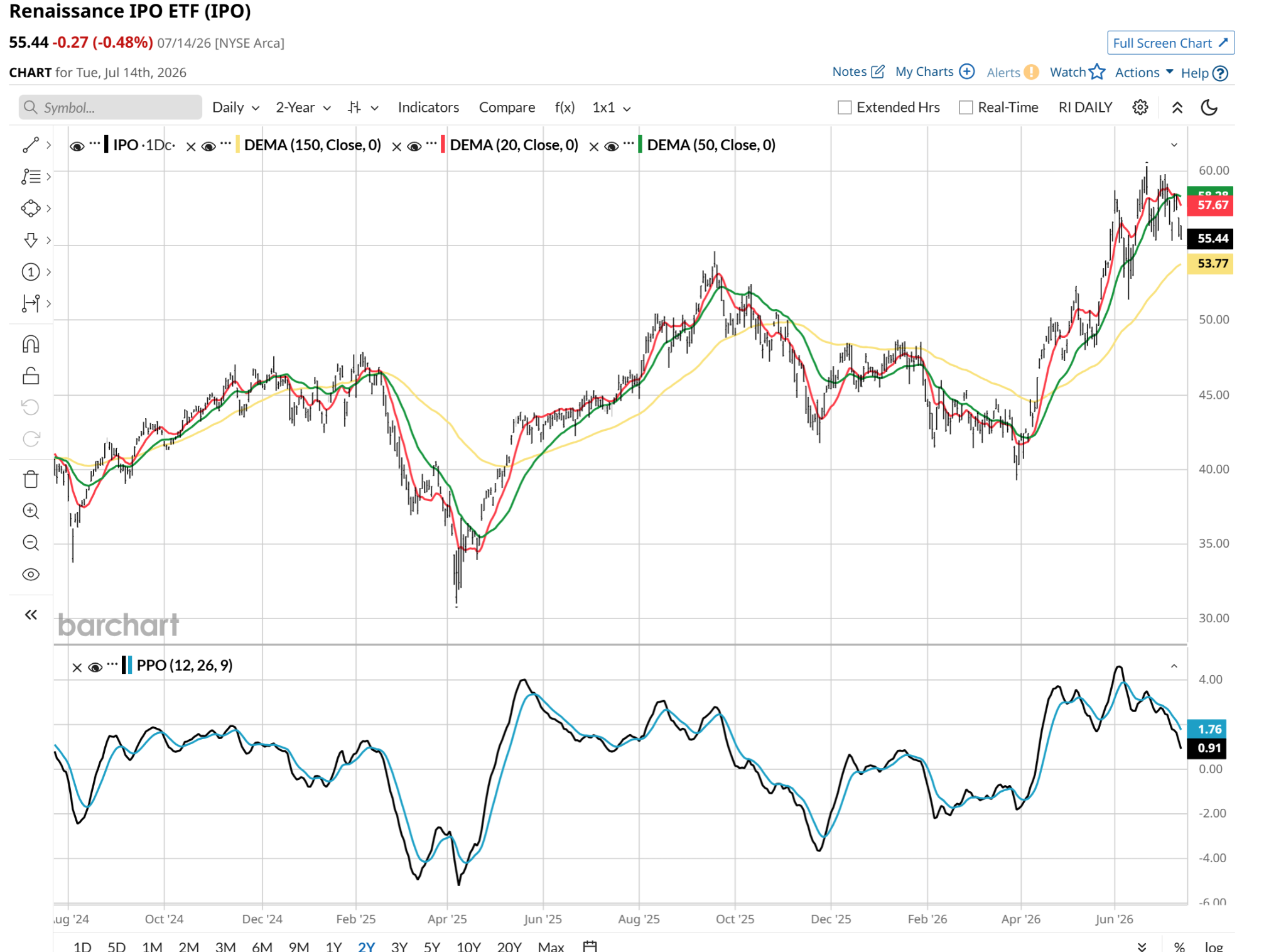

If that chart directly above is any indication, IPOs from the past three years are more likely to emulate the recent decline of SPCX than this decade’s surge higher by NVDA. The Renaissance IPO ETF (IPO) is a $166 million fund that started back in 2013. It buys IPOs and holds them for three years.

Which Recent IPOs Have the Best-Looking Charts?

I scanned the holdings, and here are the five I thought had the best charts. They are likely to be trend-breakers, since that IPO ETF chart above features a wilting percentage price oscillator (PPO) and a 20-day moving average that wants to head south.

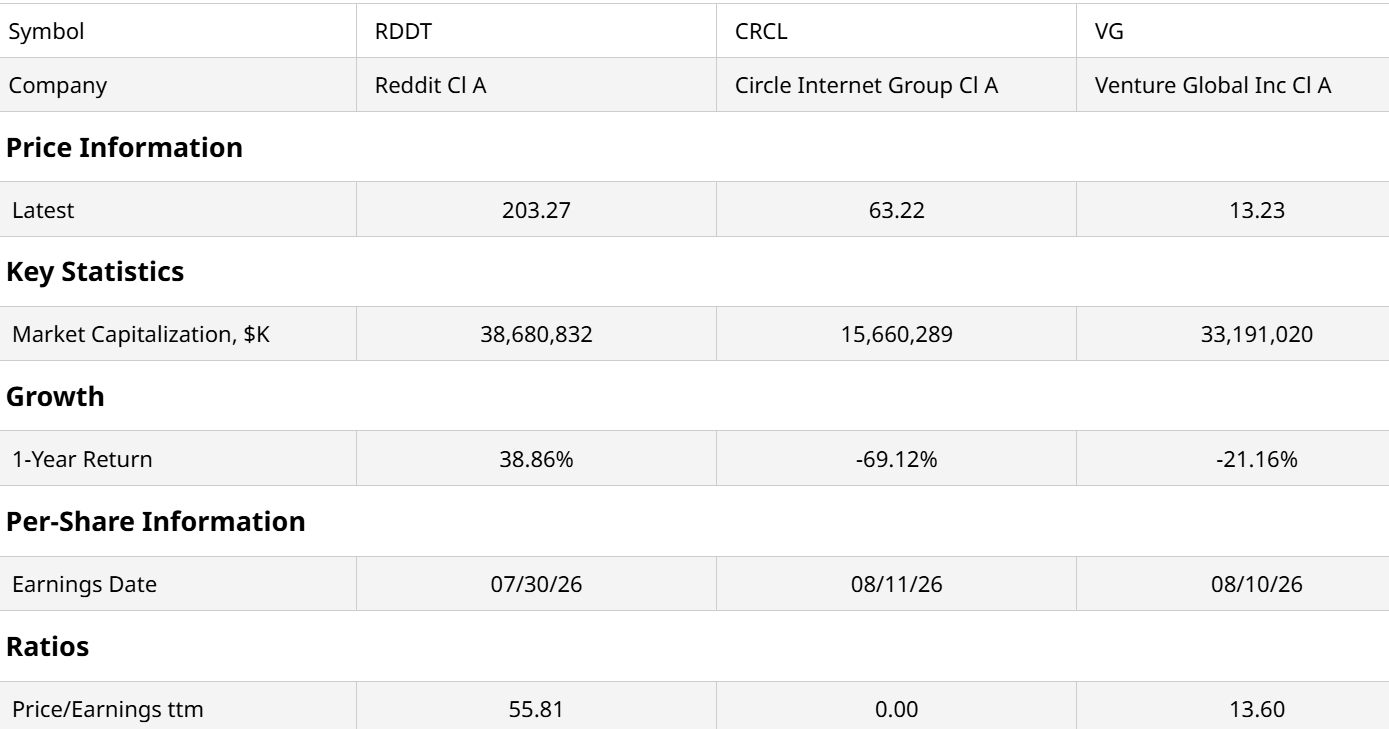

Reddit (RDDT) grabbed massive headlines with its March 2024 debut, managing to hold onto its premium valuation thanks to unique community-driven data licensing deals with tech giants.

Meanwhile, stablecoin issuer Circle Internet Group (CRCL) experienced an incredibly volatile round-trip following its blockbuster 2025 listing, soaring immediately after launch before facing a steep 68% decline as the initial crypto-infrastructure hype cooled.

Finally, Venture Global LNG (VG) has faced a turbulent post-IPO market, navigating brutal energy sector swings and project delays that heavily depressed its stock, even as recent geopolitical tensions in the Middle East spark a sharp fundamental rebound in global liquefied natural gas fees.

Final Thoughts

When the lockouts end, the floodgates truly open.

Insiders who have been holding illiquid private shares for maybe a decade look at the public ticker and rush to cash out. This massive wave of secondary selling introduces a heavy, permanent supply of stock for sale that broad retail demand simply cannot absorb. The unhappy ending is filled with deep, multi-month drawdowns.

Rob Isbitts is a semi-retired CIO, former fiduciary investment advisor, and Barchart columnist. Check out his other work at ETFYourself.com (featuring the Fresh Charts weekly trading post), and ROAR.PiTrade.com, helping investors to better-manage their own portfolios.

On the date of publication, Rob Isbitts did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20close-up%20of%20a%20General%20Motors%20corporate%20sign%20by%20lindaparton%20via%20Adobe%20Stock.jpeg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Zoetis%20sign%20at%20their%20Canadian%20By%20JHVEPhoto.jpeg)

/Microsoft%20headquarters%20By%20Peter.jpeg)

/A%20SoFi%20logo%20on%20an%20office%20building%20by%20Tada%20Images%20via%20Shutterstock.jpg)