/Alphabet%20(Google)%20Image%20by%20Markus%20Mainka%20via%20Shutterstock.jpg)

Alphabet (GOOG) (GOOGL) is pushing deeper into the artificial intelligence (AI) race as it expands the capabilities of its Gemini ecosystem with two new AI models, Nano Banana 2 Lite and Gemini Omni Flash. The launches highlight Google’s strategy of making advanced generative AI faster, cheaper, and more accessible across consumer products, developers, and enterprise applications.

Nano Banana 2 Lite is Google’s most cost-efficient image generation model, delivering text-to-image outputs in about four seconds at a low cost of $0.034 per 1,000 images, making it suitable for rapid design, prototyping, and large-scale image creation.

Meanwhile, Gemini Omni Flash focuses on high-quality video generation and conversational video editing, allowing developers to build advanced multimedia applications through the Gemini API and Google AI Studio. Priced at $0.10 per second of video output, the model strengthens Google’s push into AI-powered content creation and developer tools.

These releases represent more than just new AI features as they are part of Google’s broader effort to defend its leadership in search, cloud, advertising, and AI-powered productivity tools. As competition intensifies, these latest AI breakthroughs might translate into stronger monetization and reinforce Google’s position in the next phase of the AI revolution.

Amid these innovative moves, what should be your stance?

About Alphabet Stock

Headquartered in Mountain View, California, Alphabet has transformed the tech landscape through its wide-ranging businesses, including Google Services, Google Cloud, and forward-looking initiatives like Waymo and Verily. Its strategic focus on artificial intelligence and cloud computing continues to be a major growth engine, reinforcing its strong competitive positioning. With a market cap of $4.36 trillion, Alphabet remains a dominant force in global technology and a key member of the Magnificent Seven (MAGS).

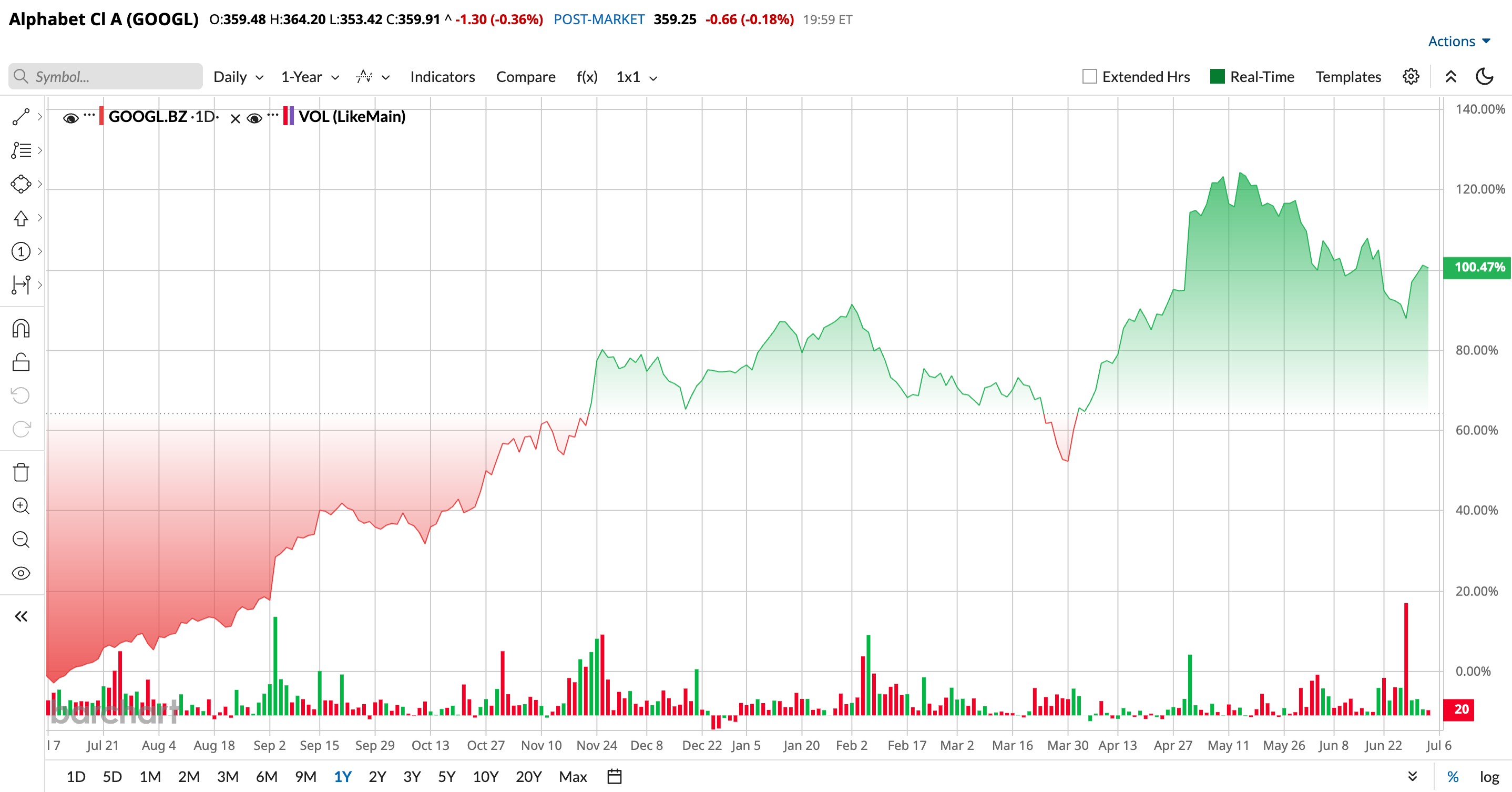

Alphabet’s stock has delivered a strong rally over the past year as investors increasingly rewarded the company’s AI strategy, cloud growth, and improving monetization across its ecosystem. The stock has gained 101.5% over the past 52 weeks and is up 15% year-to-date (YTD), highlighting continued investor confidence in Google’s ability to capitalize on the AI opportunity.

Moreover, the company has continued expanding its Gemini AI ecosystem, with new AI models aimed at improving search, content creation, and developer adoption.

The stock reached a 52-week high of $408.61 on May 18, 2026, reflecting optimism around Alphabet’s AI advancements, strong earnings momentum, and accelerating cloud business. However, since that peak, shares have pulled back 11.9% as investors weighed concerns around rising AI infrastructure spending and whether massive capital investments will translate into near-term returns.

GOOGL currently trades at a premium compared to the sector median and its own historical average at 25.23 times forward price-to-earnings (Non-GAAP).

Better-than-Expected Q1 Results

Alphabet delivered a solid first-quarter 2026 earnings report on April 29, materially exceeding expectations. Total revenue came in at $109.9 billion, up 22% year-over-year (YOY), representing one of the company’s strongest growth rates in recent years and comfortably ahead of consensus estimates.

Its bottom line expanded even faster than the top line. Net income surged to $62.6 billion, up 81% YOY from $34.5 billion, while EPS rose to $5.11, up 82% YOY and topped the consensus estimates. Operating income increased 30% YOY to $39.7 billion, with operating margins expanding to roughly 36% from 34%, highlighting improved efficiency despite heavy AI investment.

Moreover, Google Cloud emerged as the primary growth engine, with revenue rising 63% YOY to $20 billion, driven by surging enterprise demand for AI infrastructure and services. Meanwhile, Search remained resilient with roughly 19% growth, while broader Google Services revenue grew 16% YOY, and YouTube advertising also posted solid gains.

Furthermore, the company raised its 2026 capital expenditure guidance to $180 billion to $190 billion, signaling an aggressive push to scale AI infrastructure, including data centers and proprietary chips.

Investors cheered the beat with shares rising 9.96% on April 30.

Analysts remain optimistic, forecasting EPS of roughly $14.30 for fiscal 2026, a 32.3% YOY jump, followed by a further 3.2% rise to $14.75 in 2027.

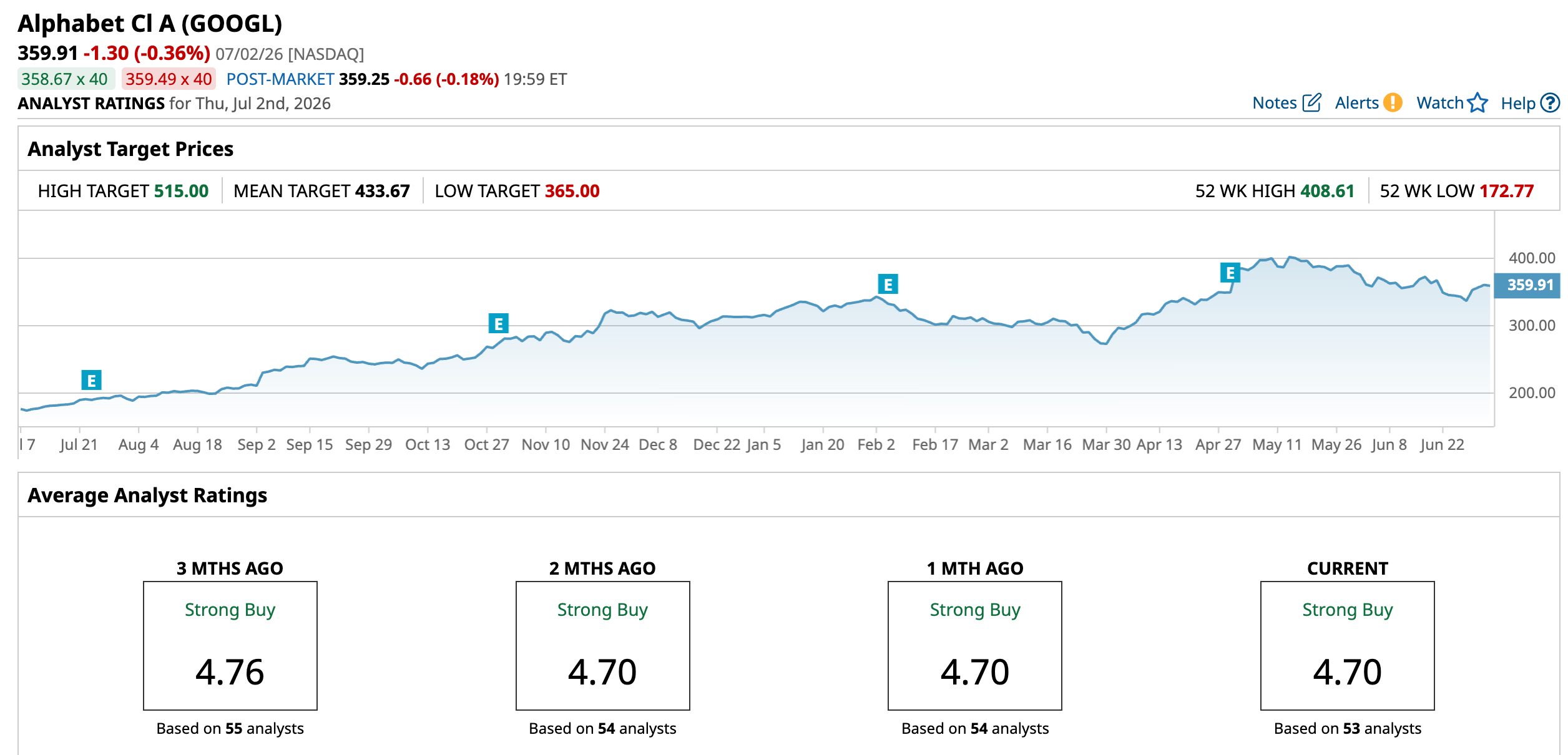

What Do Analysts Expect for Alphabet Stock?

Most recently, Jefferies reiterated its “Buy” rating on Alphabet with a $445 price target, citing the company’s long-term AI leadership, strong Google Cloud growth, massive distribution network, and advantage from its vertically integrated TPU.

Also, Citizens maintained a “Market Outperform” rating and $515 price target on Alphabet, highlighting continued confidence in the company’s AI strategy despite concerns around talent retention. The firm noted the departure of Google AI executive Noam Shazeer, to OpenAI as a reminder of competitive pressure in the AI talent market.

Additionally, TD Cowen raised its price target for GOOGL to $475 from $450 while maintaining a “Buy” rating, citing strong long-term growth potential from Google Cloud and AI investments.

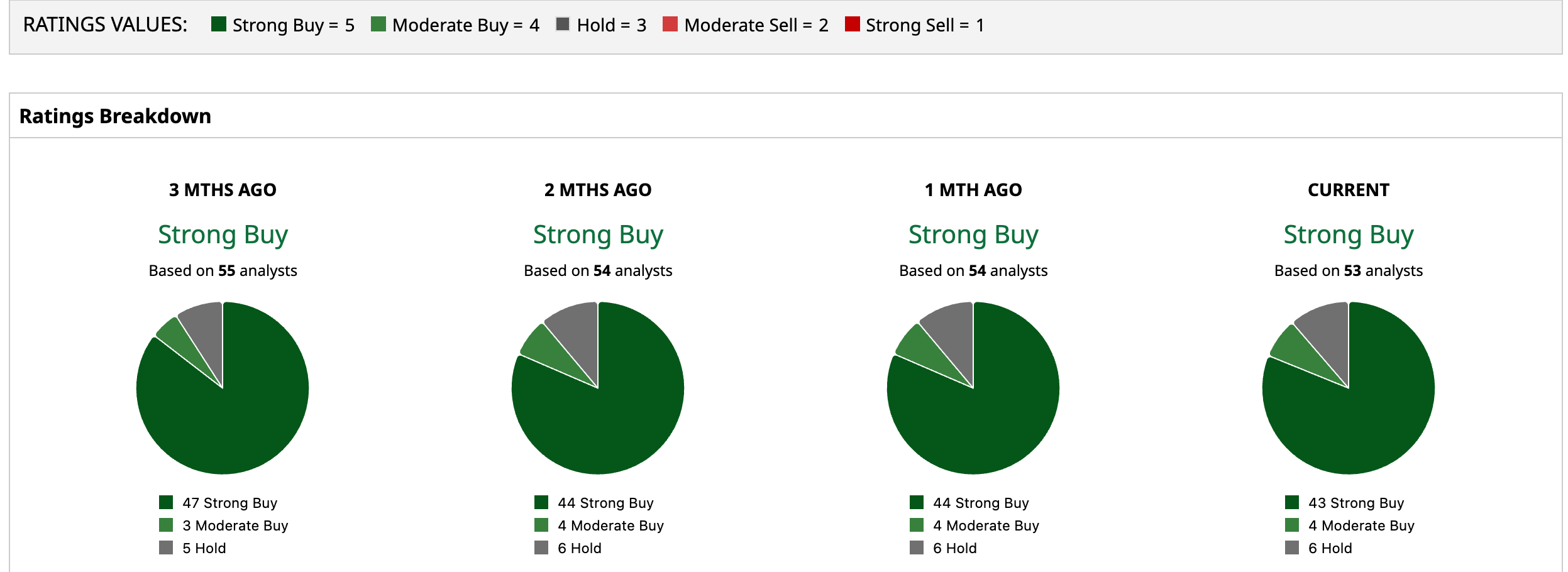

Wall Street is majorly bullish on GOOGL. Overall, GOOGL has a consensus “Strong Buy” rating. Of the 53 analysts covering the stock, 43 advise a “Strong Buy,” four suggest a “Moderate Buy,” and the remaining six analysts are on the sidelines, giving it a “Hold” rating.

GOOGL’s average analyst price target of $433.67 indicates an upside of 20.5%, while Citizens’ Street-high target price of $515 suggests that the stock could rally as much as 43.1%.

On the date of publication, Subhasree Kar did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/AI%20technology%20concept%20by%20NMStudio789%20via%20Shutterstock.jpg)