Super Micro Computer (NASDAQ:SMCI) investors got good news last month after learning that the tech company, which has been mired in controversy in recent months, was able to file its quarterly and annual financials on time, satisfying the Nasdaq exchange. By doing so, it alleviates fears around the accuracy of its financials and it means the stock isn't at risk of being delisted anytime soon.

Now that the financials are filed, is it safe to once again buy shares of the company? Let's take a closer look at Supermicro's numbers, and assess whether it's a good investment.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. Learn More »

Compliance regained, but slowing growth may be a new concern

On Feb. 28, Supermicro filed its outstanding quarterly and annual reports, putting the stock back in compliance with the Nasdaq exchange. The tech company, which sells servers and IT solutions and infrastructure, says it can now fully focus back onto its growth strategy.

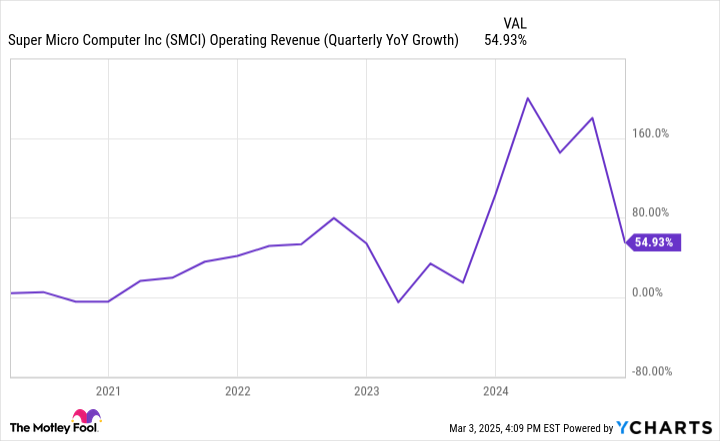

For the last three months of 2024, Supermicro reported sales of $5.7 billion, which were up 55% year over year. That's a fast growth rate but it is a declining one for a company that for multiple periods in the past was more than doubling its top line.

SMCI Operating Revenue (Quarterly YoY Growth) data by YCharts

However, it is difficult for a company to sustain such a high rate of growth, and a slowdown can be inevitable. But there are also signs that the business is growing slower than expected.

In February, Supermicro released updated guidance for fiscal 2025, which ends in June, projecting sales to be within a range of $23.5 billion to $25 billion (it was previously $26 billion to $30 billion). That would still result in a growth rate of around 62% at the midpoint, but it's still a sizable adjustment in the forecast nonetheless.

Its margins remain low

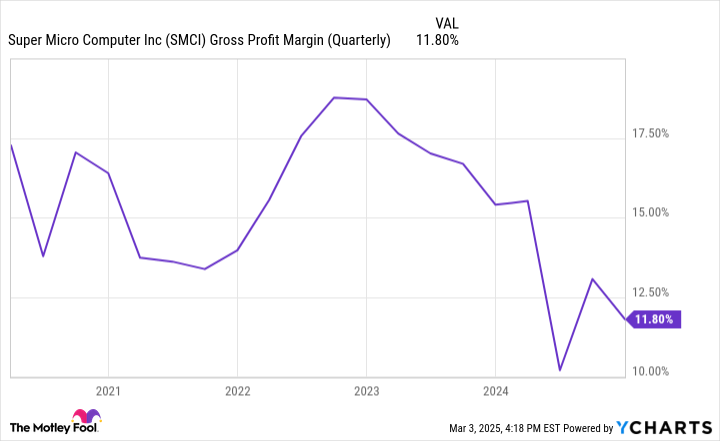

One of the things that concerned me about Supermicro's financials in the past was its low margins. And that remains a problem. A low gross profit margin will make it difficult for the company to grow its sales, especially if its top line isn't growing nearly as fast as it was before. Supermicro's margins dipped below 12% last year and the company still appears to be struggling to improve upon them.

SMCI Gross Profit Margin (Quarterly) data by YCharts

Supermicro has reported a profit in each of the past four quarters, which is a positive sign, but its low margins means that there isn't much of a buffer should costs spike, which may happen due to tariffs and worsening macroeconomic conditions.

This still isn't a terribly safe stock to own

While Supermicro filed its financials on time, investors shouldn't forget that's just the minimum to satisfy the exchanges; it's not a reason to invest in the business.

The big picture is that its growth rate is slowing down, and Supermicro's expenses may rise higher in the near future. And without strong margins to offer a good buffer, I wouldn't be surprised if the company's profits shrink in future quarters. This is still a highly volatile stock that investors may be better off watching rather than buying right now.

Should you invest $1,000 in Super Micro Computer right now?

Before you buy stock in Super Micro Computer, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Super Micro Computer wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $677,631!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*. Don’t miss out on the latest top 10 list, available when you join Stock Advisor.

*Stock Advisor returns as of March 3, 2025

David Jagielski has no position in any of the stocks mentioned. The Motley Fool recommends Nasdaq. The Motley Fool has a disclosure policy.

/NVIDIA%20Corp%20logo%20outside%20building-by%20BING-JHEN_HONG%20via%20iStock.jpg)

/Microsoft%20headquarters%20By%20Peter.jpeg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Amazon%20-%20Image%20by%20bluestork%20via%20Shutterstock.jpg)