Shares of shoe company Deckers Outdoor (NYSE:DECK) pulled back 21.4% during February, according to data provided by S&P Global Market Intelligence. The company reported financial results right at the end of January, which started the decline. And this fall merely carried over into the new month as investors and analysts continued to digest the report.

On Jan. 30, Deckers reported financial results for its fiscal third quarter of 2025, beating estimates and raising its guidance. And yet the stock still plunged and has continued sliding since. For some, this was a surprising outcome.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. Learn More »

The issue is what Deckers' guidance implies for its upcoming fiscal fourth quarter. Given the numbers the company has already reported for the first three quarters of the fiscal year, management expects to generate Q4 net sales of about $936 million. For perspective, it had net sales of $960 million in the fourth quarter of fiscal 2024.

Additionally, Deckers' guidance implies a Q4 gross margin of about 52%, compared with a gross margin of over 56% in the prior-year period. So growth and margins are suddenly hitting a wall, which has investors quite worried.

Deckers set to take a step back from record results

For context, Deckers has been a publicly traded company for 30 years, and yet it's guiding for a record-high gross margin of 57% for its fiscal 2025. Give management some credit for this, but not all the credit. There are some particular things outside its control that it's benefited from, particularly high average selling prices and lower sales at wholesale channels.

In the conference call to discuss Q3 results, Deckers' CFO Steve Fasching said, "While we are proud to deliver this record gross margin, I would caution that the extremely high levels of full-price selling and very low levels of wholesale closeouts are abnormal, and not something we would normally expect to repeat going forward."

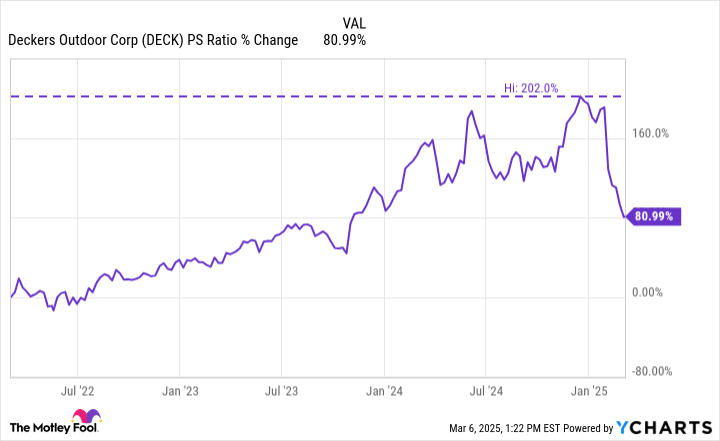

Here's the thing: Deckers stock was trading at an all-time high price-to-sales (P/S) ratio of 7, which is high for a shoe stock, and was up roughly 200% in just three years. Its valuation was supported with strong growth and higher margins. But with both those things cooling, at least temporarily, it was natural for Deckers stock to keep sliding in February as that valuation comes down.

DECK PS Ratio data by YCharts

What's next for Deckers shareholders?

Shoe retailers such as Foot Locker have mentioned that shoppers are looking for discounted shoes right now, which is a headwind for the entire space, including Deckers. But perspective is important. At the end of the day, the company believes it will grow net sales by 15% in fiscal 2025 and have record gross margin of over 57%. That's a healthy business.

The question is how much Deckers can continue to grow in fiscal 2026 and beyond. Even moderate growth could result in decent stock performance, considering the financial strength of the company and the now-lower valuation.

Don’t miss this second chance at a potentially lucrative opportunity

Ever feel like you missed the boat in buying the most successful stocks? Then you’ll want to hear this.

On rare occasions, our expert team of analysts issues a “Double Down” stock recommendation for companies that they think are about to pop. If you’re worried you’ve already missed your chance to invest, now is the best time to buy before it’s too late. And the numbers speak for themselves:

- Nvidia: if you invested $1,000 when we doubled down in 2009, you’d have $304,161!*

- Apple: if you invested $1,000 when we doubled down in 2008, you’d have $44,694!*

- Netflix: if you invested $1,000 when we doubled down in 2004, you’d have $534,395!*

Right now, we’re issuing “Double Down” alerts for three incredible companies, and there may not be another chance like this anytime soon.

*Stock Advisor returns as of March 3, 2025

Jon Quast has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Deckers Outdoor. The Motley Fool recommends Foot Locker. The Motley Fool has a disclosure policy.

/Cybersecurity%20by%20AIBooth%20via%20Shutterstock.jpg)