DigitalOcean (DOCN) just reached an important milestone. The cloud infrastructure company officially joined the Russell 1000 Index on June 29, a move that reflects its rapid growth and expanding market value. The announcement comes after an exceptional first quarter in which the company beat Wall Street's expectations on both revenue and earnings while raising its full-year outlook.

The timing couldn't be better. DigitalOcean has transformed itself into an AI-focused cloud platform, attracting larger enterprise customers and AI startups at a rapid pace. That combination has sent DOCN stock soaring over the past year. But after such a massive rally, investors also need to consider whether the valuation already reflects much of the optimism.

The Russell 1000 Inclusion Caps an Incredible Run

Joining the Russell 1000 is more than just a symbolic achievement. It means DigitalOcean has grown from a small-cap company into a firm that qualifies for one of the market's most widely followed large-cap indices. The change became effective on June 29, prompting passive index funds that track the Russell 1000 to add DOCN shares to their portfolios.

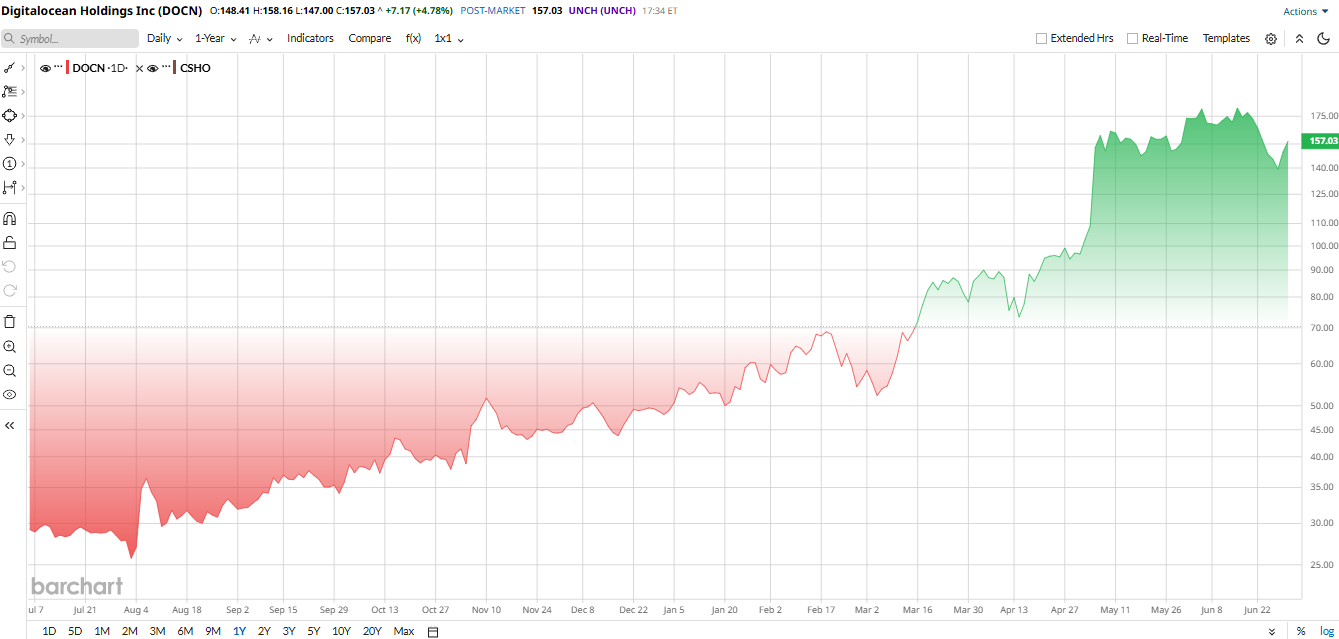

Investors welcomed the news. DOCN stock gained almost 8% on June 29 and has been one of the market's biggest winners over the past year. Shares have surged approximately 350% over the last 12 months and are up 167% year-to-date (YTD).

The rally hasn't been driven by the index inclusion alone. Investors have also responded positively to DigitalOcean's AI strategy, stronger-than-expected earnings, and growing demand from larger customers running AI inference workloads.

The biggest challenge for investors isn't the business. It's the stock price. Following its massive rally, DigitalOcean now trades at 119 times trailing earnings as tracked by Barchart, well above the broader tech sector. Its price-to-sales (P/S) ratio has also expanded well beyond many cloud infrastructure peers.

DigitalOcean's Q1 Earnings Show AI Demand Is Accelerating

Q1 results explain why investors have become so optimistic. Revenue climbed 22% year-over-year (YOY) to $258 million, comfortably ahead of Wall Street expectations of roughly $249 million. Adjusted earnings also topped estimates, with non-GAAP EPS of $0.44 versus analyst expectations near $0.26.

Annual run-rate revenue (ARR) reached $1.03 billion, marking another major milestone for the business. Even more encouraging, AI-related customers generated $170 million in ARR, up 221% YOY, with revenue from customers spending more than $1 million annually growing by 179%.

Management was confident enough to raise its full-year outlook. DigitalOcean now expects 2026 revenue between $1.13 billion and $1.145 billion, representing roughly 25% to 27% annual growth, alongside higher earnings guidance.

DigitalOcean Is Betting Heavily on Becoming an AI-Native Cloud

DigitalOcean's strategy now extends well beyond traditional cloud hosting.

Earlier this year, the company launched its AI-Native Cloud platform designed for inference and agentic AI workloads. It also acquired Katanemo Labs, adding agentic AI technology to its platform, while expanding GPU infrastructure to support growing customer demand.

The company continues adding larger AI customers, strengthening its management team with new executive hires, and expanding global data-center capacity. Management believes these investments position DigitalOcean to benefit from the next wave of enterprise AI adoption.

What Does Wall Street Think of DOCN Stock?

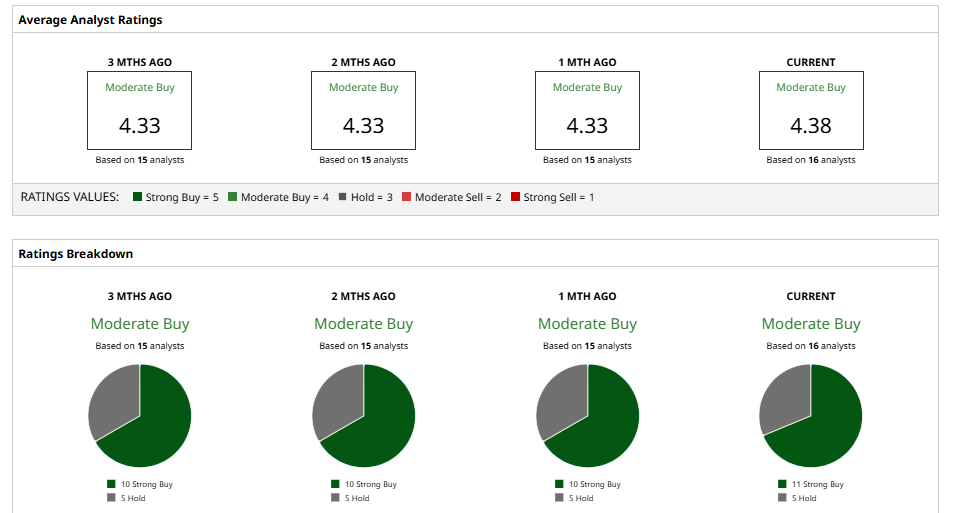

Wall Street remains largely optimistic despite the premium valuation. DOCN stock has a consensus “Moderate Buy" rating, with most analysts recommending investors own shares. Despite the monstrous run, they believe DOCN could climb another 38% from current levels, based on the mean price target of $179. Analysts continue to point to DigitalOcean's accelerating AI business, improving customer mix, expanding ARR, and growing GPU capacity as reasons for optimism.

For long-term investors, the Russell 1000 inclusion reinforces how far DigitalOcean has come. The next challenge is proving that its AI strategy can justify today's premium valuation.

On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/AI%20technology%20concept%20by%20NMStudio789%20via%20Shutterstock.jpg)