Constellation Brands (STZ), which sells Corona and Modelo beers and other drinks, generated strong free cash flow and FCF margins for its latest quarter ended May 31. But investors are wondering if it's undervalued. One attractive play is to sell short out-of-the-money (OTM) puts for a high monthly yield.

STZ closed at $137.47, up slightly, but down after its June 30 quarterly release, when STZ closed at $139.09 per share.

Good and Bad News Relating to FCF

The good news is that Constellation generated $485 million in free cash flow (FCF) on $2.433 billion in sales in Q1. Sales were down slightly (-3.3% YoY), but FCF was up +9% YoY.

More importantly, the FCF margin rose from 17.67% of sales last year to 19.92% this Q1 ending May 31, according to Stock Analysis. That shows that Constellation Brands is squeezing out more cash from its operations as its sales tread water.

The bad news is this: management forecasts that this year its FCF could range between $1.6 billion and $1.7 billion for the fiscal year ending Feb. 28, 2027. Why is that bad news?

This will be lower than its trailing 12-month (TTM) FCF, which was $1.834 billion in Q1, according to Stock Analysis. Moreover, even using a 20% based on analysts' revenue forecasts, FCF won't be higher.

Here's why. Analysts estimate sales this year will hit $9.1 billion and only slightly higher next fiscal year at $9.27 billion. That implies $9.185 billion for the next 12 months (NTM) sales.

So, applying a 20% FCF margin (slightly higher than the TTM 19.92% figure):

$9.185b x 0.20 = $1.837 billion FCF

That is only $3 million over the $1.834 billion Constellation has generated over the past year. This might imply only a slight increase in the stock's fair market value (FMV).

What STZ Could Be Worth

Let's assume the market might be willing to give STZ an FCF yield of 7.50%. That will set a fair market value (FMV) for STZ stock using the FCF projection above.

That is actually better than its present 7.75% FCF yield, based on STZ's market cap today of $23.676 billion):

$1.834b / $23.676b mkt cap = 0.0775 = 7.75% FCF yield

So, here is how the FMV calculation works for STZ:

$1.837b NTM FCF / 0.075 FCF yield = $24.493 billion FMV

That is just 3.45% higher than Constellation's existing market cap of $23.676 billion, according to Yahoo! Finance's calculation.

In other words, the price target for STZ, based on FCF projections, is just 3.45% higher:

$137.47 x 1.0345 = $142.22 Price Target (PT)

However, other analysts are more sanguine about its prospects. Yahoo! Finance reports that the average PT of 23 analysts is $174.64, and Barchart's mean survey PT is $175.30. Similarly, AnaChart's survey of 19 analysts has an average PT of $173.54 per share.

So, maybe there is some upside in STZ stock. It may be based on a higher multiple on its FCF (i.e., a lower FCF yield metric).

However, there is no guarantee that STZ will rise, even though it's at a low point. One way to conservatively play STZ is to sell short cash-secured out-of-the-money (OTM) put options.

Shorting OTM STZ Puts

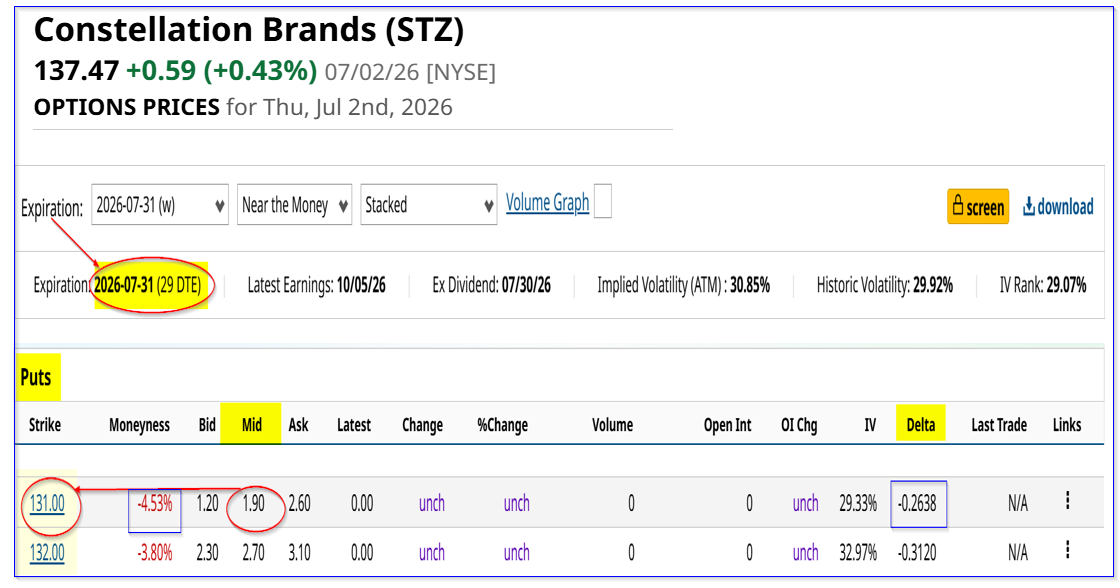

For example, look at the July 31 options expiry period. It shows that the $131.00 STX put strike price, which is 4.7% below yesterday's closing price ($137.47), has a midpoint premium of $1.90 per put contract.

That implies that a 4.7% out-of-the-money (OTM) put contract for the next 29 days has a cash-secured yield of 1.45%:

$1.90 / $131.00 = 0.0145 = 1.45% short-put yield

This means that an investor who posts $13,100 with their brokerage firm as collateral (i.e., $131.00 x 100 shs per put contract), can enter an order to “Sell to Open” 1 put at $131.00. The account will then receive $190.

So, the net yield for 1 month is 1.45% (i.e., $190/$13,100). As long as STZ stays over $131.00 by July 31, the collateral will not be assigned to buy 100 STZ shares.

But, even if that happens, the investor's net breakeven buy-in point is lower:

$131.00 - $1.90 = $129.10 breakeven

That's 6.0% below yesterday's closing price. It also implies that the investor has a good potential upside:

$142.22 / $129.10 = 1.105 -1 = +10.6% upside

Moreover, if an investor can repeat this play each month for the next 12 months, the expected return (ER) is very attractive:

1.45% x 12 = 17.40% 12 mo ER

That is a better play than just holding STZ stock, based on my FCF-based price target.

The bottom line is that STZ may or may not be undervalued. But, for value investors, shorting out-of-the-money cash-secured puts is a very attractive way to play STZ.

On the date of publication, Mark R. Hake, CFA did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Microsoft%20headquarters%20By%20Peter.jpeg)

/NVIDIA%20Corp%20logo%20outside%20building-by%20BING-JHEN_HONG%20via%20iStock.jpg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Amazon%20-%20Image%20by%20bluestork%20via%20Shutterstock.jpg)