CrowdStrike CRWD is scheduled to report its fourth-quarter fiscal 2025 results on March 4, 2025.

Stay up-to-date with all quarterly releases: See Zacks Earnings Calendar.

CrowdStrike anticipates revenues between $1.0287 billion and $1.0354 billion for fourth-quarter fiscal 2025. The Zacks Consensus Estimate for CRWD’s fiscal fourth-quarter revenues is pegged at $1.03 billion, indicating year-over-year growth of 22.28%.

For the fiscal fourth quarter, the company expects non-GAAP earnings per share in the band of 84-86 cents. The Zacks Consensus Estimate for CRWD’s fiscal fourth-quarter earnings is pegged at 85 cents per share, indicating a year-over-year decline of 10.5%.

The consensus mark for CRWD’s fiscal fourth-quarter non-GAAP earnings has remained unchanged at 85 cents over the past 90 days.

Image Source: Zacks Investment Research

CrowdStrike’s earnings beat the Zacks Consensus Estimate in each of the trailing four quarters, the average surprise being 10.3%.

Earnings Whispers for CRWD

Our proven model does not conclusively predict an earnings beat for CrowdStrike this time. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the odds of an earnings beat, which is not the case here. You can see the complete list of today’s Zacks #1 Rank stocks here.

Though CRWD currently carries a Zacks Rank #2, it has an Earnings ESP of 0.00%. You can uncover the best stocks to buy or sell before they are reported with our Earnings ESP Filter.

Factors Likely to Influence CRWD’s Q4 Results

CrowdStrike’s fourth-quarter fiscal 2025 results are likely to reflect the benefits of the continued solid demand for its products, given the healthy environment of the global security market. The increasing number of people logging into employers' networks has triggered a greater need for security and might have spurred the demand for CRWD’s products in the fiscal fourth quarter. A strong pipeline of deals indicates the same.

Stellar revenue growth in subscriptions might have contributed significantly to the fourth-quarter top line. Further, the increasing number of net new subscription customers might have acted as a tailwind.

Moreover, CrowdStrike’s collaboration with Amazon Web Services (“AWS”) is an upside, benefiting the company from its products’ availability on the AWS platform. The expansion in the volume of transactions through Amazon’s AWS Marketplace, growth in co-selling opportunities with AWS salesforce and the uptake of AWS service integrations is likely to have contributed to CRWD’s earnings in the to-be-reported quarter.

In the fourth quarter of fiscal 2025, CRWD achieved C5 compliance from the German Federal Office for Information Security and FedRAMP authorization from the United States. These two certifications are likely to have aided CrowdStrike in securing more contracts from the federal agencies in both countries, contributing to its top-line in the to-be-reported quarter.

CRWD Price Performance & Stock Valuation

In the past year, shares of CRWD have climbed 18.4%, underperforming the Zacks Security industry, Zacks Computer and Technology sector and the S&P 500 index’s growth of 22.5%, 20.1% and 19.1%, respectively. CRWD stock has also underperformed its peers, including CyberArk CYBR, Fortinet FTNT and Check Point Software Technologies CHKP.

1-Year Price Return Performance

Image Source: Zacks Investment Research

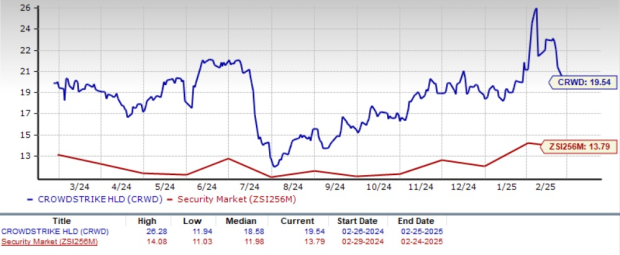

Now, let’s look at the value CRWD offers investors at the current levels. CRWD is trading at a premium with a forward 12-month P/S of 19.54X compared with the industry’s 13.79X, reflecting a stretched valuation.

Forward 12-Month P/S Valuation

Image Source: Zacks Investment Research

Investment Consideration for CrowdStrike

Despite fierce competition, CrowdStrike continues to dominate the cybersecurity space, securing multiple eight-figure contracts in the last reported quarter, proving its ability to attract high-value customers.

A significant driver of new customer addition is the Falcon Flex subscription model, which simplifies security adoption by offering modular, scalable cybersecurity solutions. This flexibility encourages long-term commitments, ensuring steady revenue growth and deep customer integration.

With 45 of the Fortune 50 relying on CrowdStrike, its market influence is undeniable. Its ability to land and expand within enterprise accounts sets it apart from peers, making it one of the most compelling long-term cybersecurity investments.

Conclusion: Buy CRWD Stock for Now

While CRWD's underperformance and stretched valuation can raise investors’ concerns, its strong market position is encouraging. CrowdStrike’s solid offerings across endpoints, cloud workloads, identity and data and subscription-based business model make it a compelling choice for long-term investment. Considering all these factors, we believe it is prudent to invest in the stock.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is among the most innovative financial firms. With a fast-growing customer base (already 50+ million) and a diverse set of cutting edge solutions, this stock is poised for big gains. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Check Point Software Technologies Ltd. (CHKP): Free Stock Analysis Report

Fortinet, Inc. (FTNT): Free Stock Analysis Report

CyberArk Software Ltd. (CYBR): Free Stock Analysis Report

CrowdStrike (CRWD): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).