Walmart’s (WMT) stock dropped by nearly 4% on Wednesday on higher-than-average share and options volume. The world’s largest retailer’s stock has now fallen by more than 19% since hitting an all-time high of $135.15 on May 19. There are several reasons for the six-week correction.

However, yesterday’s decline is most likely due to a report from the sell-side research firm Cleveland Research, which suggested that Walmart has lowered prices to clear excess inventory, resulting in lower same-store sales. Walmart’s temporary move may cause it to miss its Q2 2026 revenue guidance.

In yesterday’s options trading, Walmart’s options volume was 286,828, more than double the 30-day average, and the second-highest daily total in the past three months.

Walmart had 15 unusually active options on Wednesday -- options with volume of 500 contracts or more and expiring in seven days or more -- with calls and puts almost equally split at 7 and 8, respectively.

As for the put/call volume, it was relatively neutral at 0.86. However, the daily metric since the beginning of June has been above 0.86 on only two occasions: 0.98 on June 25 and 0.92 on June 17, suggesting investors are slowly becoming more bearish about Walmart stock.

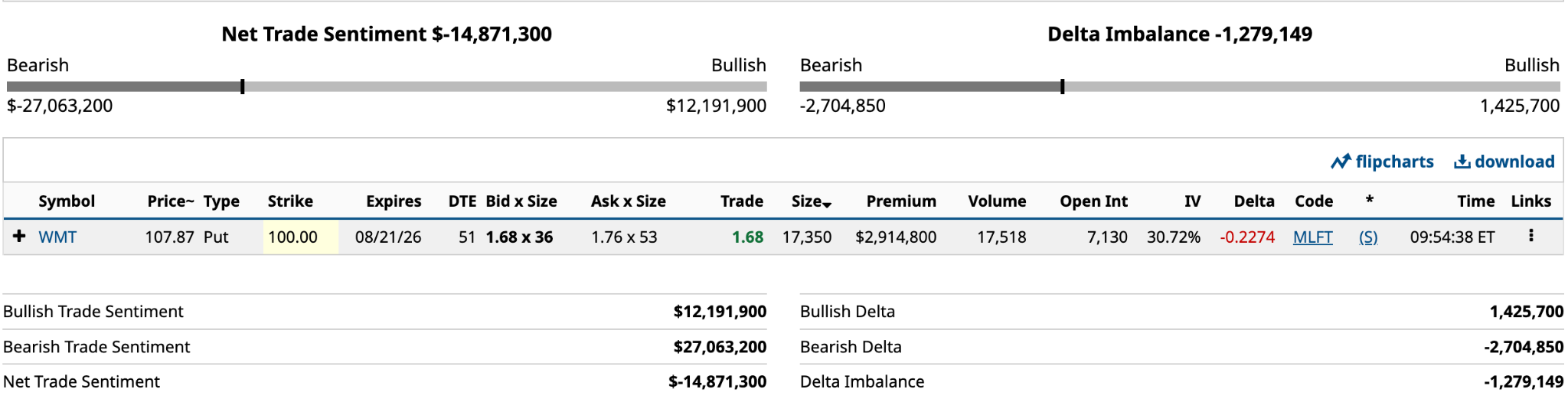

The unusually active option of the 15 that caught my attention from yesterday is the Aug. 21 $100 put. While its Vol/OI (volume-to-open-interest) ratio wasn’t high at 2.65, the 18,894 in volume was.

Today, I’ll take a closer look at the Aug. 21 $100 put and the options strategy a particular trader/investor may have implemented based on it.

The WMT Put Option in Question

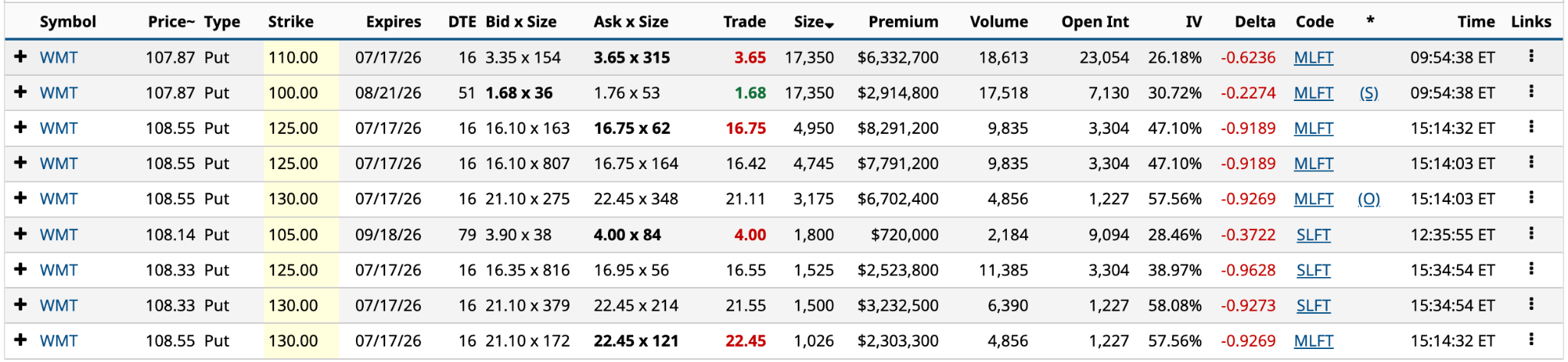

The volume for the Aug. 21 $100 put was the highest of the 15 unusually active options from yesterday. The only other with a volume of 10,000 or more was the July 17 $125 put at 11,385. The 16-day DTE (days to expiration) plays a part in today’s commentary.

Breaking down the 18,894 volume for the Aug. 21 $100 put, I’ll look at the put’s options flow from yesterday.

The one trade yesterday at 9:54 accounted for 92% of the total volume for the Aug. 21 $100 put. There were also a large number of trades ranging from 10 to 100 contracts. But it is the 17,350 trade that piqued my interest. You’ll note the “S,” which indicates it was a sell-to-open trade for premium income. However, the MLFT (multi-leg floor trade) code suggests it is combined with another option.

As you can see from below, there were nine put trades yesterday with volumes of 1,000 contracts or more, including the Aug. 21 $100 put.

The July 17 $110 Put

You’ll notice that a trade for the July 17 $110 put took place at 9:54, the same time as the Aug. 21 $100 put. More importantly, the volume for the July 17 $110 put was 17,350, the same amount as the Aug. 21 $100 put. That’s no coincidence.

These two puts were part of a Short Diagonal Put Spread (or reverse diagonal put spread) options strategy. The strategy is similar to a Bear Put Spread -- a bearish options strategy where you buy a put option and sell a put option at a lower strike price, expecting the share price to be below the lower strike price at expiration -- except that the two puts have different expiration dates. You’re moderately to extremely bullish over the long haul rather than bearish.

In this instance, the investor/trader bought 17,350 July 17 long $110 puts for $6.33 million, and sold 17,350 Aug. 21 short $100 puts for $2.91 million in premium, reducing the net debit by 46% to $3.42 million.

Why would someone do this?

The primary reason is to reduce the cost of the nearer-term put, which is ITM (in-the-money), by $2.13, based on the information as of yesterday’s trades. However, as I write this on Thursday trading, Walmart’s share price is up 2.8% on the day at $111.82. So now both puts are OTM (out of the money).

To do the same trade today, the net debit would be $0.52, based on an ask price of $1.41 for the July 17 $110 put and a bid price of $0.89 for the Aug. 21 $100 put. The spread between the delta for the long put and the short put is 0.2316, down from 0.396 yesterday. That means that for every $1 the share price moves lower, the benefit from the July 17 $110 long put decreases.

At the end of the day, the investor/trader responsible for these two trades likely placed a reverse diagonal put spread bet because Walmart’s share price has been losing ground since the third week of May, and they wanted to protect, or even profit from, the stock’s near-term weakness.

The risk of such a bet is that, should the share price fall to $90, for example, by August 21, they might be assigned the shares, resulting in a $10 paper loss [$100 put strike - $90 share price], less any gains from the July 17 $110 put and any premium collected from the Aug. 21 $100 put. Meanwhile, if the share price jumps to $120 by July 17, the long $110 put will expire worthless, and you will now own a naked short $100 put.

While they can be rolled out and down before expiration, the bet’s not a defined risk. It’s not something I’d be comfortable trading, but professionals would.

On the date of publication, Will Ashworth did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Microsoft%20headquarters%20By%20Peter.jpeg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/NVIDIA%20Corp%20logo%20outside%20building-by%20BING-JHEN_HONG%20via%20iStock.jpg)

/Amazon%20-%20Image%20by%20bluestork%20via%20Shutterstock.jpg)