OppFi Inc. OPFI shares have skyrocketed 194.6% in the past six months, outperforming the 26.1% rally of its industry and the 9.7% rise in the Zacks S&P 500 Composite.

Six Months' Price Performance

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

The stock is trading above its 50-day moving average, indicating bullish sentiment among investors.

Stock Trades Above 50-Day SMA

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

OPFI’s performance significantly surpasses its close competitors, CompoSecure, Inc. CMPO and PAR Technology Corporation PAR. CMPO and PAR shares have gained 38.4% and 25.5% in the past six months.

Given the rise in OppFi’s shares, buying it could be an obvious move. However, the crucial question we should ask is whether now is the right time to invest in OPFI. Let us analyze and find out the right move.

OPFI Gains From Bridging the Gap for Underbanked Customers

Since the pandemic, there has been a significant rise in demand for digital banks, which are more customer-friendly and serve historically underserved banking consumers (subprime and non-prime customers). These customers provide a considerable credit opportunity and are the primary target of multiple neo-banks. Per OppFi, there are nearly 60 million U.S. consumers who are credit marginalized. This shows the large market opportunity that the company can cash in on.

The biggest problem faced by customers is living paycheck to paycheck while trying to enhance their credit score. Traditionally, financing options for these customers have been limited, with high interest rates and poor customer service. In that context, OPFI can underwrite riskier loans while charging less than traditional financial institutions, thereby serving a large part of underbanked customers.

OPFI Stock Looks Undervalued

OppFi shares look cheap and appealing to investors. It is priced at 13.1 times forward 12-month earnings per share, which is lower than the industry’s average of 25.8 times.

When looking at the trailing 12-month EV-to-EBITDA ratio, OPFI is trading at 10.1 times, below the industry’s average of 14.8 times.

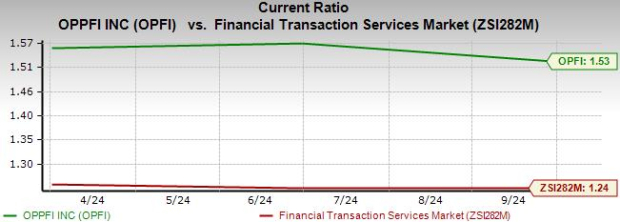

OppFi’s Liquidity Position Beats Industry

In the third quarter of 2024, OPFI’s current ratio of 1.53 outperformed the industry average of 1.24 and increased 4.8% from the year-ago quarter. A current ratio of more than 1 suggests that the company will be able to pay off its short-term obligations easily.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

OPFI’s Strong Top & Bottom-Line Prospects

The Zacks Consensus Estimate for OppFi’s 2024 and 2025 revenues is pegged at $520 million and 547.1 million, implying 2.2% and 5.2% year-over-year growth, respectively. The consensus estimate for OPFI’s 2024 and 2025 earnings per share stands at 86 cents and $1, suggesting 68.6% and 16.3% year-over-year increases, respectively.

OppFi’s Consumer Credit Risk

OPFI’s ability to underwrite riskier loans to serve underbanked customers can acts towards its detriment. If the creditworthiness of consumers deteriorates, the company might have to deal with an increase in charge-offs, thus affecting its bottom line. In a competitive market, consumers will have a rising number of alternative credit platforms to use, resulting in increasing pricing pressure on the neo-banks.

OPFI’s Bet on Bitty Seems Risky

In 2024, OppFi announced its acquisition of a 35% equity interest in Bitty Advance, encompassing its servicing business. OPFI was excited about this buyout as management believed that Bitty would serve as a cornerstone for OPFI’s expansion into a new vertical in small business financing. However, the inherent difficulties of scaling a small business lending platform, coupled with a huge target market, present potential problems.

While the acquired company has shown profitability in the past, hitting the substantial growth mark and seamless integration with OppFi’s platform may require extensive capital and extended time. The yardstick of success in terms of diversification is the realization of expected accretive benefits. Bitty’s failure to meet the standards or the detriment in economic conditions can result in a contraction of the small business lending market, and OPFI’s plan to benefit from diversification and expansion could be compromised.

Analyzing the Right Entry Point for OPFI

A significantly large market of underbanked customers, coupled with a robust liquidity position, benefits OppFi. Healthy top and bottom-line views are promising. A cheaper valuation makes the stock favorable for investing in the long run.

Meanwhile, considering the heightened exposure to credit risks from underwriting riskier loans and the probability of failing diversification and expansion, it is prudent to retain the stock in your portfolio.

OppFi carries a Zacks Rank #3 (Hold) at present. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Only $1 to See All Zacks' Buys and Sells

We're not kidding.

Several years ago, we shocked our members by offering them 30-day access to all our picks for the total sum of only $1. No obligation to spend another cent.

Thousands have taken advantage of this opportunity. Thousands did not - they thought there must be a catch. Yes, we do have a reason. We want you to get acquainted with our portfolio services like Surprise Trader, Stocks Under $10, Technology Innovators,and more, that closed 256 positions with double- and triple-digit gains in 2024 alone.

See Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

PAR Technology Corporation (PAR): Free Stock Analysis Report

OppFi Inc. (OPFI): Free Stock Analysis Report

CompoSecure, Inc. (CMPO): Free Stock Analysis Report

/A%20Palantir%20sign%20displayed%20on%20an%20office%20building%20by%20Poetra_RH%20via%20Shutterstock.jpg)