Even as the business has a strong moat, Palantir (PLTR) stock has been a victim of pessimism in the recent past. A key reason is the company’s loss of some European government contracts, which is likely to impact the company’s international growth.

However, the markets have a tendency to overreact. This presents a good buying opportunity in PLTR stock as overall business momentum remains positive. In recent news, Palantir announced a partnership with Surf Air Mobility (SRFM) to “accelerate the development and commercial release of SurfOS, including OperatorOS, OwnerOS, and SurfOS Enterprise Solutions products.”

Further, the company also announced a deal with Nvidia (NVDA) “for running NVIDIA AI and Nemotron open models in sovereign environments.” These deals add to the company’s growth visibility and underscore the positive underlying business momentum. It’s also worth noting that for Q1 FY26, Palantir signed 206 deals of at least $1 million. As the order intake supports sustained growth, PLTR stock is likely to trend higher.

About Palantir Stock

Founded in 2003 and headquartered in Aventura, Florida, Palantir builds software that empowers organizations to effectively integrate their data, decisions, and operations at scale. The company was initially formed to assist in counterterrorism investigations and operations following 9/11. Currently, Palantir also works with commercial enterprises that face similar challenges when working with data.

Palantir has built four principal software platforms: Gotham, Foundry, Apollo, and Artificial Intelligence Platform. As of December 2025, Palantir had 954 customers, with 54% of FY25 revenue coming from government customers and 46% from the commercial segment. Further, for FY25, 26% of the company’s revenue was from outside the United States.

Palantir has been on a healthy growth trajectory with FY25 revenue increasing by 56% on a year-on-year (YoY) basis to $4.5 billion. For the same period, the company’s operating cash flow was robust at $2.1 billion. The company also reported a total remaining deal value of $11.2 billion as of FY25, which provides clear revenue visibility. Amidst these positives, PLTR stock has corrected by 30% in the last six months, and this seems like a good buying opportunity.

Strong Fundamentals and Robust Growth

As of Q1 FY26, Palantir reported a cash buffer of $8 billion. For the same period, the company’s balance sheet was debt-free. With high financial flexibility, Palantir is positioned to invest aggressively in innovation driven growth.

Earlier this month, Wolfe Research highlighted Palantir as “the most applied enterprise AI software company, with the largest and fastest growth rates in the industry.” With a significant total addressable market, the top-line growth trajectory is likely to remain robust.

Of course, the loss of government contracts in Europe is a concern. However, Palantir reported a U.S. commercial customer count of 615 as of March 2026. On a YoY basis, the customer count increased by 42%. Therefore, the growth potential within the United States for government and enterprise customers is significant.

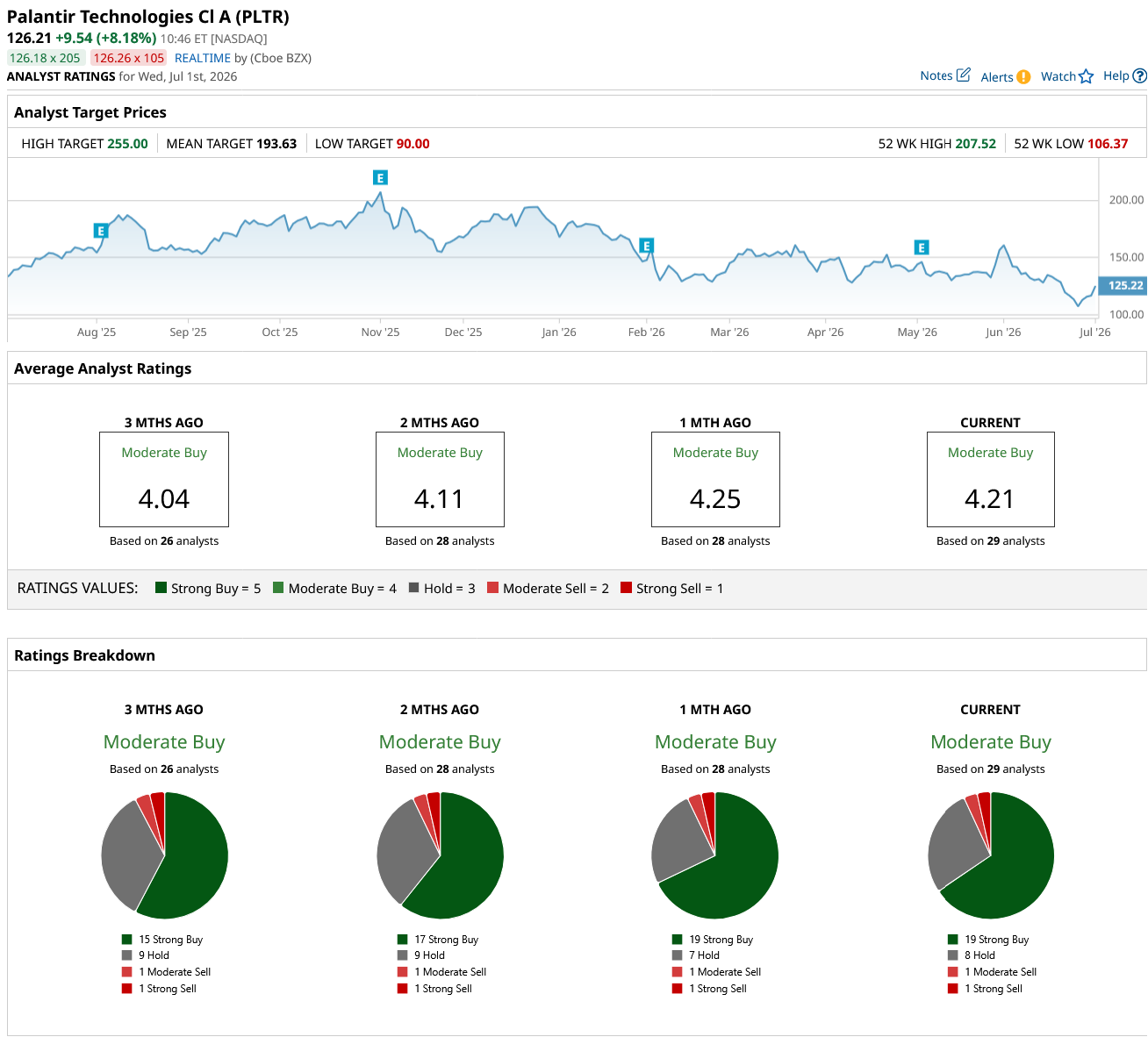

What Do Analysts Say About PLTR Stock?

Based on 29 analysts with coverage, PLTR stock has a consensus “Moderate Buy” rating. While 19 analysts have a “Strong Buy” rating for PLTR stock, eight have a “Hold,” one analyst has a “Moderate Sell,” and one has a “Strong Sell” rating.

The mean price target of $193.63 represents a potential upside of 53% from current levels. Further, the most bullish price target of $255 suggests that PLTR stock could climb as much as 102% from here.

Concluding Views

PLTR stock has been an underperformer in the last 52 weeks. However, with analyst estimates of earnings growth for FY26 and FY27 at 84.13% and 40.52%, respectively, there is a possibility of a strong comeback.

An important point to note is that PLTR stock trades at a valuation premium even after the correction. The premium is justified on the back of high earnings growth and a product moat.

The valuation premium can also be justified by the company’s high cash flow potential. For Q1 FY26, Palantir reported adjusted free cash flow of $925 million. This implies an annualized FCF potential of $4 billion that’s likely to swell further considering the growth trajectory.

On the date of publication, Faisal Humayun Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20close-up%20of%20an%20AMD%20office%20by%20gehapromo%20via%20Adobe%20Stock.jpeg)

/A%20logo%20for%20Bending%20Spoons%20displayed%20on%20a%20smartphone%20screen%20by%20Timon%20via%20Adobe%20Stock.jpeg)

/ServiceNow%20Inc%20building%20in%20Silicon%20Valley-by%20Sundry%20Photography%20via%20iStock.jpg)