Space stocks are back in the spotlight, and this time the story is actually moving the whole sector. On June 29, Rocket Lab (RKLB) shocked investors with an $8 billion cash and stock deal to buy Iridium Communications (IRDM). The transaction is expected to close around mid-2027 and ranks among the biggest commercial space mergers so far. That agreement valued Iridium at a 24% premium and immediately sent Rocket Lab up 15.93%, with Iridium jumping 25.44%.

Recently, space names had dropped roughly 30–45% over the prior month after SpaceX Exploration Technology’s (SPCX) IPO, so this kind of headline was enough to flip sentiment. Planet Labs PBC (PL) quickly joined the rebound, climbing 15.55% in a single session and clawing back part of its recent losses. Now the question is whether Planet Labs can turn this sympathy rally into lasting gains or if it is just catching a short-lived burst of enthusiasm.

Planet Labs’ Financials

Planet Labs is a San Francisco-based company that runs a large fleet of Earth observation satellites and sells frequent imagery and analytics to government and commercial clients.

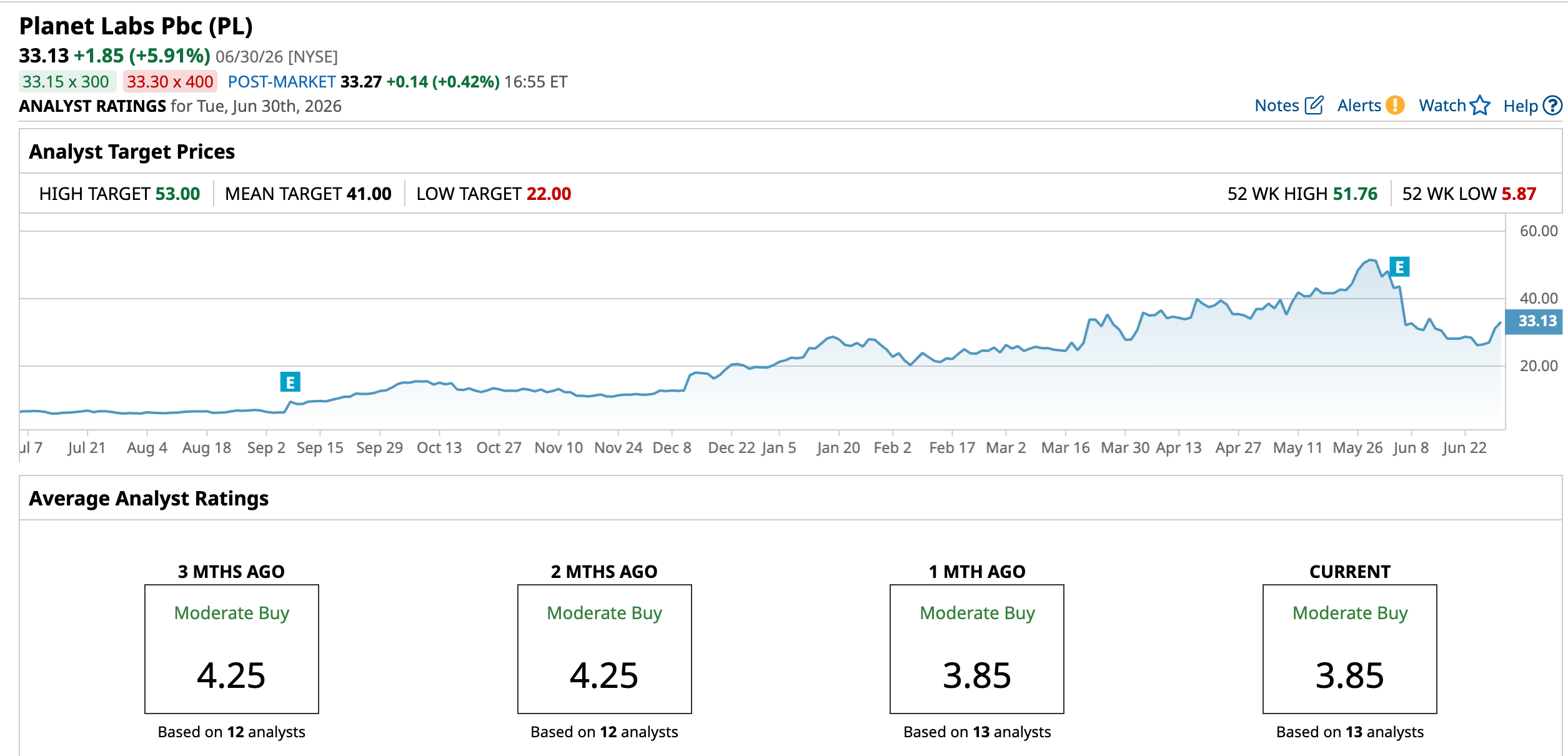

Its stock price has a year-to-date (YTD) performance of 68.1% and a 52-week gain of 443.36%.

This kind of move comes with a heavy valuation. The company’s market cap stands at $11.15 billion, which works out to a price-to-sales multiple of 31.35 times and a price to book ratio of 21.74 times, compared with sector medians of 1.98 times and 3.34 times.

The most recent quarter, reported in April, shows a business still spending to grow but also lifting its revenue base. The period ended April 26 and included earnings per share of −$0.40, missing the consensus estimate of −$0.13 and resulting in an earnings surprise of -207.69%. It also delivered revenue of $94.15 million, up 8.44% from the prior quarter and 42% year-over-year (YOY).

The net income line was slightly negative at $139 thousand, yet net income growth of 8.91% points to gradual improvement even as expansion continues. The backlog of roughly $906 million, up around 72% YOY, gives Planet solid visibility on future work.

PL’s cash flow numbers add more detail. Planet Lab reported operating cash flow of $15.44 million in April 2026, down 88.51%, which signals the impact of timing and investment rather than a settled cash engine. The net cash flow of $140.04 million, up 32.66% from the previous period, shows the balance sheet remains supported.

Planet’s Strategic Wins

Planet Labs recently locked in a sizable extension with the National Geospatial-Intelligence Agency (NGA) under the Luno B IDIQ framework, which includes a one-year $22 million option for Maritime Domain Awareness (MDA). This option backs tools for AI-driven maritime event detection, “dark fleet” tracking, and frequent situational updates for NGA and Defense Innovation Unit users. The same announcement also added a new Global Monitoring Service (GMS) award for crisis response, built around near-daily change detection across different regions.

Pelican 11 is another key piece of the story. Planet has shipped this tech demo satellite to Vandenberg Space Force Base ahead of its launch on SpaceX’s Transporter 17 mission. It sits in the second generation of the Pelican high-resolution fleet and is meant to test technologies aimed at roughly 30 cm class imagery. Earlier Pelican satellites deliver about 50 cm class imagery, so Pelican 11’s job is to prove out new hardware, software, and operations before those upgrades roll into the wider Gen 2 Pelican constellation planned for 2026 and 2027.

Planet is also involved in the Atmospheric Impact of Reentered Spacecraft (AIRS) initiative, led by Astroscale Holdings (ASRHF). This effort brings industry and universities together to study how spacecraft reentry affects the atmosphere as activity in low Earth orbit grows. Planet is sharing non-proprietary manufacturing and material data with researchers at the University of Southampton to help build more accurate atmospheric models.

All of these moves add to recurring government revenue, push Planet toward sharper and more valuable imagery.

Planet Labs’ Analyst Expectations

Planet Labs is heading into an important stretch for investors. The company’s next earnings release is set for September 14, covering the quarter that ends in July 2026, with the average earnings estimate at −$0.18 per share versus −$0.07 a year earlier. That works out to an expected change of -157.14% YOY.

Management is leaning into that growth angle. Planet is guiding revenue in a range of $102 million to $107 million for the second quarter, with the midpoint suggesting around 42% YOY growth.

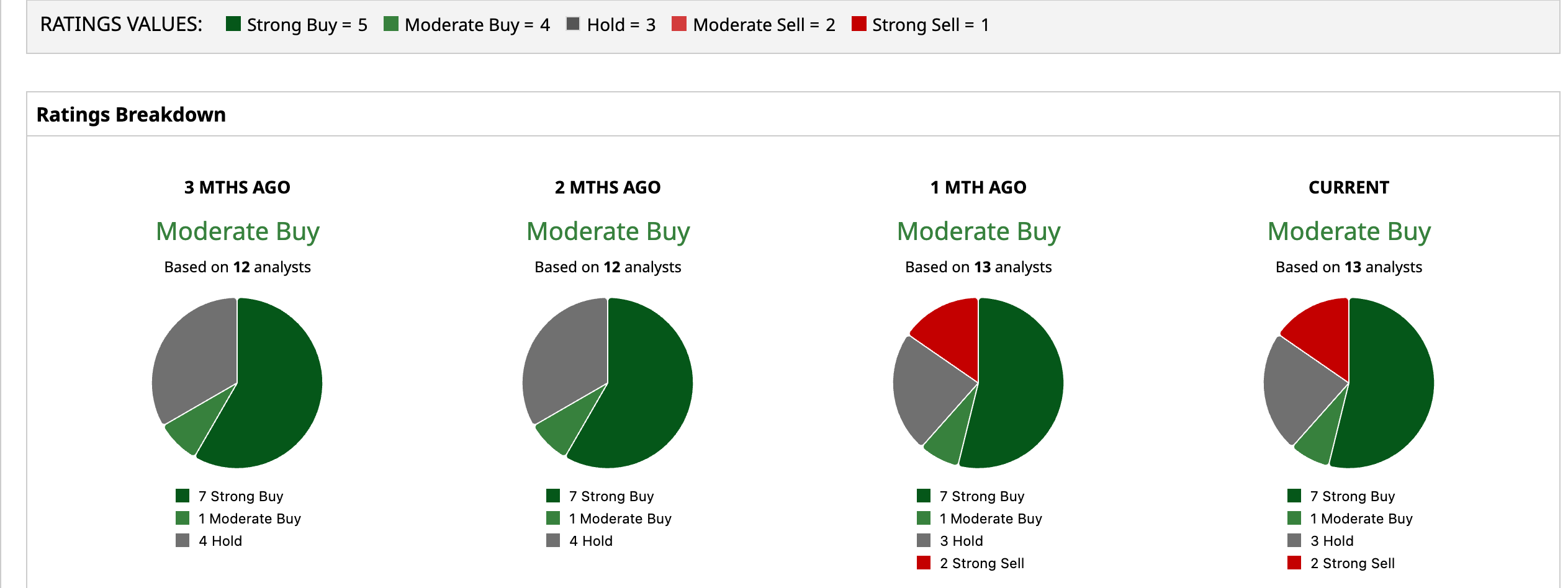

Analysts are tying these pieces together in a generally positive way. A group of 13 analysts has landed on a “Moderate Buy” consensus rating for PL. The average price target is $41.00, which implies roughly 23.76% upside from the stock’s recent level.

Conclusion

Planet Labs’ latest run-up looks less like a random spike and more like the market repricing a company tied to a big space deal. The Rocket Lab Iridium partnership reminded investors that real money is now chasing space infrastructure and data, and Planet’s backlog and contracts give that sympathy move something concrete to lean upon. The revenue is expected to grow about 42%, with a consensus price target $41, and the next leg for the stock will largely hinge on whether Planet can actually deliver on that growth story.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20close-up%20of%20an%20AMD%20office%20by%20gehapromo%20via%20Adobe%20Stock.jpeg)

/A%20logo%20for%20Bending%20Spoons%20displayed%20on%20a%20smartphone%20screen%20by%20Timon%20via%20Adobe%20Stock.jpeg)

/ServiceNow%20Inc%20building%20in%20Silicon%20Valley-by%20Sundry%20Photography%20via%20iStock.jpg)