It was about a year ago that shares of Iovance Biotherapeutics (NASDAQ:IOVA) began to take off. The stock soared on news of approval from the Food and Drug Administration for Amtagvi (lifileucel) as a treatment option for patients with unresectable or metastatic melanoma.

Since hitting a high of more than $18 last February, however, the stock has been declining steadily. And over the past six months, it has fallen by 32%. Entering trading this week, shares of Iovance are worth a little over $6 -- just a fraction of the highs they reached when regulators approved Amtagvi.

Start Your Mornings Smarter! Wake up with Breakfast news in your inbox every market day. Sign Up For Free »

What is wrong with Iovance and why isn't it trading at a higher valuation? Could this be a great buying opportunity for investors, or is the healthcare stock in danger of falling even lower this year?

Why aren't investors more excited about Iovance?

There was a sharp decline in Iovance's share price in early November when it posted its most recent quarterly results. While the company reported "significant demand" for its recently approved treatment, sales totaled $58.6 million for the quarter and were well short of the $147.6 million in expenses that the company incurred for the period, which ended on Sept. 30, 2024.

The company projects that for 2025, its revenue will be around $450 million to $475 million. But even that may not be enough to keep the business from incurring a loss. In just the past nine months alone, the company had incurred around $400 million in expenses, and its costs are likely to rise as it commercializes Amtagvi and rolls it out to more markets.

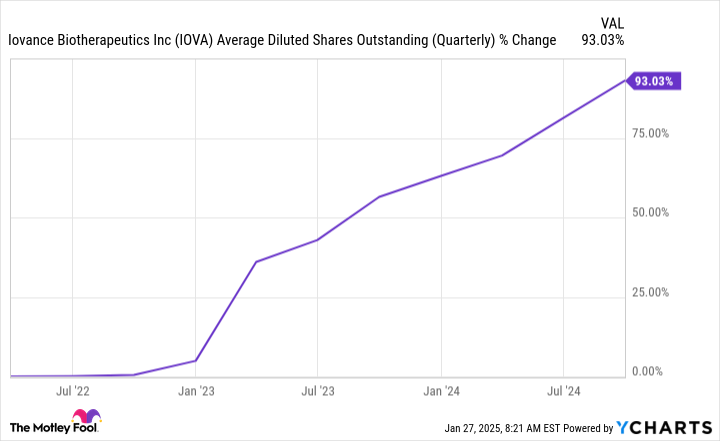

And a lack of a profitability isn't the only problem for investors, as they may need to brace for more dilution ahead.

Iovance is burning through a lot of cash

Over the course of Iovance's past three quarters, the company has burned through a total of $279.7 million. This is before factoring in capital expenditures and only looks at its day-to-day operating activities. That's a problem because Iovance only reported $397.5 million in cash, cash equivalents, and investments as of the end of September. That's not a huge amount of liquid assets, especially given that it may need a lot more cash to grow its business in the months ahead.

The company has been drastically increasing its share count, and the concern for investors is that more stock offerings could be inevitable in order to ensure it has sufficient cash to expand its operations.

IOVA Average Diluted Shares Outstanding (Quarterly) data by YCharts

As more shares hit the market, that could create an excess of supply, resulting in a declining stock price. Unless there's a lot of excitement around the business, which leads to more bullishness and buying activity among investors, large or frequent offerings may put the stock on a persistent, downward trajectory.

Is Iovance stock worth the risk?

Iovance isn't profitable right now and may not be in 2025, and it can still be burning through plenty of cash along the way. But investors shouldn't forget this is still a business in its early growth stages. And by 2029, Amtagvi may be generating as much as $846 million in revenue based on analyst projections for the treatment.

At a market capitalization of less than $2 billion, Iovance could make for an underrated buy right now. This isn't a risk-free investment by any means, but given the potential for Amtagvi and with Iovance still conducting more clinical trials involving lifileucel, there may be plenty of reasons to remain bullish on the stock in the long run.

If you're willing to take on some risk and can be patient with the stock, Iovance may be worth buying as it has the potential to generate some great returns given its modest valuation.

Don’t miss this second chance at a potentially lucrative opportunity

Ever feel like you missed the boat in buying the most successful stocks? Then you’ll want to hear this.

On rare occasions, our expert team of analysts issues a “Double Down” stock recommendation for companies that they think are about to pop. If you’re worried you’ve already missed your chance to invest, now is the best time to buy before it’s too late. And the numbers speak for themselves:

- Nvidia: if you invested $1,000 when we doubled down in 2009, you’d have $334,473!*

- Apple: if you invested $1,000 when we doubled down in 2008, you’d have $45,122!*

- Netflix: if you invested $1,000 when we doubled down in 2004, you’d have $524,100!*

Right now, we’re issuing “Double Down” alerts for three incredible companies, and there may not be another chance like this anytime soon.

*Stock Advisor returns as of January 27, 2025

David Jagielski has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Iovance Biotherapeutics. The Motley Fool has a disclosure policy.

/Nvidia%20logo%20and%20sign%20on%20headquarters%20by%20Michael%20Vi%20via%20Shutterstock.jpg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)