/AI%20(artificial%20intelligence)/AI%20by%20TierneyMJ%20via%20Shutterstock.jpg)

After a brutal June selloff in many of the market's biggest tech and artificial intelligence (AI) stocks, investors have started looking beyond the usual mega-cap names. With most of Big Tech trading in the red amid profit-taking and valuation concerns, the companies supplying the AI ecosystem have quietly continued to outperform.

One of these names is Jabil (JBL), a manufacturing and AI infrastructure specialist. JBL stock has soared 68% year-to-date (YTD) and 66% in the past six months alone, fueled by explosive demand for AI servers, networking equipment, and data-center infrastructure. The company reported a strong third quarter, and now investors are evaluating whether this under-the-radar AI stock still has room to run.

AI Infrastructure Continues to Fuel Growth

Jabil is not a pure-play AI company. It is an electronics manufacturing services (EMS) company. Jabil designs, manufactures, assembles, tests, and integrates electronic products for customers across multiple industries. Its end markets include AI and cloud data centers, networking and telecommunications, healthcare, automotive, consumer electronics, and industrials.

In the third quarter of fiscal 2026, revenue increased 12% year-over-year (YOY) to $8.8 billion. Core operating income reached $504 million, while core operating margin expanded to 5.8%. Core diluted EPS also climbed 24% YOY to $3.16. Jabil’s diversified business benefits it more than being just a pure-play AI company. Management emphasized that revenue strength wasn't concentrated in a single business but was broad-based across the company's portfolio.

The Intelligent Infrastructure segment, in particular, has become the company's fastest-growing and most profitable business thanks to the AI boom. It generated $4.2 billion in revenue during the quarter, an increase of 21% YOY. This segment involves the manufacturing of hardware used to build modern cloud and AI data centers. The segment includes three major end markets. Capital equipment and cloud and data-center infrastructure both posted double-digit growth, while networking and communications revenue jumped more than 50%.

Management now projects the Intelligent Infrastructure segment to generate a 32% YOY increase in revenue to $4.9 billion in Q4. Not only that, Jabil now expects around $13.6 billion in AI-related revenue during fiscal 2026, an increase of 50% over fiscal 2025. Jabil’s exposure to multiple areas of AI infrastructure — including compute, storage, networking, optics, power systems, liquid cooling, and rack-level integration — is the reason for this upbeat outlook.

AI might be the reason investors are pouring money into JBL stock now, but its other businesses are providing stability. Notably, Regulated Industries generated $3.2 billion, while Connected Living & Digital Commerce brought in $1.4 billion in revenue. Similarly, Automotive and Transportation exceeded expectations, fueled by stronger export demand from China, industry consolidation, and growth in powertrain-agnostic vehicle platforms. The company now expects full-year revenue to be around $4.4 billion. Digital Commerce remains one of the company’s higher-margin businesses, supported by automation, robotics, retail technology, and warehouse solutions. It is projected to bring in $2.7 billion in revenue for the fiscal year.

Growth Is Being Driven Without Heavy Capital Spending

Another appealing reason why Jabil shouldn’t stay under-the-radar is its capital-light operating model. The company is driving growth without heavy capital spending. It expects capital expenditures to remain between 1.5% and 2% of revenue in fiscal 2026.

Interestingly, Jabil focuses on manufacturing and integration services while expanding capacity only where customer demand is already visible. The company also generated adjusted free cash flow of $359 million in the quarter, with a target of more than $1.4 billion for the year to support AI growth. The balance sheet also remains healthy, with $1.4 billion in cash at the end of Q3.

For the full fiscal year, management has forecast 17% YOY growth in revenue, with core diluted EPS of $12.70. Similarly, analysts predict Jabil’s earnings to increase by 32% in fiscal 2026 to $11.71, followed by 33% growth to $15.58 per share in fiscal 2027.

Why Jabil Shouldn’t Be Overlooked

While AI is the main growth engine for the company now, Jabil’s diversified business is its biggest strength. Most AI companies are dependent on the fact that AI capex will continue growing at today’s pace or even higher. However, even if AI spending eventually slows, Jabil’s businesses with healthcare, automotive, industrial manufacturing, and digital commerce can continue generating revenue. On the downside, Jabil won’t grow as explosively as a pure AI company.

That brings us to valuation. The question now is whether JBL stock’s 68% YTD rally has made shares overpriced. While investors’ optimism has pushed the forward price-to-earnings (P/E) multiple to around 30 times, Jabil has compelling factors like accelerating AI revenue, expanding profit margins, robust free cash flow generation, and diversified exposure across multiple end markets. The combination of high-growth AI exposure and diversified cash-generating businesses is the reason I believe Jabil shouldn’t be overlooked.

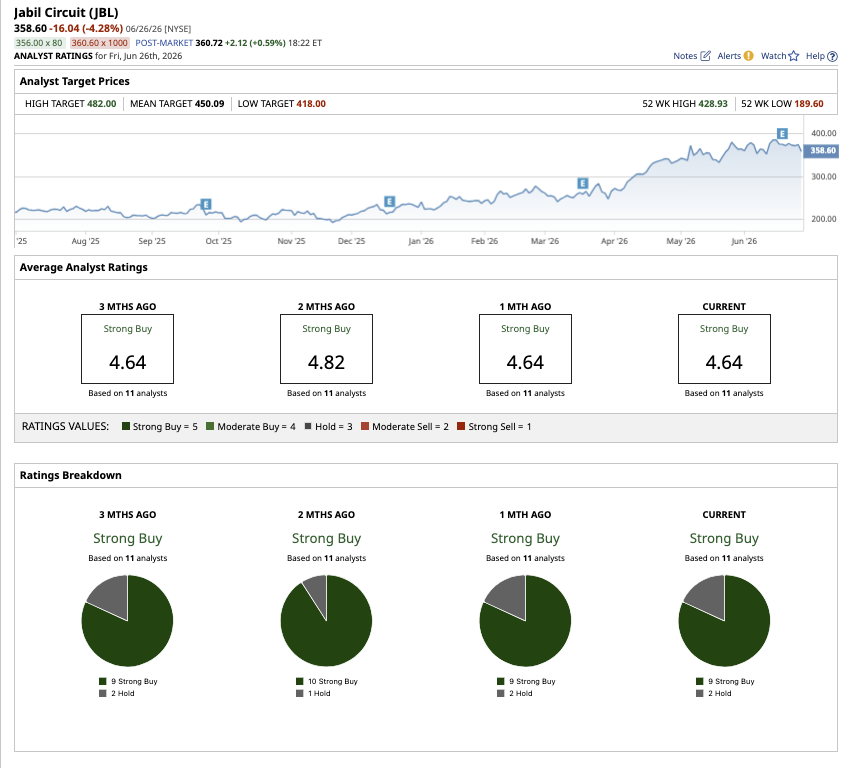

Overall, JBL stock remains a consensus “Strong Buy” on Wall Street. Of the 11 analysts covering the stock, nine rate it a “Strong Buy” while two analysts rate it a “Hold.” The average target price of $449.18 suggests potential upside of 17% from current levels, while the high price estimate of $482 implies the stock could climb as much as 26% over the next 12 months.

On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/The%20CrowdStrike%20logo%20on%20an%20office%20building%20by%20bluestork%20via%20Shutterstock.jpg)

/A%20concept%20image%20showing%20a%20lightbulb%20with%20planet%20earth%20in%20a%20mossy%20green%20background%20by%20Capt_Pic%20via%20Shutterstock.jpg)

/An%20image%20of%20a%20Tesla%20humanoid%20robot%20in%20front%20of%20the%20company%20logo%20Around%20the%20World%20Photos%20via%20Shutterstock.jpg)