/A%20SoFi%20logo%20on%20an%20office%20building%20by%20Tada%20Images%20via%20Shutterstock.jpg)

After losing a significant value, falling more than 45% from its 52-week high, SoFi (SOFI) stock has been consolidating in a tight range over the past several weeks. Investors have grown cautious about the company's premium valuation and the slowing growth of one of its capital-light businesses.

Short-Term Concerns Mask SoFi's Strong Execution

Investor sentiment has been weighed down by slower growth in SoFi's non-lending business, particularly its technology platform. SoFi’s growing fee-based, capital-light businesses diversify its revenue beyond lending, reduce credit risk, and enable the company to command a premium valuation. Thus, the weakness in this segment significantly weighed on its share price.

However, those concerns have overshadowed SoFi’s impressive performances and solid long-term growth potential. Despite these concerns, SoFi delivered an impressive first quarter. Adjusted net revenue climbed 41% year-over-year (YoY), accelerating from 37% growth in the previous quarter. The results suggest that customer demand remains resilient even amid a challenging macroeconomic environment.

Lending was SoFi's primary revenue driver, producing almost $690 million in net interest income. At the same time, its non-lending segments, including credit card interchange fees, brokerage income, Loan Platform Business (LPB) revenue, referral fees, and loan origination fees, generated approximately $390 million. Although growth in the technology platform moderated, overall fee-based revenue still rose by 23%, reflecting continued momentum across SoFi's diversified financial ecosystem.

SoFi’s Strengthening Customer Value Augurs Well for Growth

One of SoFi's biggest competitive advantages is its ability to attract new members while encouraging existing customers to use more products.

During the first quarter, SoFi added 1.1 million new members, taking total membership to 14.7 million, up 35% YoY. Product adoption grew even faster, with 1.8 million new products added, lifting the total to 22.2 million, a 39% increase. Faster product growth than member growth signals that customers are increasingly adopting multiple SoFi services.

Cross-selling metrics support this trend. Around 43% of new products were opened by existing members, up from 40% in the prior quarter and 36% a year earlier. Higher cross-sell rates improve customer retention, increase lifetime value, and support stronger long-term profitability.

LPB Adds Strategic Flexibility

SoFi's Loan Platform Business (LPB) provides a structural advantage over traditional lenders. Instead of holding every loan on its balance sheet, the company can either retain loans to earn recurring interest income or distribute them through its platform to generate fee-based revenue with no credit risk.

The business continues to gain momentum. During the quarter, SoFi secured $3.6 billion in new commitments from three institutional partners, highlighting growing demand for its loan origination platform. As LPB expands, it could become an increasingly meaningful source of high-margin, capital-light revenue.

Lending and Deposits Support Long-Term Growth

While SoFi is diversifying its revenue streams, its lending business posted record loan originations across every major category. Personal loans reached a record $8.3 billion, student loan originations more than doubled to $2.6 billion, and home loans climbed to $1.2 billion.

Another key strength is its rapidly growing deposit base. Deposits increased by $2.7 billion during the quarter to $40.2 billion. A larger deposit base lowers funding costs, supporting higher net interest margins and improving profitability.

The Bottom Line on SOFI Stock

While the slowdown in its tech platform business has weighed on investor sentiment, SoFi's rapid member growth, rising product adoption, expanding fee-based revenue, record lending activity, and a growing deposit base all point to a solid long-term outlook.

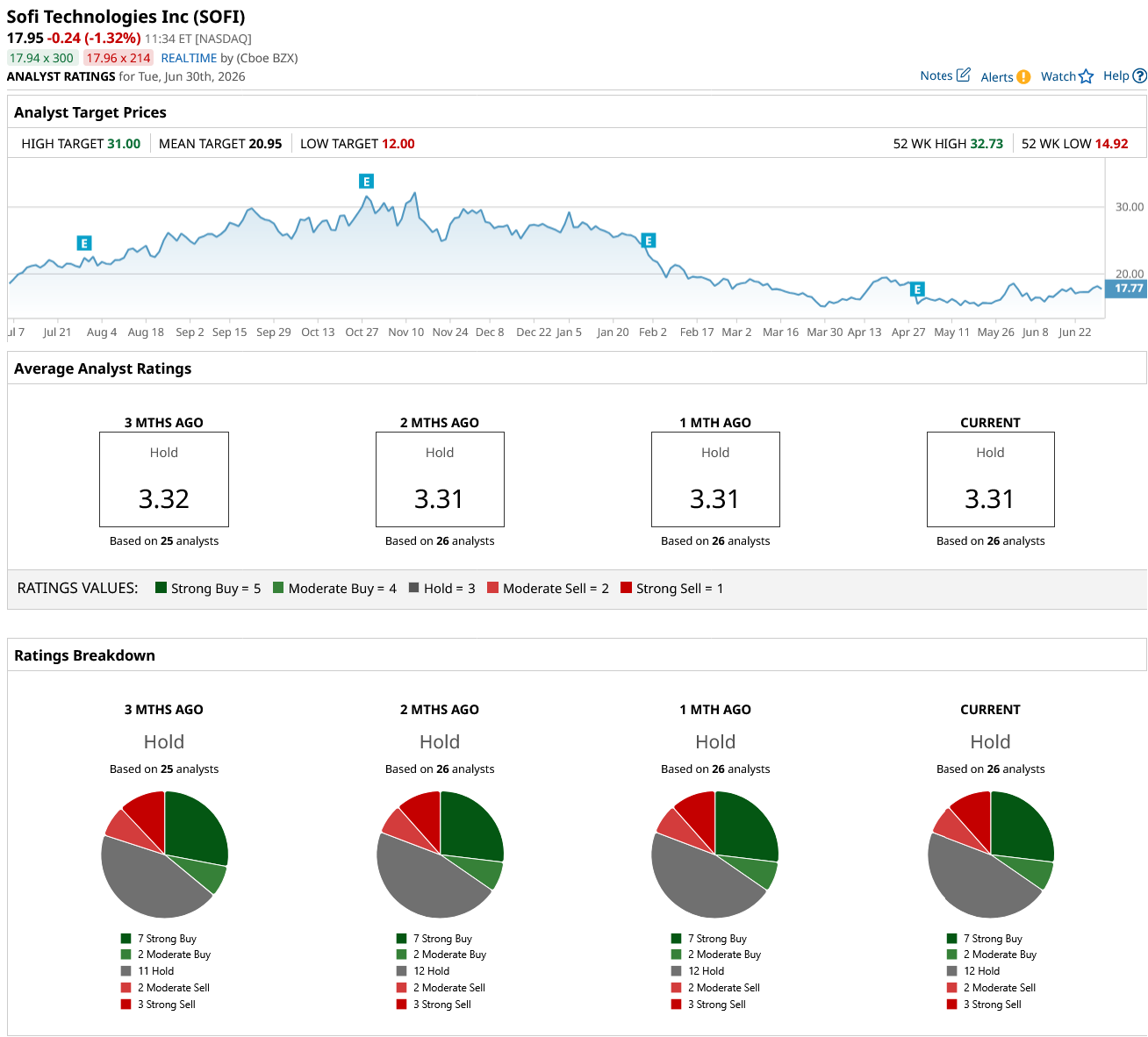

Analysts rate SOFI stock a consensus “Hold.” However, SoFi’s business is becoming more diversified and profitable. Moreover, the company continues to execute well, suggesting that the recent period of share price consolidation after a sharp decline could be an attractive buying opportunity for long-term investors.

On the date of publication, Sneha Nahata did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/An%20Intel%20sign%20out%20front%20of%20a%20corporate%20office%20by%20wolterke%20via%20Adobe%20Stock.jpeg)

/Alibaba%20by%20testing%20via%20Shutterstock.jpg)

/Alphabet%20(Google)%20Image%20by%20Markus%20Mainka%20via%20Shutterstock.jpg)