/Space/Planet%20earth%20with%20flying%20rocket%20by%20Sergey%20Mironov%20via%20Shutterstock.jpg)

Credo Technology (CRDO) is a small semiconductor company that just reported blowout growth, tripling revenue last year. Now analysts say it could get another boost from SpaceX (SPCX) moving into “neocloud” services, which means if SpaceX becomes a cloud/data center provider, Credo may sell a lot of cables and optics.

GF Securities recently argued that SpaceX is evolving toward a neocloud business model. If that thesis proves correct, Credo Technology could emerge as one of the biggest beneficiaries. The bank also initiated a “Buy” rating for CRDO.

The math is simple behind this theory. Modern AI data centers require enormous amounts of high-speed connectivity. Credo specializes in exactly that market. Its active electrical cables, optical connectivity products, and networking solutions help move data across massive AI clusters.

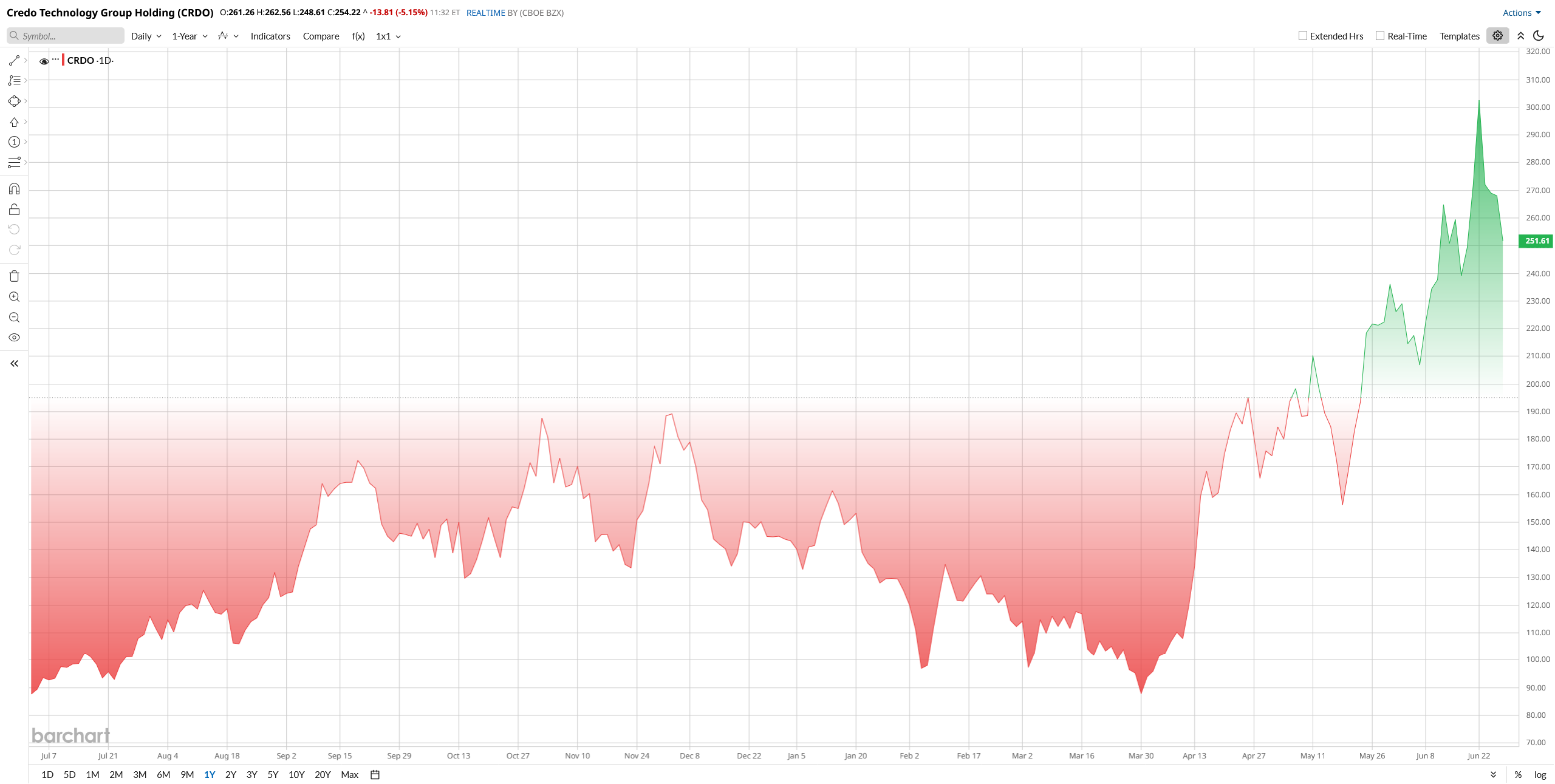

CRDO stock has soared 165% over the past year. The question now is whether the SpaceX opportunity can fuel the next leg higher.

Credo's Business Is Firing on All Cylinders

Before discussing SpaceX, it's worth looking at what Credo is already accomplishing.

The company reported fiscal fourth-quarter revenue of $437 million. That was up 157% year-over-year (YoY) and ahead of analyst expectations of roughly $432 million.

Adjusted earnings came in at $1.16 per share. Analysts were expecting about $1.03 per share. In other words, Credo beat on both revenue and earnings.

Adjusted net income reached $226.7 million. Cash and short-term investments climbed to $1.4 billion. Free cash flow totaled $177.5 million during the quarter.

CEO Bill Brennan summed up the year well. Revenue more than tripled to $1.3 billion during fiscal 2026, while non-GAAP net income increased more than fivefold to $662 million.

Management guided for fiscal first-quarter revenue between $465 million and $475 million. That outlook came in slightly ahead of Wall Street expectations and reinforced the company's strong growth story.

Why SpaceX Could Become a Major Growth Driver

SpaceX is best known for rockets and satellites. But analysts increasingly believe the company is becoming something more.

GF Securities recently highlighted SpaceX's growing ambitions in AI infrastructure and cloud computing. The firm believes the company is shifting toward a neocloud model that could require massive investments in data center hardware and networking equipment.

That is where Credo enters the picture.

AI data centers need high-bandwidth connectivity to move information between thousands of GPUs. Credo's products are specifically designed for those workloads.

If SpaceX continues building large-scale AI infrastructure, demand for Credo's connectivity solutions could rise significantly.

Investors appear to be embracing that possibility. CRDO stock recently pushed to new highs following bullish analyst commentary tied to both AI demand and emerging neocloud opportunities.

Importantly, SpaceX is not the company's only opportunity. Hyperscalers continue expanding AI capacity, and enterprise AI deployments are still in the early innings.

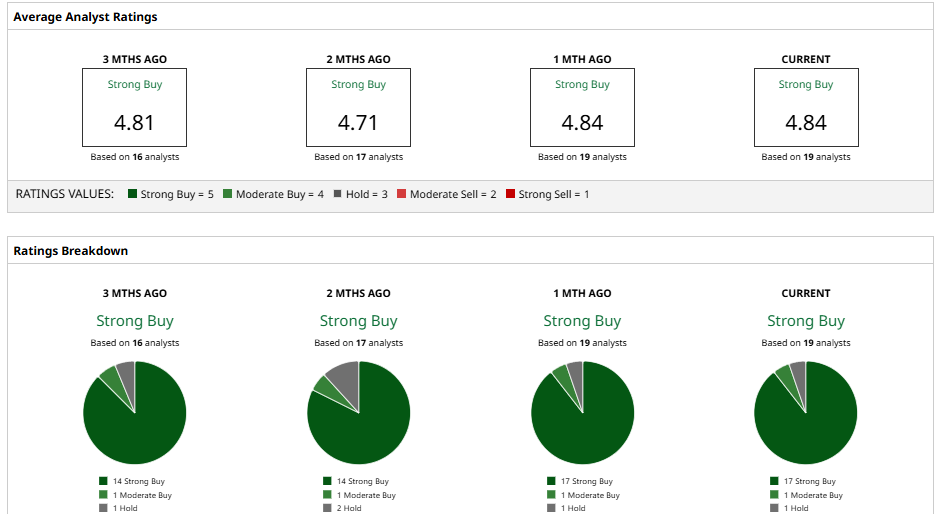

What Wall Street Thinks of CRDO Stock

Analysts remain overwhelmingly bullish. Stifel recently raised its price target to $350 and maintained a “Buy” rating. The firm believes optical networking products could become a major revenue driver over the next several years.

Evercore ISI initiated coverage with an “Outperform” rating and a $325 target. Analysts highlighted Credo's expanding role in AI infrastructure.

TD Cowen raised its target to $260 while pointing to strong margins and confidence in management's outlook.

Overall, the consensus rating on CRDO stock remains “Strong Buy.” The mean price is targeted at $277.47, which suggests a moderate 10% upside potential.

While price targets vary, most analysts agree on one point. Credo sits at the center of several powerful trends, including AI infrastructure expansion, optical networking adoption, and potentially the emergence of SpaceX as a neocloud operator.

If that neocloud thesis plays out, Credo could become one of the biggest winners in the next phase of AI infrastructure spending.

On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Renewable%20Energy%20by%20Yuri%20Hoya%20via%20Shutterstock.jpg)

/A%20Palantir%20sign%20displayed%20on%20an%20office%20building%20by%20Poetra_RH%20via%20Shutterstock.jpg)