Gorilla Technology (GRRR) has given investors a compelling reason to pay attention. The company recently announced a new AI compute infrastructure contract worth up to $2.5 billion over five years. For a company that generated just over $100 million in revenue last year, that number is massive.

The timing is also notable. Gorilla just reported another quarter of strong growth, topped Wall Street revenue expectations, improved its cash position, and raised full-year guidance. The latest contract adds another layer to the story. It gives investors greater visibility into future revenue and reinforces management's strategy of expanding beyond security software into AI infrastructure.

While execution risks remain, Gorilla is building a backlog of large AI-related projects that could transform the company's financial profile over the next several years.

About GRRR Stock

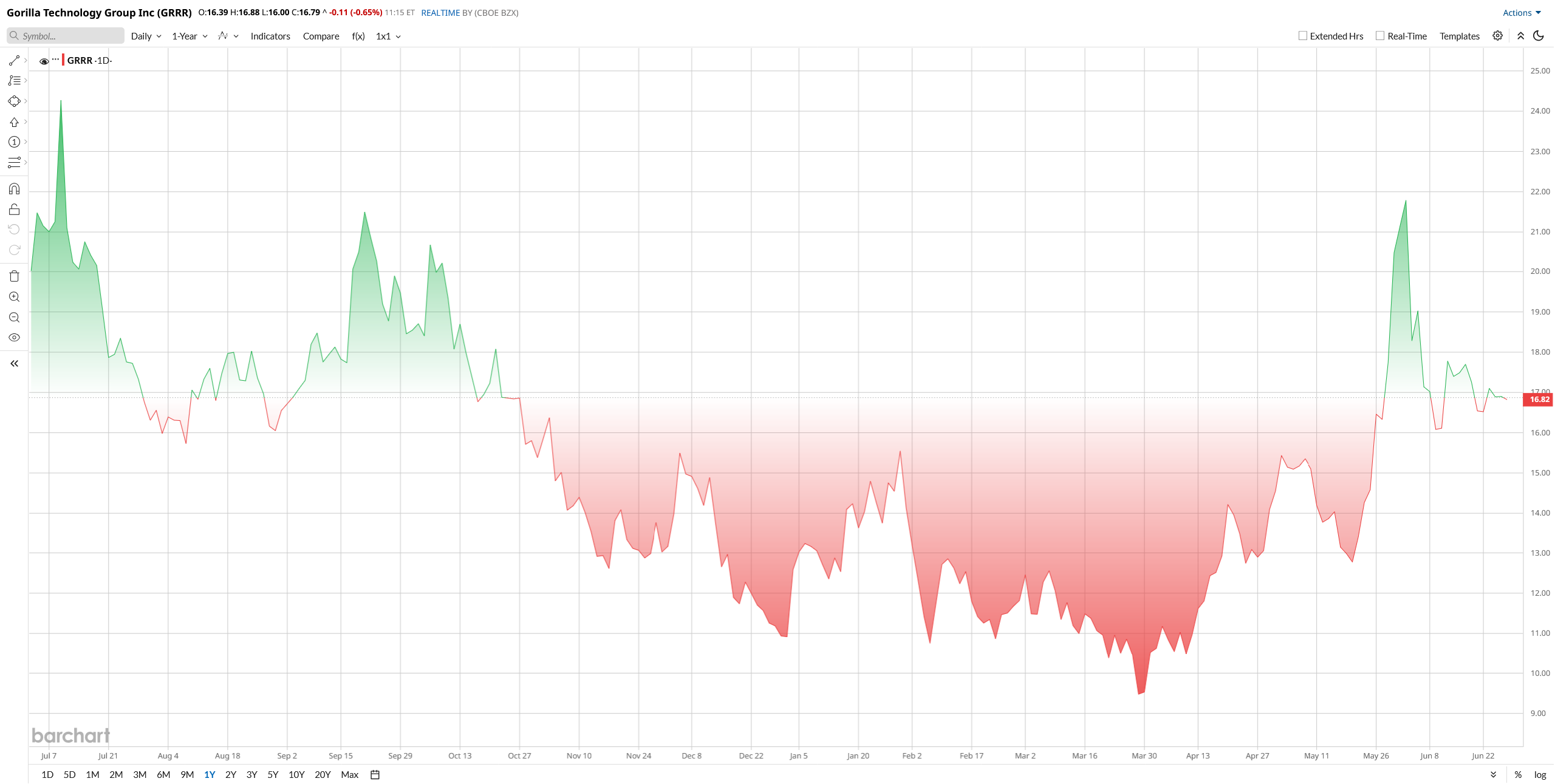

GRRR stock has surged more than 52% year-to-date (YTD) in 2026, fueled by major AI infrastructure wins, expanding data center projects, and rising revenue guidance.

Even after the rally, valuation remains attractive compared to many AI-focused peers. Gorilla trades at roughly 12.7 times forward earnings. That is well below the technology sector median, which sits above 25 times forward earnings. The stock also trades at a price-to-sales ratio of around 4 times, below many fast-growing AI infrastructure companies.

Considering analysts expect strong earnings growth over the next two years, the valuation does not appear stretched.

Gorilla's Business Is Accelerating

Gorilla Technology develops AI-powered security, analytics, and infrastructure solutions for governments and enterprises. Over the last year, management has increasingly focused on AI data centers and GPU-as-a-service offerings (GPUaaS), positioning the company to benefit from surging global demand for AI computing capacity.

That shift is starting to pay off. In the first quarter of 2026, Gorilla generated revenue of $28.2 million, up 55% from a year ago. The company reported an adjusted loss of $0.18 per share. Revenue exceeded analyst expectations, while results also highlighted improving operating cash flow and a rapidly expanding contract pipeline.

CEO Jay Chandan said the company is "building capacity, signing contracts, collecting cash, and putting infrastructure on the ground." Investors appear to be buying into that vision.

Management is essentially building an AI infrastructure platform across several high-growth regions. If these projects move forward as planned, Gorilla could become a significantly larger company than it is today.

The company now expects full-year 2026 revenue between $160 million and $200 million, well above prior expectations.

The $2.5 Billion Opportunity

The biggest catalyst arrived this month. Gorilla announced a five-year AI compute infrastructure contract expected to generate approximately $2.5 billion in revenue. The project will deploy roughly 1,000 advanced GPU servers at the NeutraDC Batam data center in Indonesia.

Management expects the initial deployment phase alone to contribute roughly $1.3 billion of revenue over the life of the contract.

More importantly, this is not simply a memorandum of understanding or a future possibility. It is a contracted business that provides long-term revenue visibility.

For a company of Gorilla's size, a contract worth multiple billions of dollars has the potential to reshape future growth expectations.

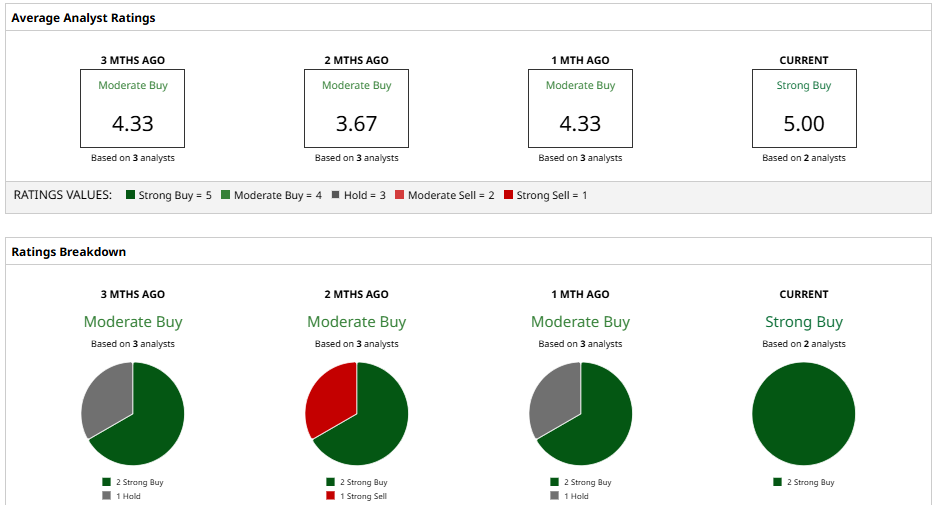

What Wall Street Thinks of GRRR Stock

Analysts remain bullish on Gorilla's prospects. Cantor Fitzgerald recently raised its price target to $40 from $31 and maintained an “Overweight” rating. The firm cited growing confidence in Gorilla's AI data center contracts and revenue outlook.

Northland Securities also raised its target price to $40 while keeping an “Outperform” rating. Analysts there described demand for AI data centers as a "tidal wave" and pointed to Gorilla's expanding project pipeline.

According to Barchart data, GRRR stock carries a consensus “Strong Buy” rating. The average analyst target sits around $40, implying substantial upside of 135% from recent trading levels.

On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Renewable%20Energy%20by%20Yuri%20Hoya%20via%20Shutterstock.jpg)

/A%20Palantir%20sign%20displayed%20on%20an%20office%20building%20by%20Poetra_RH%20via%20Shutterstock.jpg)