Howdy market watchers!

The end of the month and end of the second quarter is almost here! Commodity markets experienced another volatile week as traders balanced improving U.S. crop conditions, shifting weather forecasts, export demand, geopolitical developments, and energy market volatility. Grain markets remained largely defensive despite isolated weather concerns, while cattle futures continued to trade near historically strong levels with cash trade advancing. Energy markets reversed sharply lower after Middle East tensions eased, providing some relief for fuel users across agriculture.

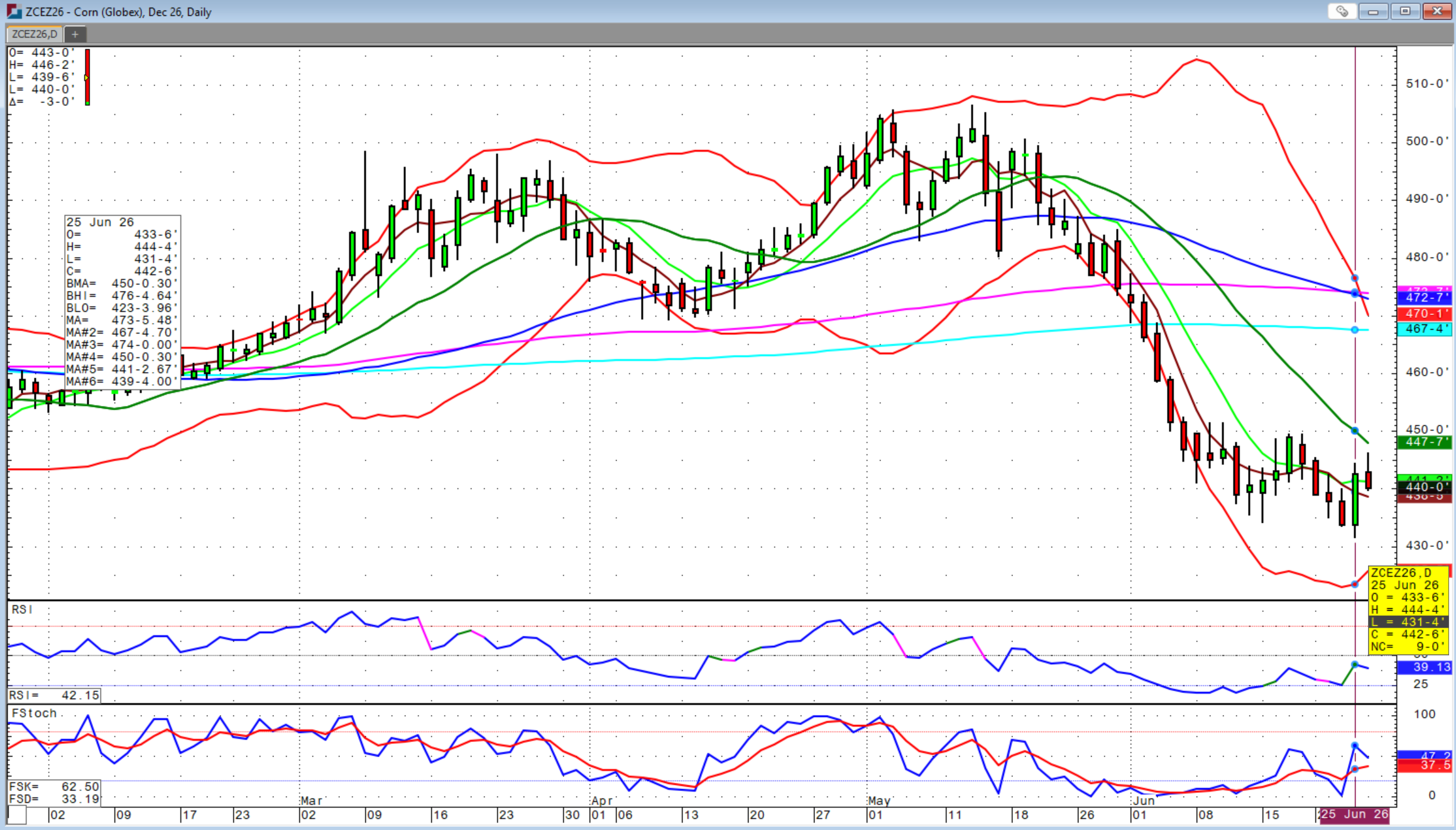

Corn futures finished the week under pressure as nearly ideal growing conditions across much of the Corn Belt encouraged expectations for another large U.S. crop. Frequent rainfall combined with moderate temperatures has supported crop development throughout Iowa, Illinois, Indiana, Nebraska, and portions of Minnesota. USDA crop ratings remain among the strongest seen in recent years, and traders have become increasingly comfortable with the potential for above-trend yields if favorable weather continues through pollination during July. Export demand continues to provide some underlying support, but aggressive competition from South America has limited buying interest from international importers. Brazil continues to offer competitively priced corn into world markets following another sizeable second-crop harvest.

Managed money funds have also continued reducing long positions established earlier this spring. Liquidation from speculative traders added additional selling pressure during several trading sessions this week. Looking ahead, weather during the first half of July will likely remain the single largest driver of corn prices. Any shift toward excessive heat or widespread dryness during pollination could quickly change market sentiment. Until then, traders appear comfortable pricing in the potential for another large harvest.

Soybean futures traded sideways to slightly lower during the week as improving weather offset supportive export news. Timely rainfall across much of the Midwest has significantly reduced concerns surrounding early-season crop stress. Soybeans typically have greater ability to recover from weather adversity than corn, leading many analysts to maintain optimistic production forecasts. Export business remains mixed. Chinese purchasing activity has improved modestly, although South American supplies continue to dominate global trade due to competitive pricing.

Soybean oil has remained one of the more volatile agricultural markets as traders continue evaluating renewable diesel demand and vegetable oil supplies worldwide. Price weakness in soybean oil has limited upside momentum across the entire soybean complex during recent weeks. Market participants will closely monitor July weather forecasts, USDA acreage revisions, and export sales for signs that demand can offset expectations for another large North American crop.

Wheat markets remained volatile throughout the week as harvest activity accelerated across the Southern Plains while traders evaluated production prospects across North America, Europe, and the Black Sea region. Winter wheat harvest continues progressing across Kansas, Oklahoma, and Texas with generally favorable yields being reported. While localized quality concerns exist due to rainfall in some areas, overall production expectations remain respectable. Kansas City wheat futures continue receiving intermittent support from concerns over high-protein wheat supplies, although ample global wheat inventories have limited sustained rallies.

Internationally, weather conditions across Russia and portions of Europe continue receiving close attention. Any production issues in major exporting countries could quickly improve U.S. export competitiveness later this summer. Demand remains relatively sluggish as global buyers continue sourcing wheat from multiple origins. Nevertheless, lower prices have begun attracting increased interest from importers, providing some underlying support. Producers should continue monitoring harvest quality reports and export demand as marketing opportunities develop through the summer months.

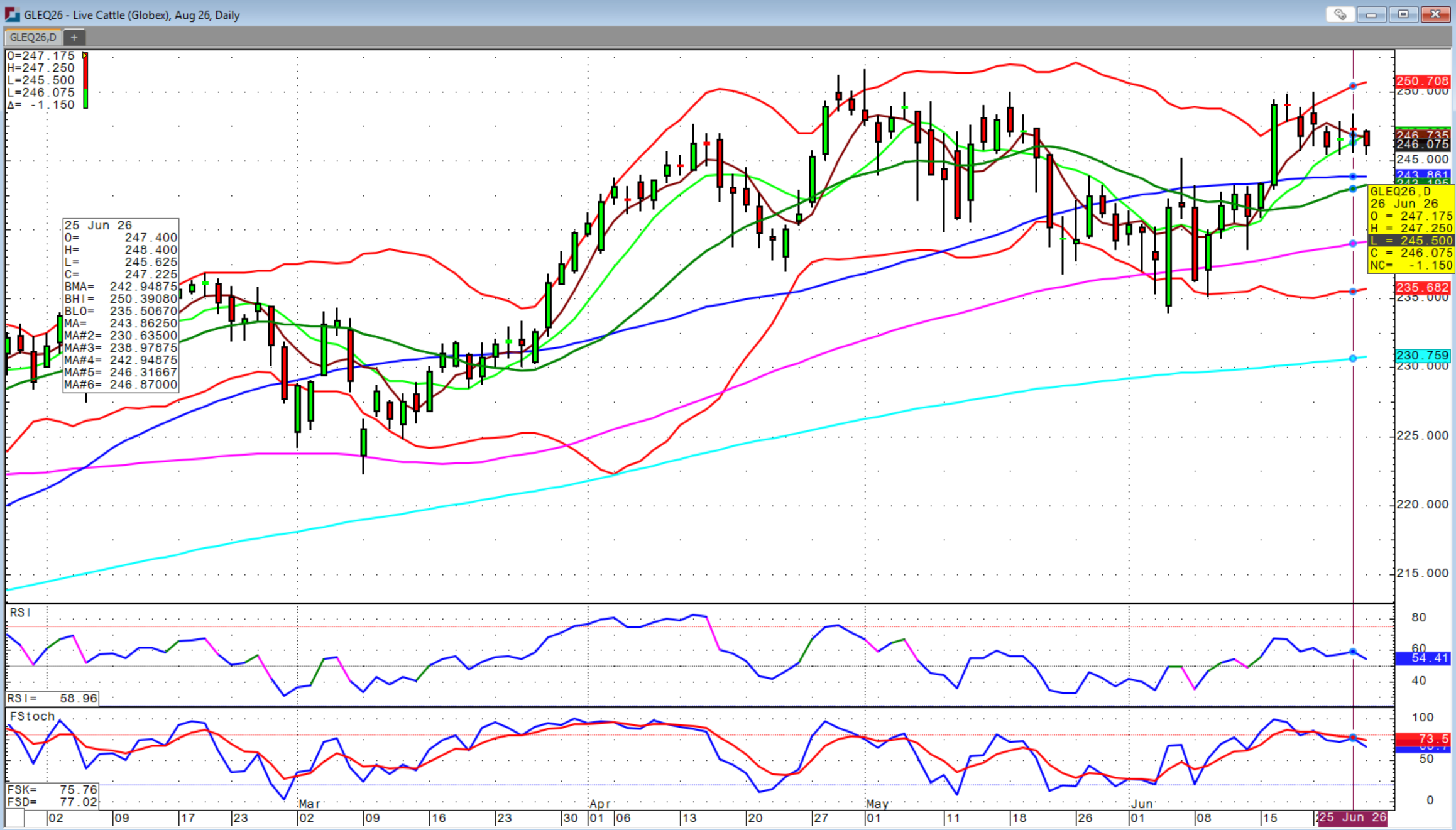

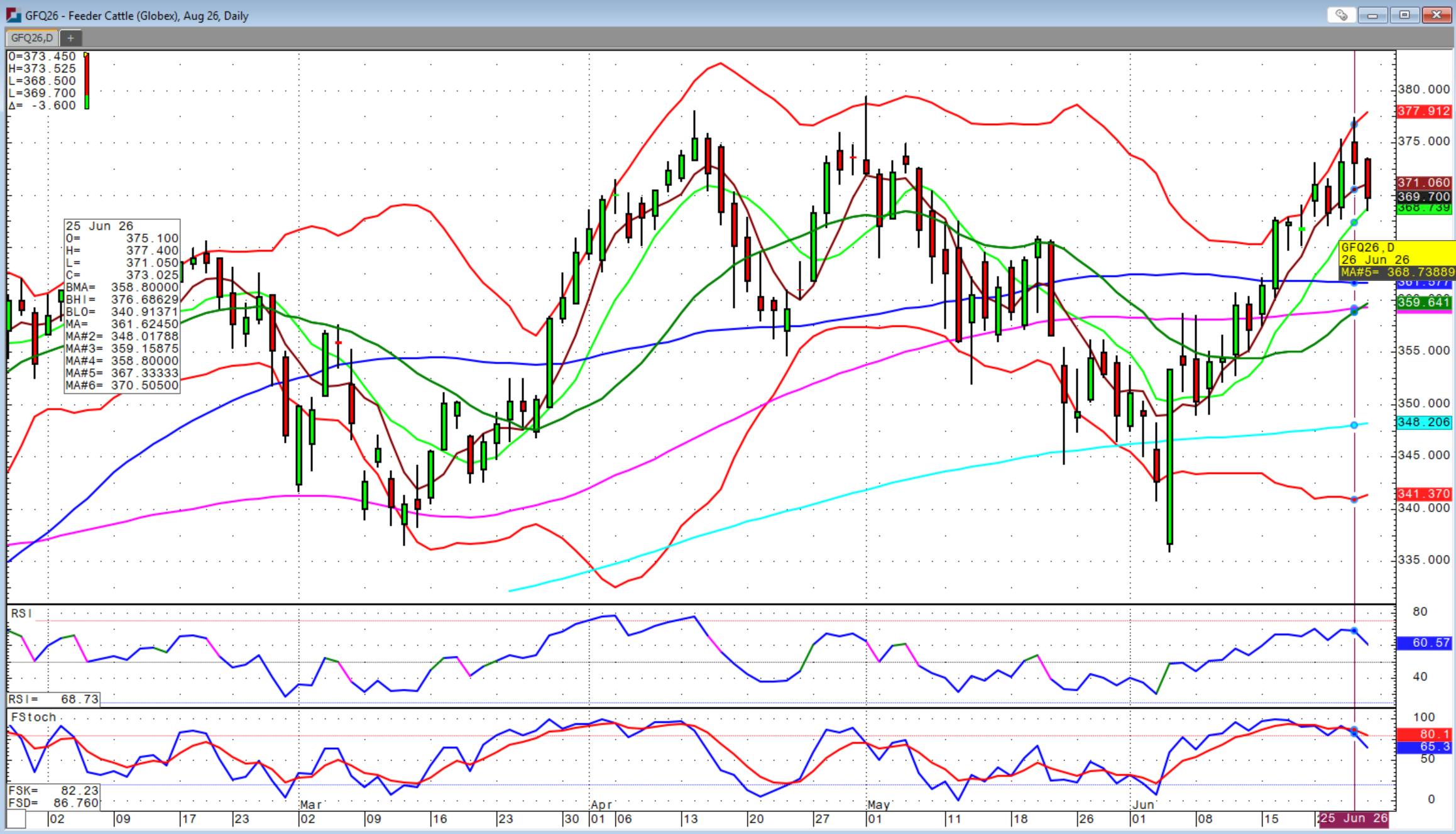

Live cattle and feeder cattle futures remained historically strong despite some profit-taking during the week. Fundamental supply conditions remain exceptionally supportive. U.S. cattle inventories continue near multi-decade lows following years of drought-induced herd liquidation across major cow-calf regions. Beef demand has remained remarkably resilient despite elevated retail prices. Consumers continue demonstrating willingness to purchase beef products, supporting packer margins and wholesale beef values.

Cash cattle markets have generally remained firm as packers compete for limited market-ready supplies. Feedlot placements continue reflecting reduced feeder cattle availability across much of the country. While elevated feed costs remain a concern for cattle feeders, lower corn prices have modestly improved feeding margins compared to earlier this year. Analysts generally expect cattle prices to remain historically strong through much of 2026 unless beef demand weakens significantly or herd expansion accelerates. However, rebuilding the national cow herd is expected to require several years, suggesting supplies may remain tight well beyond this year. Energy markets experienced one of the week's biggest reversals.

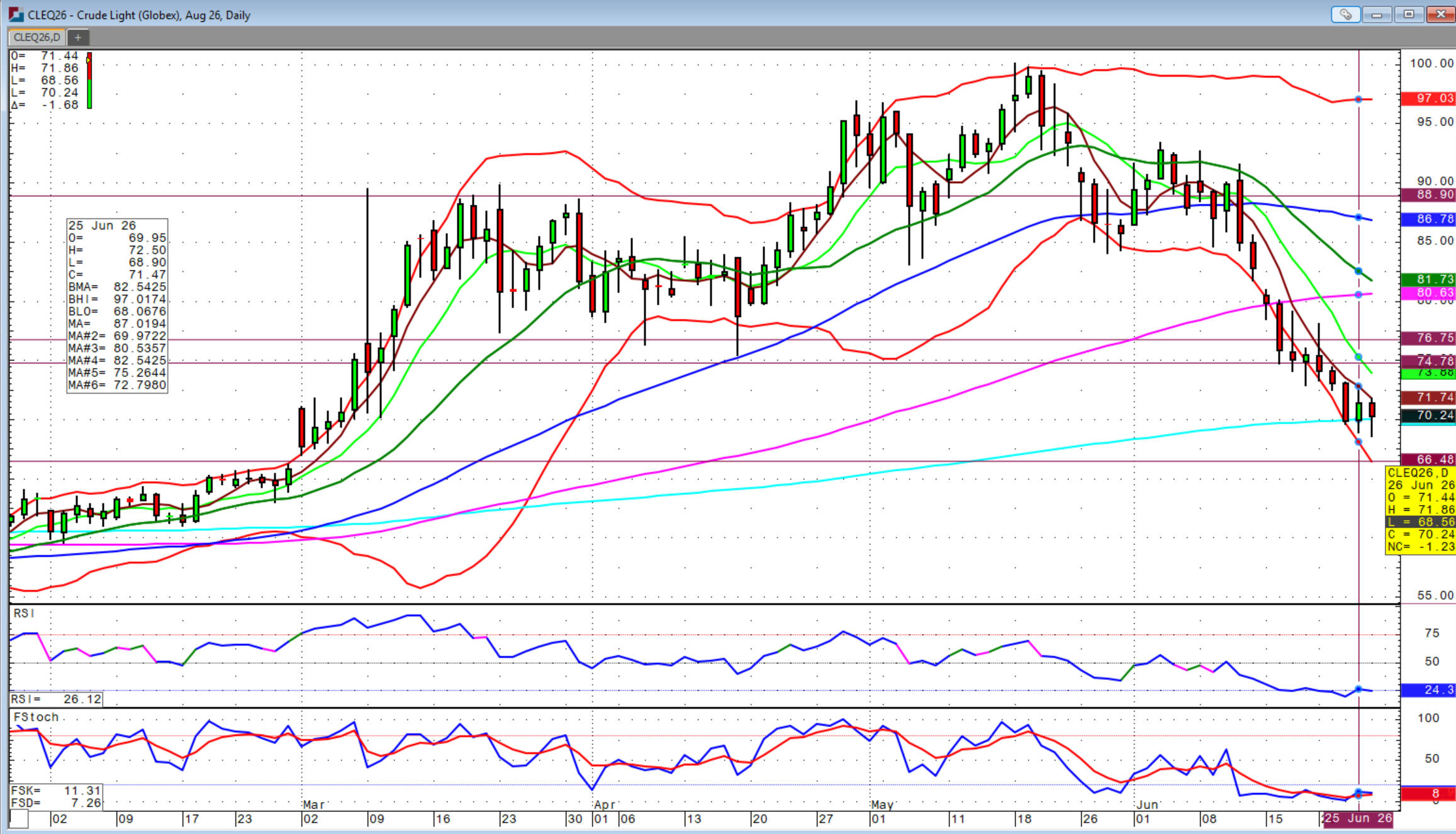

Crude oil prices declined sharply after geopolitical risk premiums eased following signs that shipping disruptions in the Middle East would remain limited. As concerns surrounding the Strait of Hormuz subsided and Saudi oil exports normalized, traders removed much of the premium that had been added earlier in the month. Brent crude fell toward the low-$70 per barrel range while WTI crude also declined significantly from recent highs. For agriculture, lower crude oil prices are welcome news. Diesel fuel remains one of the largest operating expenses for grain producers during spraying, irrigation, harvest preparation, and grain transportation. Any sustained decline in fuel costs would improve margins heading into harvest. Natural gas markets also remained relatively stable after significant volatility earlier this month. Domestic storage levels continue improving, reducing immediate concerns over summer supply availability, although weather-driven electricity demand remains an important variable heading into July.

Fertilizer markets continue watching natural gas closely since gas prices remain a primary cost component in nitrogen fertilizer production. Several major factors will likely determine commodity direction during the coming weeks.

First, weather remains the dominant influence for corn and soybean prices. Markets will increasingly focus on July forecasts as pollination approaches for corn and soybeans enter key vegetative growth stages. Second, export demand will remain critical. Continued competition from South America has pressured U.S. grain exports, but lower prices could eventually stimulate additional international buying. Third, livestock markets will continue watching beef demand and cash cattle trade. Tight supplies continue providing fundamental support, although futures markets remain vulnerable to periods of profit-taking after extended rallies. Finally, energy markets will remain sensitive to geopolitical developments.

While crude oil has retreated substantially this week, any renewed disruptions to global energy supplies could quickly reverse recent declines. Overall, agriculture enters the final week of June with generally favorable crop conditions, historically strong livestock fundamentals, and easing energy costs. As the calendar turns to July, weather will increasingly become the dominant market driver, making the next several weeks especially important for producers making marketing and risk management decisions. Grain producers should continue monitoring weather forecasts and export demand, while cattle operators remain positioned to benefit from one of the strongest supply environments seen in decades.

Sidwell Strategies is the one-stop shop to protect cattle with futures, puts, LRP or a combination of all, which is probably the best strategy overall. If you’re ready to trade commodity markets, give me a call at (580) 232-2272 or stop by my office to get your account set up and discuss risk management and marketing solutions to pursue your objectives. Self-trading accounts are also available. It is never too late to start and there is no operation too small to get a risk management and marketing plan in place.

Wishing everyone a successful trading week! Let us know if you'd like to join our daily market price and commentary text messages to stay informed!

Brady Sidwell is a Series 3 Licensed Commodity Futures Broker and Principal of Sidwell Strategies. You’re your Trading Account with Sidwell Strategies at https://portal.stonex.com/prefill/index/BradySidwellU52F112P. Contact us at (580) 232-2272 or at trade@sidwellstrategies.com.

Futures and Options trading involves the risk of loss and may not be suitable for all investors. Review full disclaimer at https://www.sidwellstrategies.com/fccp-disclaimer-21951.

/Renewable%20Energy%20by%20Yuri%20Hoya%20via%20Shutterstock.jpg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)