/Jen-Hsun%20Huan%20NVIDIA's%20Founder%2C%20President%20and%20CEO%20by%20jamesonwu1972%20via%20Shutterstock.jpg)

Relative to the value creation by Nvidia (NVDA) stock in the last five years, the last 52-weeks have been subdued. However, in all probability, the value creation story is far from over. The company has a dominant position in AI infrastructure and that’s likely to ensure continued growth in top line and cash flows.

Importantly, it’s the Nvidia platform moat that’s likely to ensure value creation. This point is underscored by a recent observation from Wedbush Securities. While Blackwell GPUs have been banned in China, it has seen price increases. Wedbush views this as a “persistence of this premium as a demand signal rather than a revenue one.”

Additionally, the willingness to pay twice the amount for Blackwell is indicative of how "wide the capability and software-stack gap” is as compared to peers. Nvidia therefore remains attractive with the data center market likely to remain a key growth driver.

About Nvidia Stock

Headquartered in Santa Clara, Nvidia is a giant in the technology sector and commands a market valuation of $4.8 trillion. Nvidia describes itself as a data center scale AI infrastructure company. The pioneer in accelerated computing has global presence and reported FY26 revenue of $216 billion, which was higher by 65% year-over-year (YOY).

Nvidia has two reportable segments: Compute & Networking and Graphics. For FY26, the compute & networking segment was the key revenue and operating income driver. The company’s business is a cash flow machine with FY26 operating cash flow of $102.7 billion.

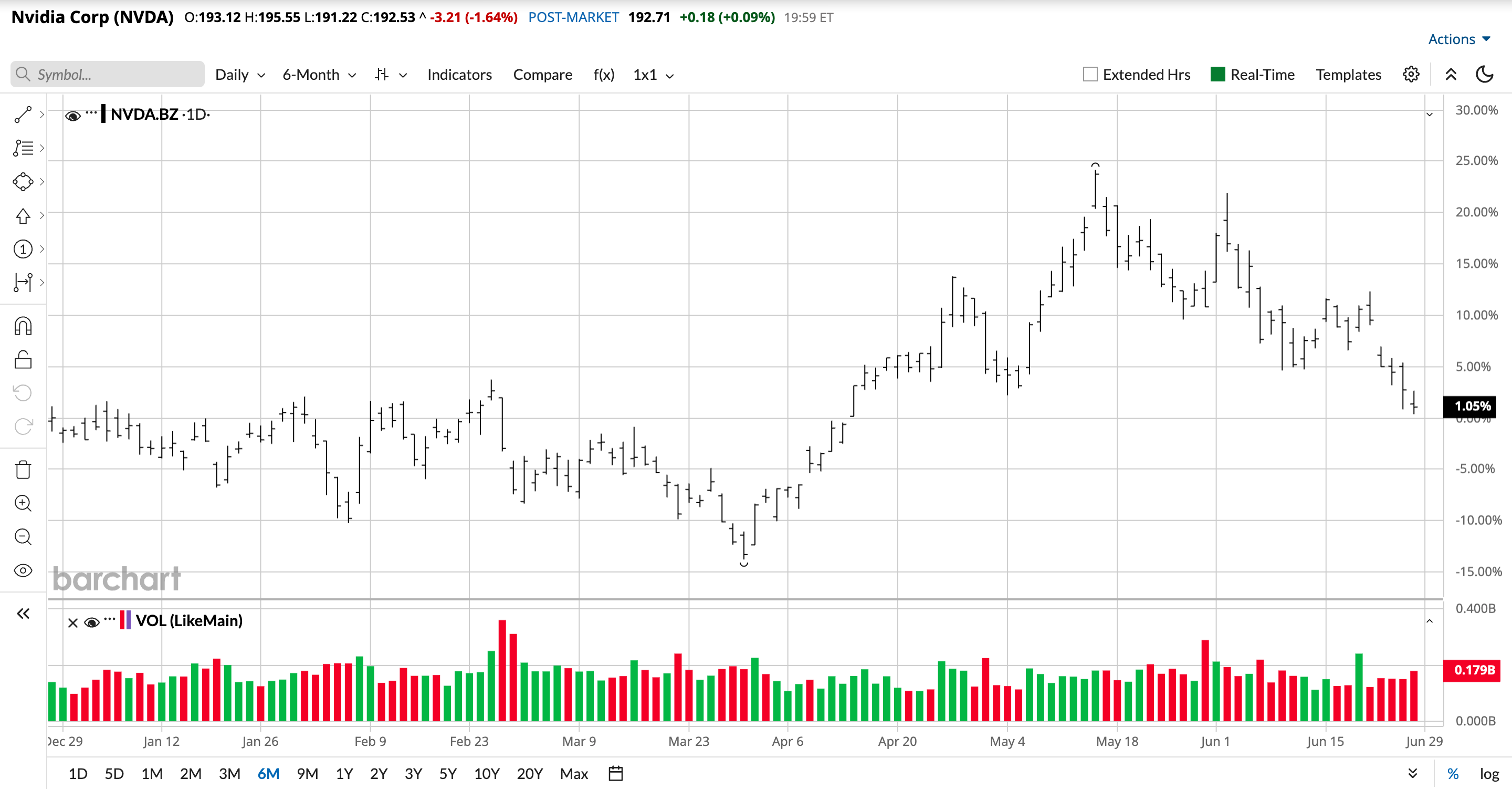

Continued investment in innovation provides Nvidia an edge and for FY26, the company’s research & development expense was $18.5 billion. While the company continues to deliver strong growth, NVDA stock has remained sideways in the last six months. This seems like an attractive accumulation opportunity with structural tailwinds likely to support sustained growth.

Large Addressable Market

According to Nvidia, hyperscale capital expenditure is likely to exceed $1 trillion in 2027. Additionally, with agentic AI proliferating all industries, the AI infrastructure spend is likely to swell to $3 trillion to $4 trillion annually by 2030.

Nvidia is already benefiting from the ramp-up of its Blackwell architecture. At the same time, the company expects to commence shipments of Vera Rubin in the second half of the year. According to Nvidia during the earnings call, Vera Rubin will be delivering “35x higher inference throughput and up to 10x greater AI factory revenue” when compared with Blackwell. So, Nvidia remains in the forefront of innovation that will support its market leadership position.

What Do Analysts Say About NVDA Stock?

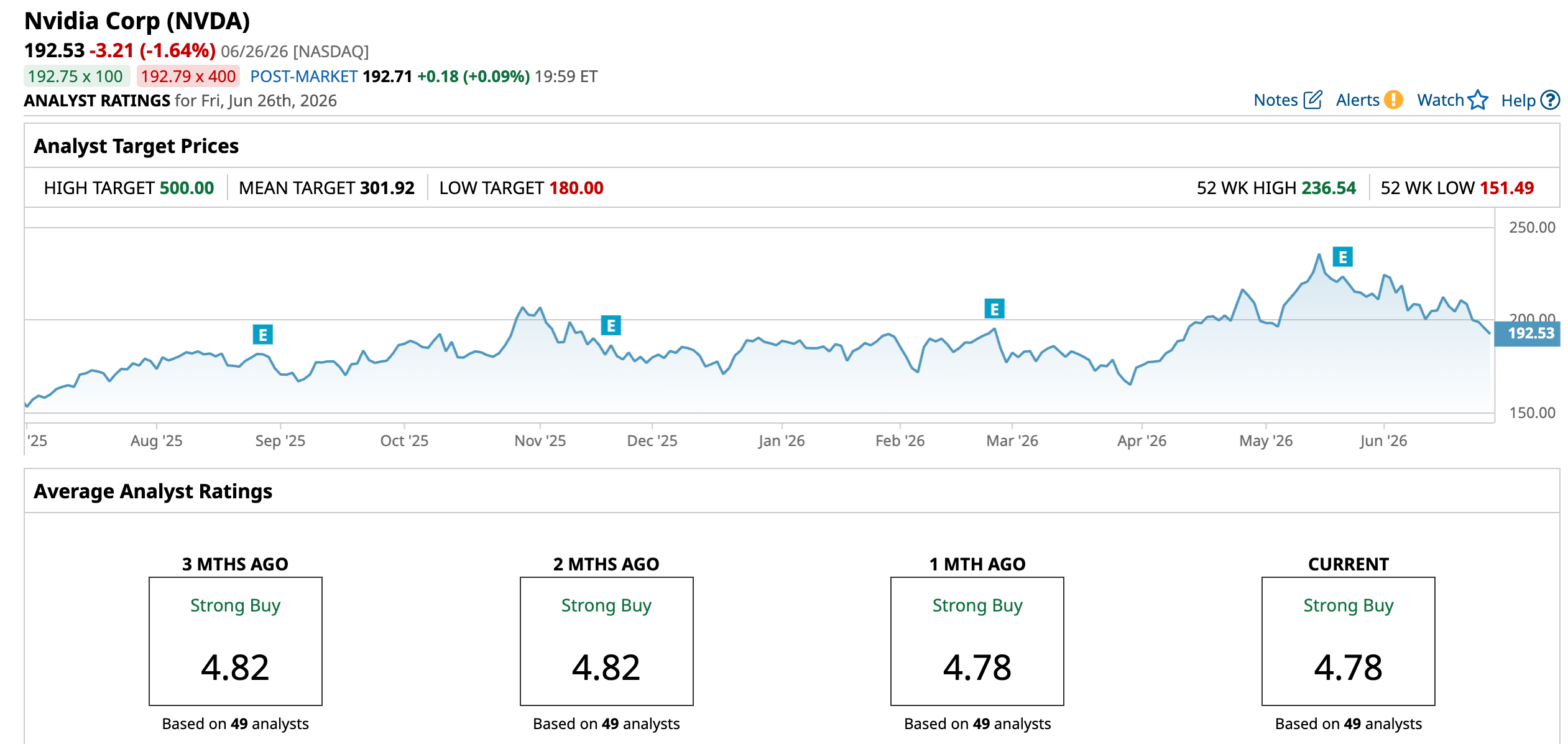

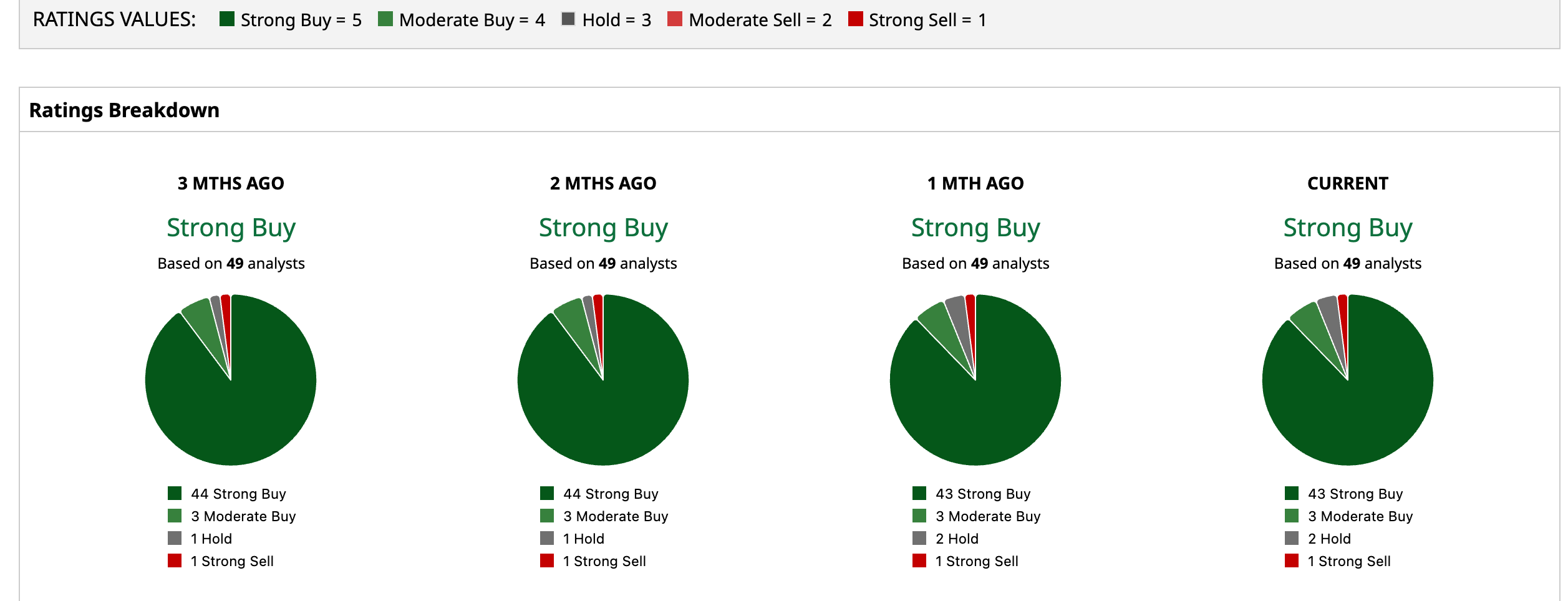

Based on 49 analysts with coverage, NVDA stock has a consensus “Strong Buy” rating. While 43 analysts have a “Strong Buy” rating for NVDA stock, three have a “Moderate Buy,” two have a “Hold,” and one analyst has a “Strong Sell” rating.

The mean price target of $301.92 represents a potential upside of 56.8% from current levels. Further, the most bullish price target of $500 suggests that NVDA could climb as much as 159.7% from here.

Concluding Views

From a valuation perspective, Nvidia stock trades at a forward price-to-earnings ratio of 22.52 times. With analysts expecting earnings growth for FY27 and FY28 at 90.15% and 34.29%, respectively, the price-earnings-to-growth ratio is 0.44 times. This is indicative of attractive valuations and the possibility of an uptrend from current levels.

Further, for Q1 FY27, Nvidia reported free cash flow of $48.6 billion. This would imply an annualized FCF potential of $195 billion. With robust growth cash flows will continue to swell and support value creation through dividends and aggressive share repurchase.

Finally, Nvidia acquired Kumo AI earlier this month for a consideration of $400 million. And, the company acquired AI chip start-up Groq in December 2025 for a consideration of $20 billion. With high financial flexibility, acquisitions will support the company’s innovation acceleration. These factors make NVDA stock attractive from a long-term perspective.

On the date of publication, Faisal Humayun Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Renewable%20Energy%20by%20Yuri%20Hoya%20via%20Shutterstock.jpg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)