If you look at the copper market chart over the past 10 years, it might seem like a perfectly balanced system. Market “bears” love to point to these figures. Global consumption has grown to about 28 million tons per year, but the industry has coped. Production has increased, and supply has met demand. No copper apocalypse has happened yet.

At first glance, everything is under control — but this is a very dangerous illusion. Those who assess copper's prospects relying only on the charts of the past decade are making a fundamental mistake. They see that the system has remained in balance, but they fail to understand how this balance has been maintained.

Personally, I have come to the conclusion that the copper market has survived due to powerful "compensators" in recent years. This refers to a phenomenal technological leap in mining, the depletion of the richest legacy deposits, and the aggressive pushed-to-the-limit collection of secondary raw materials. The problem is that all of these compensators are not infinite.

The era of easy solutions is over. To understand why the next 10 years of the copper market will not look like the previous decade, we need to put aside financial reports and recall the basic laws of physics.

A Physical Dead End: Why Copper Cannot Be Replaced

When we talk about oil, we know there are alternative sources of energy. Solar. Wind power. But when it comes to power electrical engineering, copper has become an unrivaled monopolist — and the reasons for this are embedded in the universe's architecture itself.

Why is there so much aluminum, silicon, and iron on Earth but so little copper? The answer lies in the stars. All chemical elements lighter than iron are synthesized in the cores of stars during their normal lifespans, so they are abundant in the Earth's crust. But copper is heavier than iron.

Elements of this type are born in the universe only during events like supernova explosions or neutron star mergers. Pure physics tells us that copper is inherently present in nature in orders of magnitude less than lighter metals. It is a non-renewable resource, and total geological reserves are fundamentally limited.

Ohm's Law and the Engineer's Trap

Copper has a uniquely low electrical resistivity. Only silver performs better, but it is too rare and insanely expensive for industrial use.

But why not replace copper with cheap aluminum, which is plentiful? This is where the main technological trap lies. Aluminum is great for overhead power lines where wire thickness is not critical, but aluminum's resistance is much higher than copper's resistance. If you try to wind an electric motor coil from aluminum wire instead of copper, you will have to make the motor much heavier to get the same power.

For the modern world — where the compactness and efficiency of electric vehicles (EVs), drones, and industrial robots are crucial — this is an engineering death sentence. You cannot put a refrigerator-sized motor in a modern EV. In closed systems where electricity is converted into kinetic energy, there is simply no substitute for copper.

Copper Devourers: The Real Reason for Exponential Demand

When the average person hears about copper demand, they probably imagine wires in the walls of new houses or cables for data centers. Yes, those use cases are important. But a cable in a wall is static demand — it is laid once and serves for decades. The real monster beginning to devour global copper reserves right now is the electric motor.

The world is in a stage of transitioning to electric propulsion, and this process is only gaining momentum. The heart of any electric motor is a tightly wound copper stator and rotor coil. The more motors, the faster copper reserves are depleted. Take EVs. The average electric car requires three to four times more pure copper than a traditional internal combustion engine (ICE) vehicle, and the lion's share of this metal goes not into the wiring but directly into the massive power unit.

Add to this total automation. In modern factories, every new industrial robot, conveyor, servo drive, powerful pump, or climate-control system means dozens and hundreds of new electric motors.

Copper demand from electric drive manufacturers will grow not linearly, but exponentially. Humanity will produce hundreds of millions of new electric motors in the coming decade, and each of them will require a metal born in supernovas. A metal that engineers physically cannot replace with cheap aluminum.

Tactical Shock: AI Infrastructure and Liquid Cooling

While electric motors are a fundamental demand driver for the next decade, a massive tactical shock is also unfolding in the market right now: infrastructure for artificial intelligence (AI).

In 2024, at the peak of the first wave of the AI hype, investors were buying shares of chipmakers. For the copper market, this didn't matter much. Microprocessors and printed circuit boards themselves consume a negligibly small amount of metal, compared to a scale of millions of tons. But now the virtual hype has turned into a giant physical construction site.

Modern server racks for AI consume a massive 100 to 120 kilowatts of energy, and ordinary cables simply cannot handle such a load. The industry is urgently shifting to massive copper busbars. These are thick, solid strips of pure copper for power distribution within racks.

Moreover, with such heat dissipation, traditional fans can no longer cope. Data centers are being forced to switch to direct liquid cooling systems, which means kilometers of copper tubing, copper cold plates on processors, and giant heat exchangers. In these systems, copper is necessary due to its phenomenal thermal conductivity.

Yes, in absolute terms, data centers do not consume millions of tons like the auto industry. But in the commodity market, the price balance is determined by marginal demand. In an environment where the copper market is already stretched, the sudden emergence of an industry that urgently needs additional tens of thousands —and even hundreds of thousands — of tons of copper becomes that very drop. The drop that overflows the cup.

Production Crisis: The Age of ‘Compensators’ Is Over

So, copper demand is guaranteed to go up due to mass electrification and millions of new electric motors. But why won't the mining industry be able to respond to this challenge the same way that it has over the last 10 years?

The answer lies in the exhaustion of the three main "compensators" that have so far masked the looming deficit.

Over the past two decades, the mining industry has made a colossal leap in labor productivity. The introduction of giant 400-ton autonomous haul trucks, automated drilling rigs, and control systems has allowed companies to sharply reduce production costs.

This technological boom made it profitable to extract copper from extremely low-grade ore. If 50 years ago, a copper grade of 1% to 2% was considered the norm, today industry giants are forced to process ore with a grade of only 0.4% to 0.5%.

But this technical progress is not infinite. The effect of automation will weaken because raising efficiency, having a high base, will become more and more difficult. Modern dump trucks are already highly efficient. But as the quality of the remaining ore in the ground continues to decline, mining the same ton of copper will now require processing more and more waste rock. That means higher costs for energy, water, and logistics — costs that can no longer be offset by smart electronics.

The Secondary Processing Wall and the Scrap Illusion

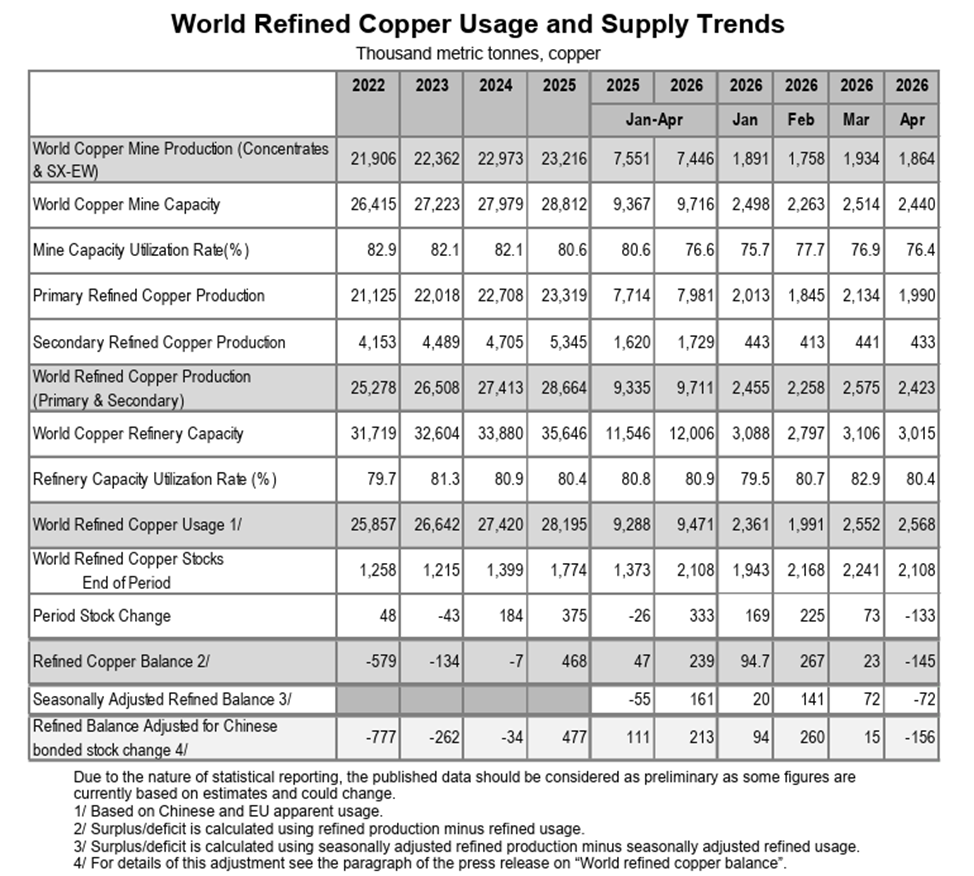

“Bears” often argue their position by claiming that the deficit will be covered by processing secondary raw materials. Indeed, in recent years, as copper prices moderately rose, the world began to collect and recycle scrap much more meticulously. Dry statistics, at first glance, give them reason for optimism. From 2024 to 2025, global production of secondary refined copper made an anomalous jump from 4.705 million tons to 5.345 million tons.

But a fundamental mistake lies here. This is a banal misunderstanding of the difference between primary and secondary raw materials.

Primary extraction of ore from the ground is a real, systemic influx of new metal into the economy, while secondary scrap is merely an exhaustible reservoir from past years. Rising prices forced the market to aggressively "vacuum up" scrap, but this process has a strict economic limit. Secondary raw material collection has its own cost curve. You can quickly and cheaply pump easily accessible reserves out of the market, but as soon as this superficial reservoir empties, the cost of finding, dismantling, and transporting each subsequent ton of old copper skyrockets.

If you want to see what this trap looks like in real time, just look at statistics from the International Copper Study Group for early 2026. Fundamental global mine production for January to April 2026 dropped to 7.446 million tons compared to 7.551 million tons for the same period in 2025. This means that physically less metal was extracted from the ground.

So, where did the temporary surplus at the beginning of the year come from? Smelters simply "threw into the furnace" the accumulated scrap reserves. Secondary production over the same period grew from 1.62 million tons to 1.729 million tons.

But this surge in secondary processing cannot be extrapolated into the future. You cannot systematically load capacity with scrap because it depletes quickly. Already in April, the overall refined copper balance plunged into a deficit of -145,000 tons.

A Geological and Time Dead End

New large and easily accessible copper deposits on the planet simply aren't being discovered. All the "easy" copper has already been mined.

To launch a new mega-mine from scratch in the current environment, it takes 10 to 15 years — from initial geological exploration and obtaining environmental permits to shipping the first commercial ton. For many years, the capital expenditures of mining companies were constrained due to low commodity prices.

Because of this underinvestment in the past, the physical supply of copper today is locked in time. The industry will simply not have time to ramp up capacity by the time demand makes its next leap.

Copper Is the Main Metal of the Future

Without copper, the entire "green" and technological revolution will simply halt on paper. Copper is not just an industrial raw material. It is the physical foundation, the blood, and the muscles of the future.

What we have seen on the charts recently — breaking local highs and the start of an uptrend — is not temporary speculative hype. It is the very beginning of a tectonic shift. The broader market is only just beginning to realize the scale of the impending problem.

In the next 10 years, the copper market will inevitably enter a phase of structural deficit. Since supply is constrained by physical, geological, and technological boundaries, and secondary reserves are already being fully utilized, the only way to balance the market in the future is "demand destruction." And the only mechanism for demand destruction in a market economy is a price increase.

Copper prices will have to reach fundamentally new historical levels — levels so high that some consumers will simply refuse to use copper where it is still physically possible. This very action will be able to balance supply and demand.

For the long-term investor, this forms one of the most reliable and asymmetric opportunities in the market. Investing in copper, and in the shares of fundamentally strong mining companies with real reserves in the ground, is not a bet on market sentiment. It is a bet on the harsh, immutable laws of physics which simply cannot be bypassed.

On the date of publication, Mikhail Fedorov did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/An%20Intel%20sign%20out%20front%20of%20a%20corporate%20office%20by%20wolterke%20via%20Adobe%20Stock.jpeg)

/Alibaba%20by%20testing%20via%20Shutterstock.jpg)

/Alphabet%20(Google)%20Image%20by%20Markus%20Mainka%20via%20Shutterstock.jpg)