Manchester United (MANU) made big news earlier this week when it announced it had secured most of the land needed to build a new 100,000-seat stadium.

The 25-acre property is close to Old Trafford, the iconic British soccer team’s current stadium. When built, the stadium would be the second-largest in Europe, behind only Barcelona’s Camp Nou at 105,000.

Already one of the most valuable sports teams in the world, the club’s money-making possibilities increase exponentially with a 100,000-seat stadium. Further, it is part of a larger 370-acre regeneration project taking place in Trafford, a borough of the city of Manchester. When the entire mixed-use development is completed, it’s expected to inject 7 billion British pounds ($9.25 billion) into the UK economy annually.

Because of the exciting news, combined with the World Cup currently underway in North America, Manchester United’s options volume surged on Thursday, up 8.3 times the 30-day average.

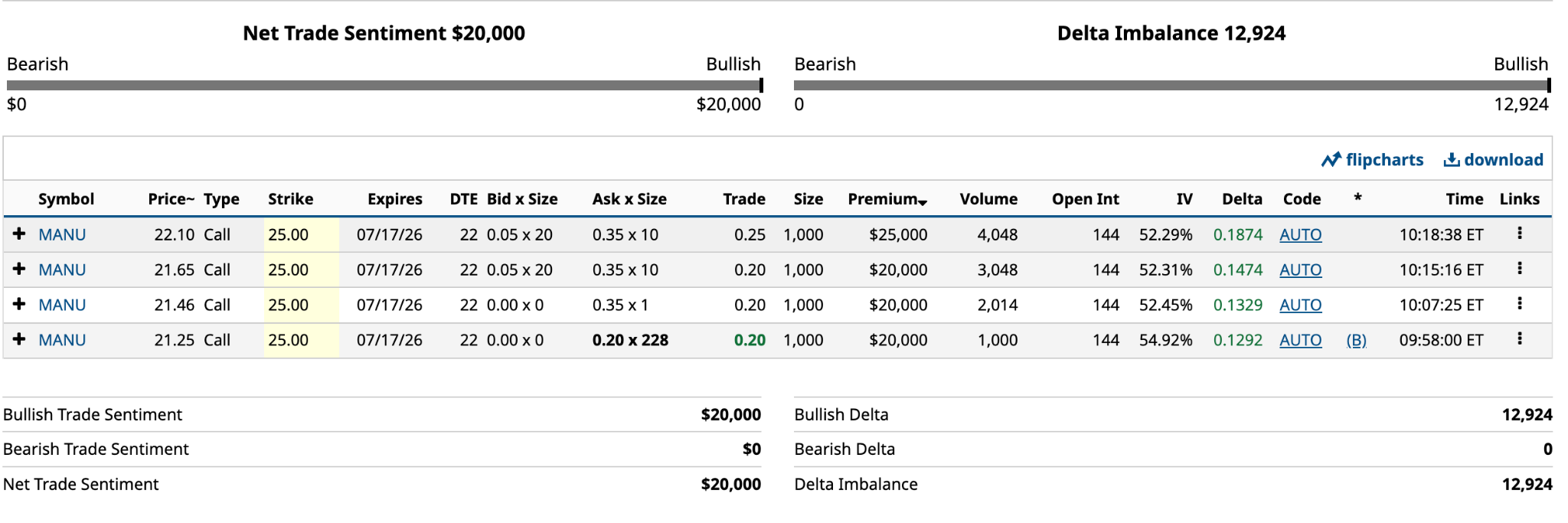

One of the top 100 unusually active options in yesterday’s trading was the July 17 $25 call, which had a Vol/OI (volume-to-open-interest) ratio of 28.40.

The call’s volume of 4,090 stands out because 98% of it was for four, 1,000-call trades. While the news is very positive for the future of Manchester United, you might want to think twice before making a similar bet.

Have an excellent weekend.

The MANU Call Option in Question

MANU’s total options volume yesterday was the third-highest in the past three months and the 10th-highest in the past year. There’s no question that Monday’s announcement sparked increased interest in the stock’s options. However, the volume surge didn’t happen until Thursday, so it’s not entirely clear why there was such a delay. I’ll get into that shortly.

As I said in the introduction, the July 17 $25 call accounted for almost all yesterday’s options volume, and four trades of 1,000 contracts did most of the work.

As you can see from above, the four trades took place between 9;58 a.m. ET and 10:18 a.m. ET. All four trade prices skewed toward the ask, suggesting a bullish lean. Overall, the trader/investor paid $85,000 for notional control of 400,000 MANU shares for just 0.98% of the share price. That’s a good use of leverage.

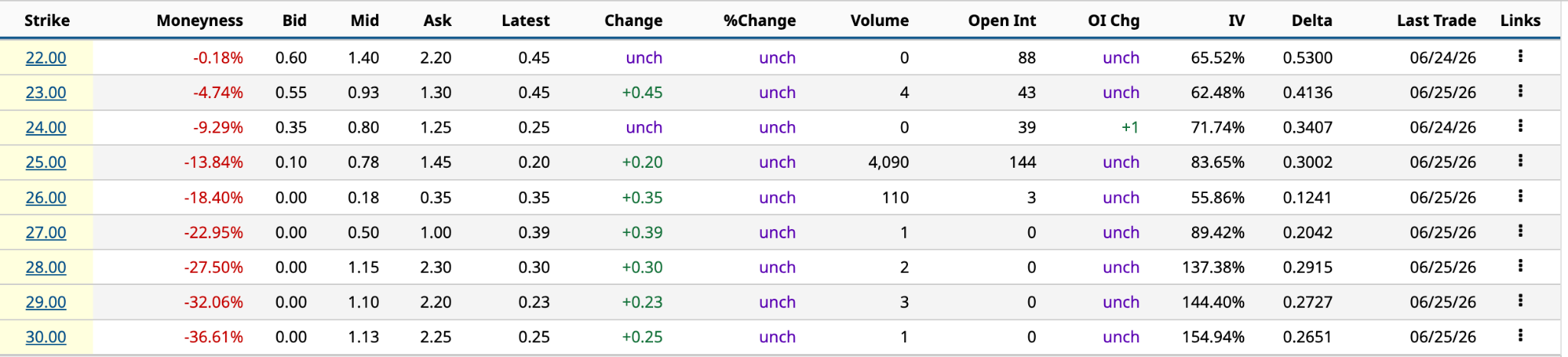

Here’s how the July 17 $25 call looked at the end of Thursday’s trading.

The probability of profit on the $25 call at the end of the day was about 25.76%. The closing share price was slightly lower than what it was for the final 1,000-call trade at 10:18 a.m. ET on Thursday. The bid/ask spread at the close was $1.35 ($1.45 ask and $0.10 bid). That’s not uncommon for low-volume options.

The trader/investor of the 4,000 contracts in early trading paid an average of $21.25 per contract, or $0.2125. That’s about 58% less than the day’s highest trade price of $0.50. That’s a big advantage.

Here are the pros and cons of buying $25 long calls, or calls at any strike price, for the underlying MANU stock.

The Pros of Long MANU Calls

Now that the stadium deal is out in the open, investors can start speculating about what it means for the team's future valuation and its revenue generation.

In May 2025, Forbes valued the team at $6.6 billion based on $834 million in revenue from the 2023-2024 season — it finished 8th in the Premier League that year — so it's got brand stickiness, as they say in marketing.

I’m not entirely sure where Forbes got its revenue number of 620 million British pounds ($834 million). The June 2024 year-end revenue, according to S&P Global Capital Markets, was 661.8 million British pounds ($874.0 billion), about the same as in 2025, and it should be slightly higher when it reports Q4 2026 in September.

The current market cap is $3.65 billion based on 172.4 million shares outstanding. The enterprise value is $4.57 billion based on the $3.65 billion market cap plus $998.2 million in debt, less $80.5 million in cash.

Forbes is effectively saying that Manchester United is undervalued by 44% in terms of enterprise value and by 81% if based on market cap. I doubt it’s the latter.

If 44% undervalued, and nothing were to change about debt and cash, the fair value of MANU stock would be $31.94 a share, 23.1% higher than the median target price of 19.65 British pounds ($25.94). The highest analyst estimate is 22.88 British pounds ($30.20), so it is in the ballpark.

There is a possibility that more news about the stadium will attract more analyst attention to the stock and possibly, higher target prices, which could lead to higher share prices.

At the end of the day, a 1% outlay is less than the cost of a trip to the movies. If you’ve got the money to burn, it’s not the worst bet in the world.

The Cons of Long MANU Calls

If you look at the OTM (out-of-the-money) July 17 call prices at the end of yesterday’s trading, you’ll notice that the $25 strike had a mid-price of $0.78, slightly higher than the $0.89 average for the nine strike prices.

With a 21-day DTE (days to expiration), the expected move is just 5.23%, well below the 14.8% needed to break even at $25.2125. Interestingly, if you compare the $25 and $26 strike prices, the probability of profit is much higher for the $25 strike price despite the only a $1 difference. It could be because the IV (implied volatility) for the $25 strike is considerably higher, suggesting greater price movement between now and July 17. It could also mean the IV numbers for the $26 call are meaningless due to the low volume and open interest.

The ideal DTE would be about six weeks, or double the July 17 expiration, providing slower time decay and a greater chance of an unexpected move. But that’s not the subject here. We’re debating the wisdom of buying July 17 $25 longs, 13.84% OTM.

For such a move to come to fruition, there has to be a catalyst before July 17. The stadium, clearly, is not it. Even with a massive push to open, it won’t happen before the second half of 2034 or into 2035. By 2030, the club can use the new stadium to positively affect its revenue streams, arguing to major partners and advertisers that higher fees today will grant them greater access at the new stadium when it opens. But that’s merely speculation.

It also isn’t earnings. MANU doesn’t report its quarterly earnings until Sept. 16. One possibility is the report earlier in June that members of the Glazer family, who’ve controlled the team for more than 20 years, are considering selling part or all of their holdings in the club.

While UK billionaire Jim Ratcliffe, through his Ineos Group business, has the largest equity position at slightly less than 29%, the Glazers control Manchester United through the Class B voting shares (68%), which carry 10 votes per share, while the Class A shares carry one vote per share.

Any decision by the family won't come in the next three weeks, so it’s not really a factor either.

The Bottom Line on MANU Stock

Owning a professional sports team is a lot like being a farmer. You don’t get rich while operating the team or farm, but if you’re lucky, you do when you sell.

Let’s face it, there are many more profitable businesses to own than Manchester United, whose 27.8% EBITDA (earnings before interest, taxes, depreciation and amortization) margin might seem okay, until you compare it to Nvidia’s (NVDA) at 61.7%. There’s no question which one you pick if you can only own one.

The stadium is expected to cost 2 billion British pounds ($2.64 billion) or more and be ready in time to potentially host games for FIFA’s 2035 Women’s World Cup. Plenty will happen over the next nine years; some of it good, some of it bad. Regardless, it’s highly likely that Manchester United will be worth far more in 2035 than it is today.

Manchester United went public in August 2012 at $14 a share. Its 200-day moving average has ranged between $14.50 and $2o. MANU is not a stock where you can get rich quickly. You must be patient. If you buy MANU stock at $22 and hold for a decade, you should do well.

However, buying July $25 calls is a crapshoot. There is no near-term catalyst I can see to recommend what the trader/investor did yesterday with four 1000-call buys. I would look elsewhere for a quick profit.

On the date of publication, Will Ashworth did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20close-up%20of%20the%20Broadcom%20logo%20on%20a%20smartphone%20by%20Timon%20via%20Adobe%20Stock.jpeg)

/An%20Intel%20sign%20out%20front%20of%20a%20corporate%20office%20by%20wolterke%20via%20Adobe%20Stock.jpeg)