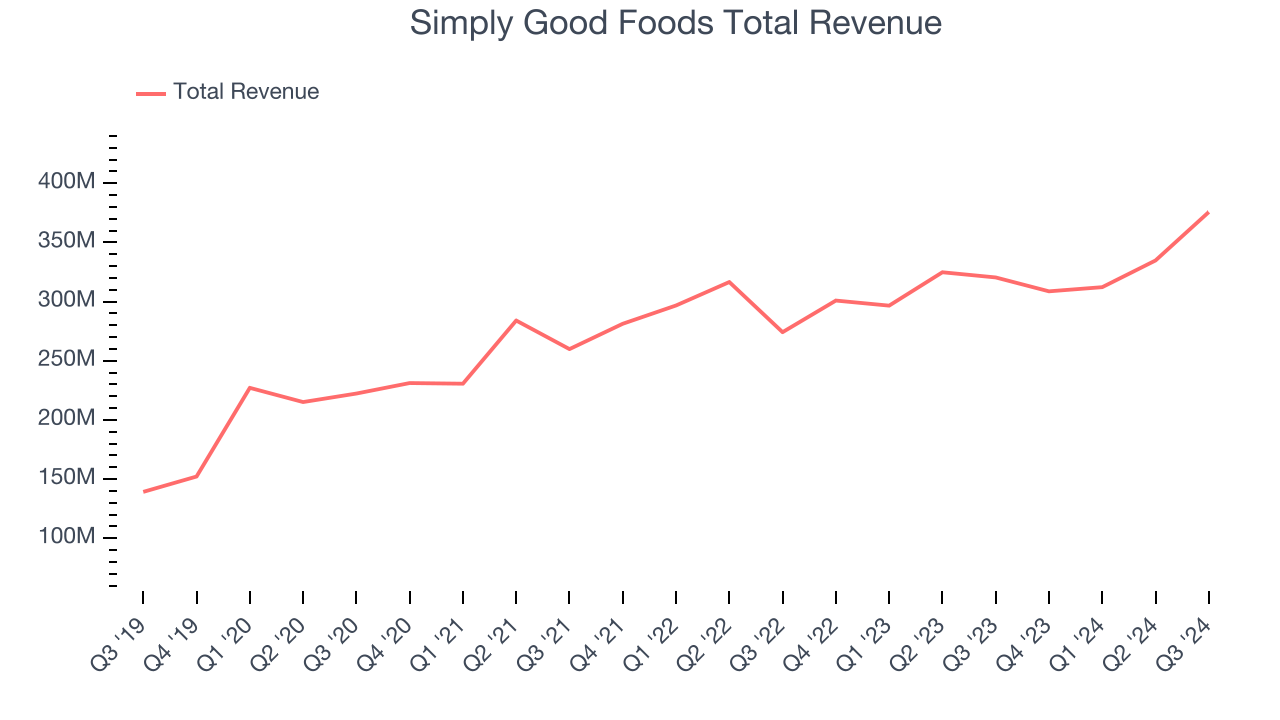

Packaged food company Simply Good Foods (NASDAQ:SMPL) met Wall Street’s revenue expectations in Q3 CY2024, with sales up 17.2% year on year to $375.7 million. Its non-GAAP profit of $0.50 per share wasalso in line with analysts’ consensus estimates.

Is now the time to buy Simply Good Foods? Find out by accessing our full research report, it’s free.

Simply Good Foods (SMPL) Q3 CY2024 Highlights:

- Revenue: $375.7 million vs analyst estimates of $373.3 million (in line)

- Adjusted EPS: $0.50 vs analyst expectations of $0.50 (in line)

- EBITDA: $77.45 million vs analyst estimates of $74.96 million (3.3% beat)

- Gross Margin (GAAP): 38.8%, up from 37.6% in the same quarter last year

- Operating Margin: 12.7%, down from 17.4% in the same quarter last year

- EBITDA Margin: 20.6%, in line with the same quarter last year

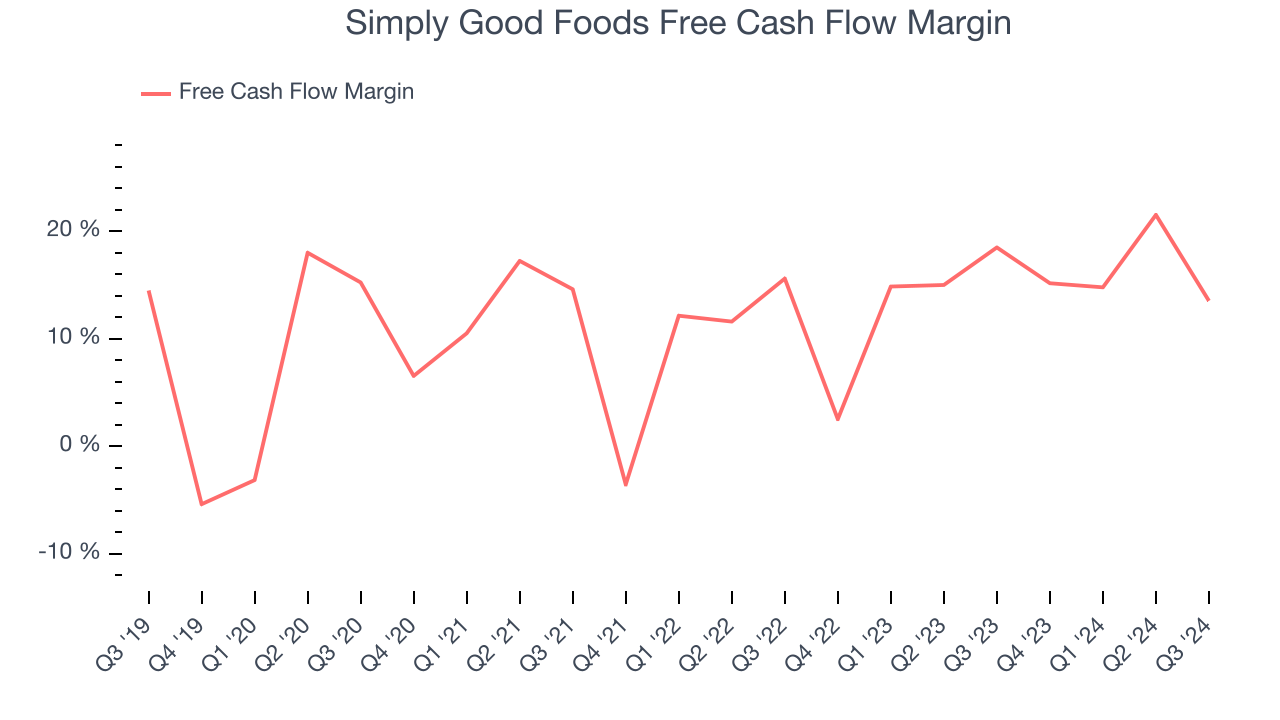

- Free Cash Flow Margin: 13.5%, down from 18.5% in the same quarter last year

- Market Capitalization: $3.23 billion

"In fiscal 2024, the Simply Good Foods team delivered on our strategic initiatives driving solid retail takeaway gains that resulted in full year volume driven legacy(5) net sales growth of about 5% and an increase of Adjusted EBITDA of nearly 10%," said Geoff Tanner, President and Chief Executive Officer.

Company Overview

Best known for its Atkins brand that was inspired by the popular diet of the same name, Simply Good Foods (NASDAQ:SMPL) is a packaged food company whose offerings help customers achieve their healthy eating or weight loss goals.

Shelf-Stable Food

As America industrialized and moved away from an agricultural economy, people faced more demands on their time. Packaged foods emerged as a solution offering convenience to the evolving American family, whether it be canned goods or snacks. Today, Americans seek brands that are high in quality, reliable, and reasonably priced. Furthermore, there's a growing emphasis on health-conscious and sustainable food options. Packaged food stocks are considered resilient investments. People always need to eat, so these companies can enjoy consistent demand as long as they stay on top of changing consumer preferences. The industry spans from multinational corporations to smaller specialized firms and is subject to food safety and labeling regulations.

Sales Growth

A company’s long-term performance can indicate its business quality. Any business can put up a good quarter or two, but many enduring ones grow for years.

Simply Good Foods is a small consumer staples company, which sometimes brings disadvantages compared to larger competitors benefitting from economies of scale.

As you can see below, Simply Good Foods grew its sales at a decent 9.8% compounded annual growth rate over the last three years as consumers bought more of its products.

This quarter, Simply Good Foods’s year-on-year revenue growth was 17.2%, and its $375.7 million of revenue was in line with Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 11.1% over the next 12 months, an acceleration versus the last three years. This projection is noteworthy and shows the market believes its newer products will spur faster growth.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) semiconductor stock benefitting from the rise of AI. Click here to access our free report on our favorite semiconductor growth story.

Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Simply Good Foods has shown terrific cash profitability, driven by its lucrative business model that enables it to reinvest, return capital to investors, and stay ahead of the competition. The company’s free cash flow margin was among the best in the consumer staples sector, averaging 14.6% over the last two years.

Taking a step back, we can see that Simply Good Foods’s margin expanded by 3.4 percentage points during that time. This shows the company is heading in the right direction, and because its free cash flow profitability rose more than its operating profitability, continued increases could suggest it’s becoming a less capital-intensive business.

Simply Good Foods’s free cash flow clocked in at $50.79 million in Q3, equivalent to a 13.5% margin. The company’s cash profitability regressed as it was 5 percentage points lower than in the same quarter last year. This warrants extra attention because consumer staples companies typically produce more consistent and defensive performance.

Key Takeaways from Simply Good Foods’s Q3 Results

It was good to see Simply Good Foods beat analysts’ EBITDA expectations this quarter. We were also happy its gross margin narrowly outperformed Wall Street’s estimates. Overall, this quarter had some key positives. The stock traded up 2.4% to $33 immediately following the results.

So do we think Simply Good Foods is an attractive buy at the current price?The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.

/Adobe%20Inc%20logo%20on%20computer-by%20DANIEL%20CONSTANTE%20via%20Shutterstock.jpg)

/A%20Palantir%20office%20building%20in%20Tokyo_%20Image%20by%20Hiroshi-Mori-Stock%20via%20Shutterstock_.jpg)

/Micron%20Technology%20Inc_billboard-by%20Poetra_RH%20via%20Shutterstock.jpg)