IT project management software company, Atlassian (NASDAQ:TEAM) reported results in line with analysts' expectations in Q2 CY2024, with revenue up 20.5% year on year to $1.13 billion. On the other hand, the company expects next quarter's revenue to be around $1.15 billion, slightly below analysts' estimates. It made a non-GAAP profit of $0.66 per share, improving from its profit of $0.57 per share in the same quarter last year.

Is now the time to buy Atlassian? Find out by accessing our full research report, it's free.

Atlassian (TEAM) Q2 CY2024 Highlights:

- Revenue: $1.13 billion vs analyst estimates of $1.13 billion (small beat)

- Adjusted Operating Income: $222 million vs analyst estimates of $213.3 million (4.1% beat)

- EPS (non-GAAP): $0.66 vs analyst estimates of $0.60 (9.3% beat)

- Revenue Guidance for Q3 CY2024 is $1.15 billion at the midpoint, below analyst estimates of $1.16 billion

- Management's revenue guidance for the upcoming financial year 2025 is $5.06 billion at the midpoint, missing analyst estimates by 1.8% and implying 16% growth (vs 23.2% in FY2024)

- Gross Margin (GAAP): 80.8%, down from 82.9% in the same quarter last year

- Free Cash Flow of $413.2 million, down 25.5% from the previous quarter

- Billings: $1.29 billion at quarter end, up 18.8% year on year

- Market Capitalization: $45.96 billion

“We announced transformative innovations for our customers like Rovo, the latest human-AI technology reshaping the way we work. We achieved significant milestones like FedRAMP’s “In Process” status, a huge step towards supporting the U.S. public sector in the cloud, and we wound down support for Server,” said Mike Cannon-Brookes, Atlassian’s co-founder and co-CEO.

Founded by Australian co-CEOs Mike Cannon-Brookes and Scott Farquhar in 2002, Atlassian (NASDAQ:TEAM) provides software as a service that makes it easier for large teams of software developers to manage projects, especially in software development.

Project Management Software

The future of work requires teams to collaborate across departments and remote offices. Project management software is both driving this change and benefiting from it. While the trend of collaborative work management has been strong for a while, the Covid pandemic has definitively accelerated the demand for tools that allow work to be done remotely.

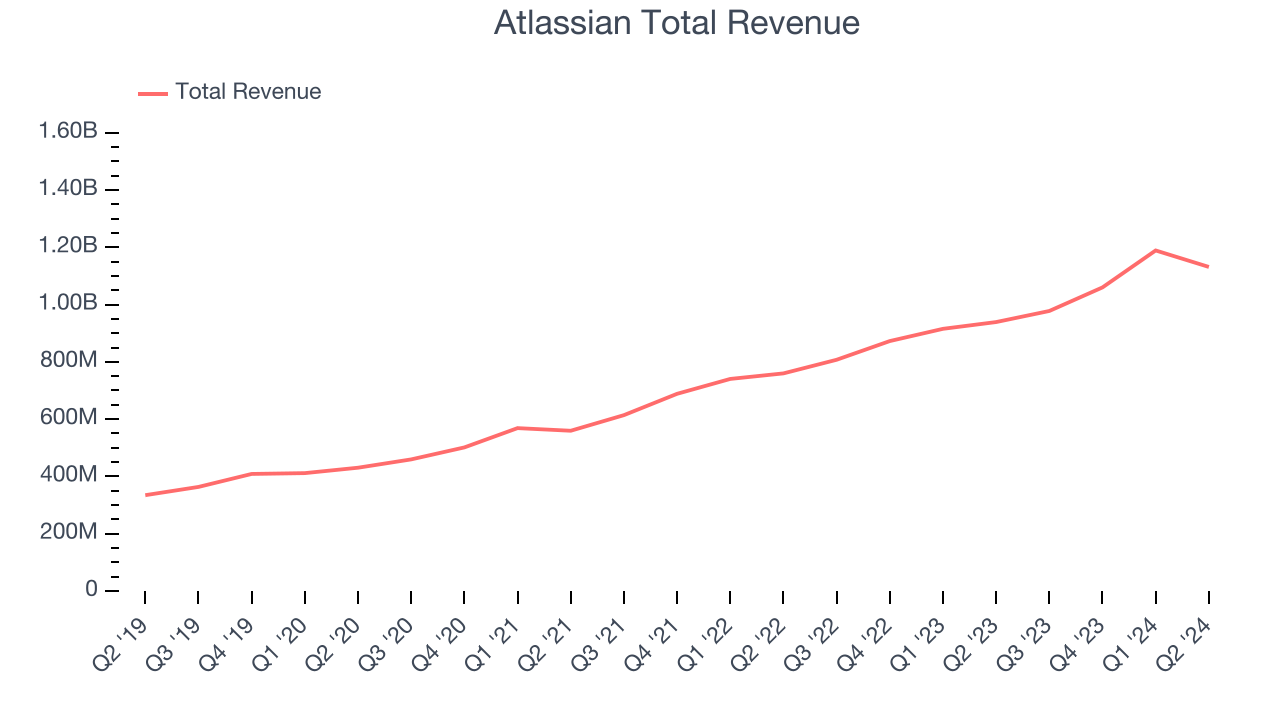

Sales Growth

As you can see below, Atlassian's revenue growth has been solid over the last three years, growing from $559.5 million in Q4 2021 to $1.13 billion this quarter.

This quarter, Atlassian's quarterly revenue was once again up a very solid 20.5% year on year. However, the company's revenue actually decreased by $57.54 million in Q2 compared to the $129 million increase in Q1 CY2024. While we'd like to see revenue increase each quarter, management is guiding for growth to rebound in the next quarter and a one-off fluctuation is usually not concerning.

Next quarter's guidance suggests that Atlassian is expecting revenue to grow 17.9% year on year to $1.15 billion, slowing down from the 21.1% year-on-year increase it recorded in the same quarter last year. For the upcoming financial year, management expects revenue to be $5.06 billion at the midpoint, growing 16% year on year compared to the 23.3% increase in FY2024.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) semiconductor stock benefitting from the rise of AI. Click here to access our free report on our favorite semiconductor growth story.

Gross Margin & Pricing Power

What makes the software-as-a-service model so attractive is that once the software is developed, it usually doesn't cost much to provide it as an ongoing service.

These costs include servers, licenses, and certain personnel, and leverage on them can decide the winners in competitive markets because they determine how much can be invested into new products, sales, and talent.

Atlassian's robust unit economics are better than the broader software industry, an output of its asset-lite business model and pricing power. They also enable the company to fund large investments in new products and sales during periods of rapid growth to achieve higher operating profits at scale. As you can see below, it averaged an impressive 81.6% gross margin over the last year. That means Atlassian only paid its providers $18.43 for every $100 in revenue to run its products and services.

Atlassian's gross profit margin came in at 80.8% this quarter, down 2.1 percentage points year on year. Atlassian's full-year margin has also been trending down over the past 12 months, decreasing by 1 percentage points. If this move continues, it could suggest a more competitive environment with some pressure to lower prices and higher input costs.

Key Takeaways from Atlassian's Q2 Results

We enjoyed seeing Atlassian exceed analysts' billings expectations this quarter. On the other hand, its full-year revenue guidance was below expectations and its revenue guidance for next year suggests a slowdown in demand. Overall, this was a bad quarter for Atlassian. The stock traded down 11.7% to $153.05 immediately after reporting.

Atlassian may have had a tough quarter, but does that actually create an opportunity to invest right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.

/AI%20(artificial%20intelligence)/AI%20microchip%20by%20DesignKingBD360%20via%20Shutterstock.jpg)