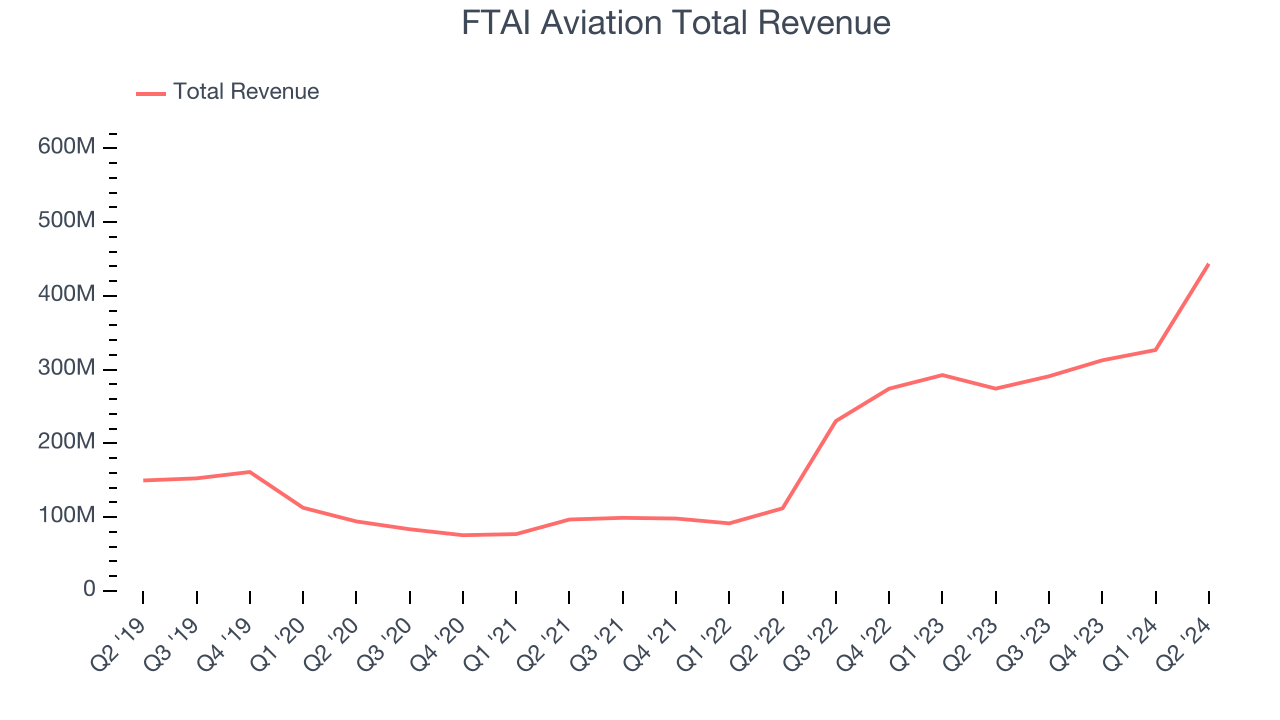

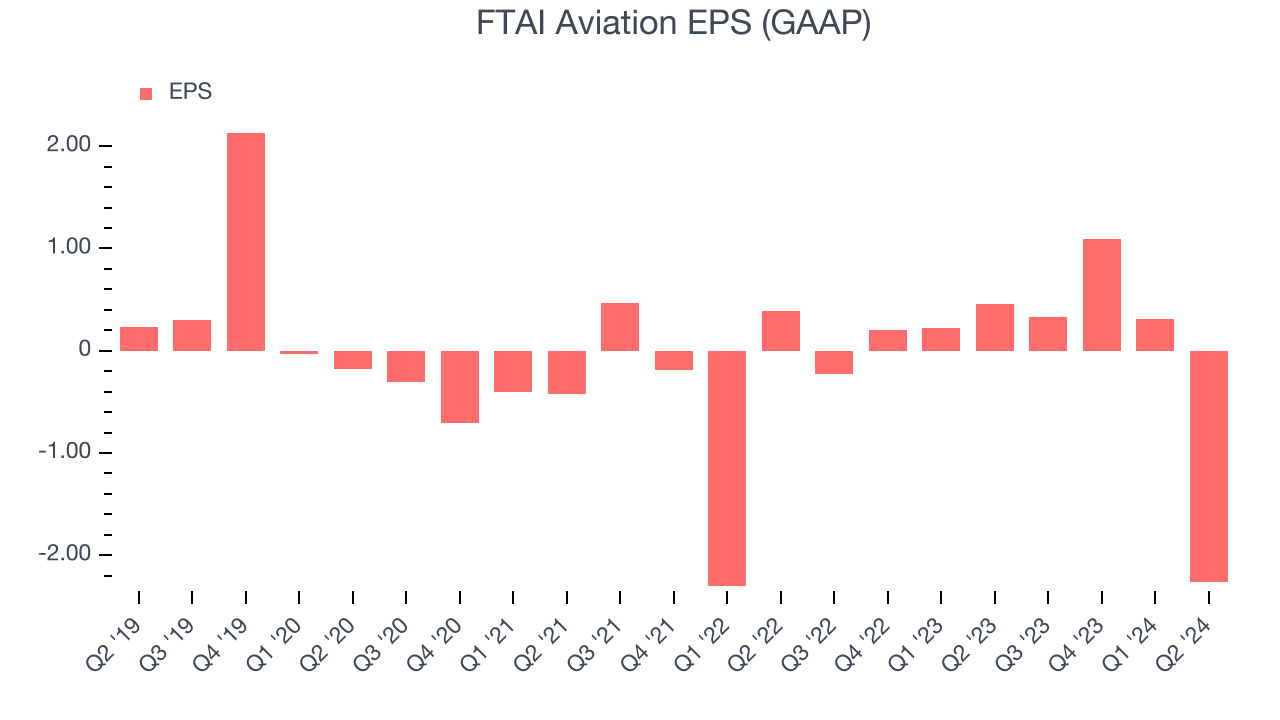

Aircraft leasing company FTAI Aviation (NASDAQ:FTAI) beat analysts' expectations in Q2 CY2024, with revenue up 61.7% year on year to $443.6 million. It made a GAAP loss of $2.26 per share, down from its profit of $0.46 per share in the same quarter last year.

Is now the time to buy FTAI Aviation? Find out by accessing our full research report, it's free.

FTAI Aviation (FTAI) Q2 CY2024 Highlights:

- Revenue: $443.6 million vs analyst estimates of $363.7 million (22% beat)

- Adjusted EBITDA: $213.9 million vs analyst estimates of $179.4 million (19.2% beat)

- Gross Margin (GAAP): 53.6%, up from 52.9% in the same quarter last year

- FTAI has inducted 20 V2500 engines year to date and expects to induct an additional 30 by year end.

- Market Capitalization: $10.55 billion

With a focus on the CFM56 engine that powers Boeing and Airbus’s aircrafts, FTAI Aviation (NASDAQ:FTAI) provides aircraft and engine leasing as well as the maintenance and repair of these products.

Vehicle Parts Distributors

Supply chain and inventory management are themes that grew in focus after COVID wreaked havoc on the global movement of raw materials and components. Transportation parts distributors that boast reliable selection in sometimes specialized areas combined and quickly deliver products to customers can benefit from this theme. Additionally, distributors who earn meaningful revenue streams from aftermarket products can enjoy more steady top-line trends and higher margins. But like the broader industrials sector, transportation parts distributors are also at the whim of economic cycles that impact capital spending, transportation volumes, and demand for discretionary parts and components.

Sales Growth

A company’s long-term performance can give signals about its business quality. Even a bad business can shine for one or two quarters, but a top-tier one tends to grow for years. Thankfully, FTAI Aviation's 22.7% annualized revenue growth over the last five years was incredible. This is a great starting point for our analysis because it shows FTAI Aviation's offerings resonate with customers.

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. FTAI Aviation's annualized revenue growth of 85.1% over the last two years is above its five-year trend, suggesting its demand was strong and recently accelerated.

This quarter, FTAI Aviation reported magnificent year-on-year revenue growth of 61.7%, and its $443.6 million of revenue beat Wall Street's estimates by 22%. Looking ahead, Wall Street expects sales to grow 12% over the next 12 months, a deceleration from this quarter.

When a company has more cash than it knows what to do with, buying back its own shares can make a lot of sense–as long as the price is right. Luckily, we’ve found one, a low-priced stock that is gushing free cash flow AND buying back shares. Click here to claim your Special Free Report on a fallen angel growth story that is already recovering from a setback.

Operating Margin

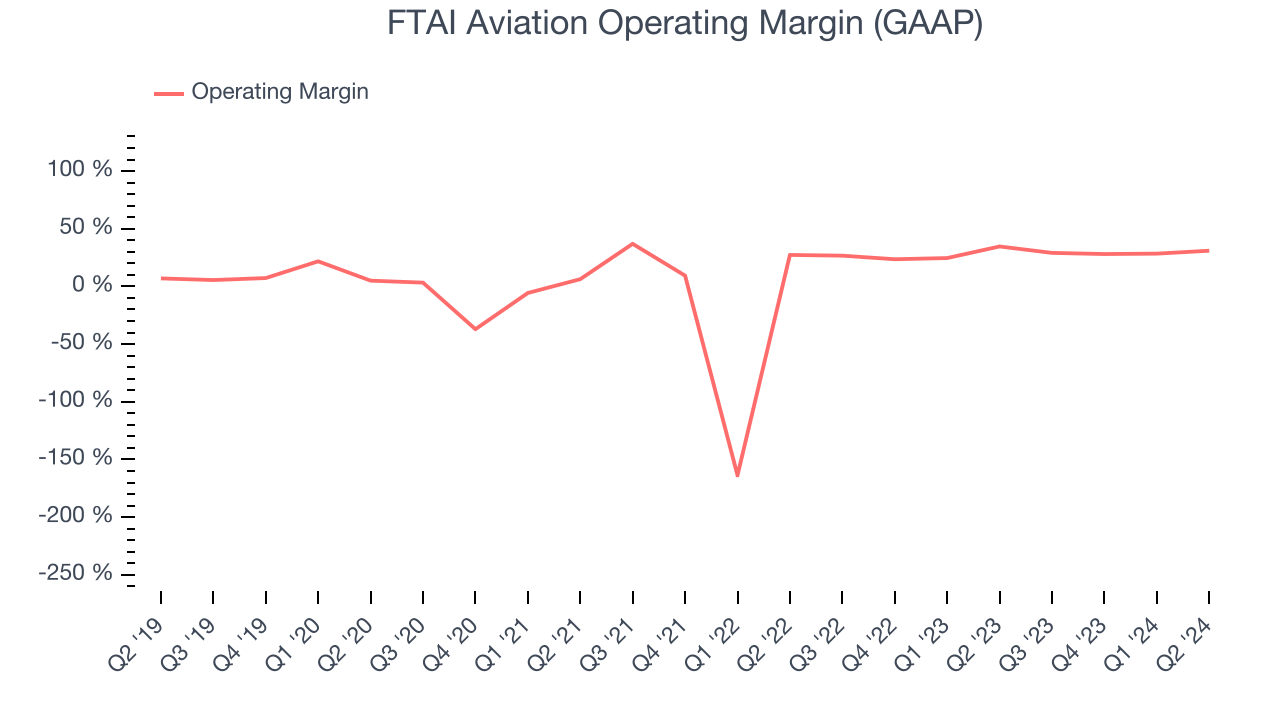

FTAI Aviation has been a well-oiled machine over the last five years. It demonstrated elite profitability for an industrials business, boasting an average operating margin of 17.5%. This isn't surprising as its high gross margin gives it a favorable starting point.

Looking at the trend in its profitability, FTAI Aviation's annual operating margin rose by 19.8 percentage points over the last five years, showing its efficiency has significantly improved.

In Q2, FTAI Aviation generated an operating profit margin of 31%, down 3.7 percentage points year on year. Since FTAI Aviation's operating margin decreased more than its gross margin, we can assume the company was recently less efficient because its general expenses like sales, marketing, and administrative overhead increased.

EPS

Sadly for FTAI Aviation, its EPS declined by 35.8% annually over the last five years while its revenue grew by 22.7%. However, its operating margin actually expanded during this timeframe, telling us non-fundamental factors affected its ultimate earnings.

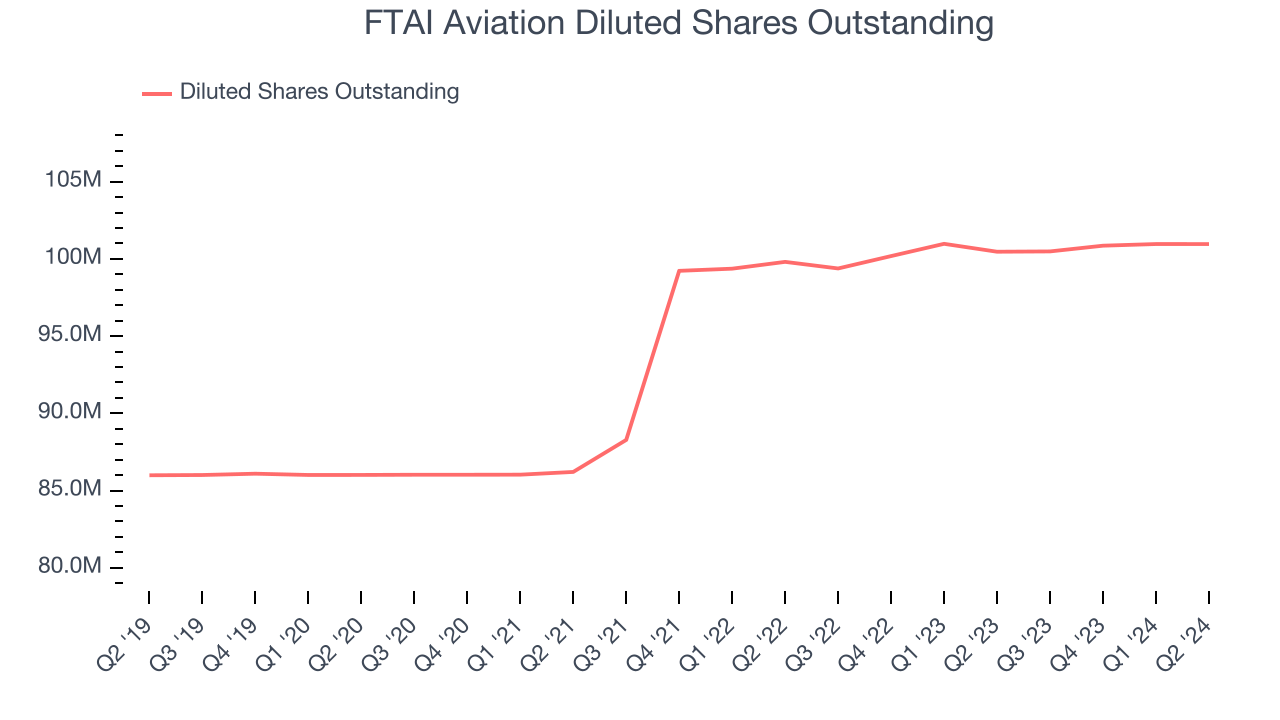

We can take a deeper look into FTAI Aviation's earnings to better understand the drivers of its performance. A five-year view shows FTAI Aviation has diluted its shareholders, growing its share count by 17.4%. This dilution overshadowed its increased operating efficiency and has led to lower per share earnings. Taxes and interest expenses can also affect EPS but don't tell us as much about a company's fundamentals.

Like with revenue, we also analyze EPS over a shorter period to see if we are missing a change in the business. For FTAI Aviation, its two-year annual EPS growth of 43.2% was higher than its five-year trend. This acceleration made it one of the faster-growing industrials companies in recent history.

In Q2, FTAI Aviation reported EPS at negative $2.26, down from $0.46 in the same quarter last year. This print missed analysts' estimates. Over the next 12 months, Wall Street is optimistic. Analysts are projecting FTAI Aviation's EPS of negative $0.53 in the last year to flip to positive $2.62.

Key Takeaways from FTAI Aviation's Q2 Results

We were impressed by how significantly FTAI Aviation blew past analysts' revenue and adjusted EBITDA expectations this quarter. This was driven by the Aerospace Products segment, which manufactures aftermarket components for engines and aircraft that is used in maintenance and repairs. The company also stated that it inducted 20 V2500 engines year to date and expects to induct an additional 30 by year end, showing that it is diversifying away from the core CFM56 engine that drives most of its business. Overall, this was a solid quarter for FTAI Aviation. The stock traded up 6.4% to $114.75 immediately following the results.

So should you invest in FTAI Aviation right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.

/Intel%20Corp_%20badge%20holder-by%20hasrul_rais%20via%20Shutterstock.jpg)

/Advanced%20Micro%20Devices%20Inc_%20logo%20on%20phone%20and%20website-by%20T_Schneider%20via%20Shutterstock.jpg)

/Palantir%20by%20Hiroshi-Mori-Stock%20via%20Shutterstock.jpg)

/Robinhood%20app%20on%20phone%20by%20Andrew%20Neel%20via%20Unsplash.jpg)