/Meta%20Platforms%20by%20Primakov%20via%20Shutterstock.jpg)

Social media giant Meta Platforms (META) recently acquired a 20% stake in Indian fintech firm Cred, investing $900 million, which now values it at $4.50 billion. Cred, launched in 2018, operates an app that commands 17 million monthly users and offers benefits to those who stay current on credit card payments. It also provides users with tools to monitor their spending habits.

However, the news has focused on Meta appointing Cred’s founder, Kunal Shah, as the new head of the messaging platform WhatsApp. Current WhatsApp CEO Will Cathcart is being moved to a new AI-focused role. Meta has used this strategy before, when it tied an approximately $14 billion investment in Scale AI to the recruitment of founder Alexandr Wang to its AI lab.

The Cred stake acquisition positions Meta as a beneficiary of the rapidly growing Indian fintech market, while also providing valuable leadership with a founder-like mentality.

About Meta Platforms Stock

Meta is one of the world’s most popular tech companies, known for Facebook, Instagram, WhatsApp, Messenger, and Threads. Its business is centered on social media, digital advertising, and growing investments in artificial intelligence and virtual reality. The company is also continuing to refine its product mix and operations to support long-term growth. Meta is headquartered in Menlo Park, California and has a massive market capitalization of $1.42 trillion.

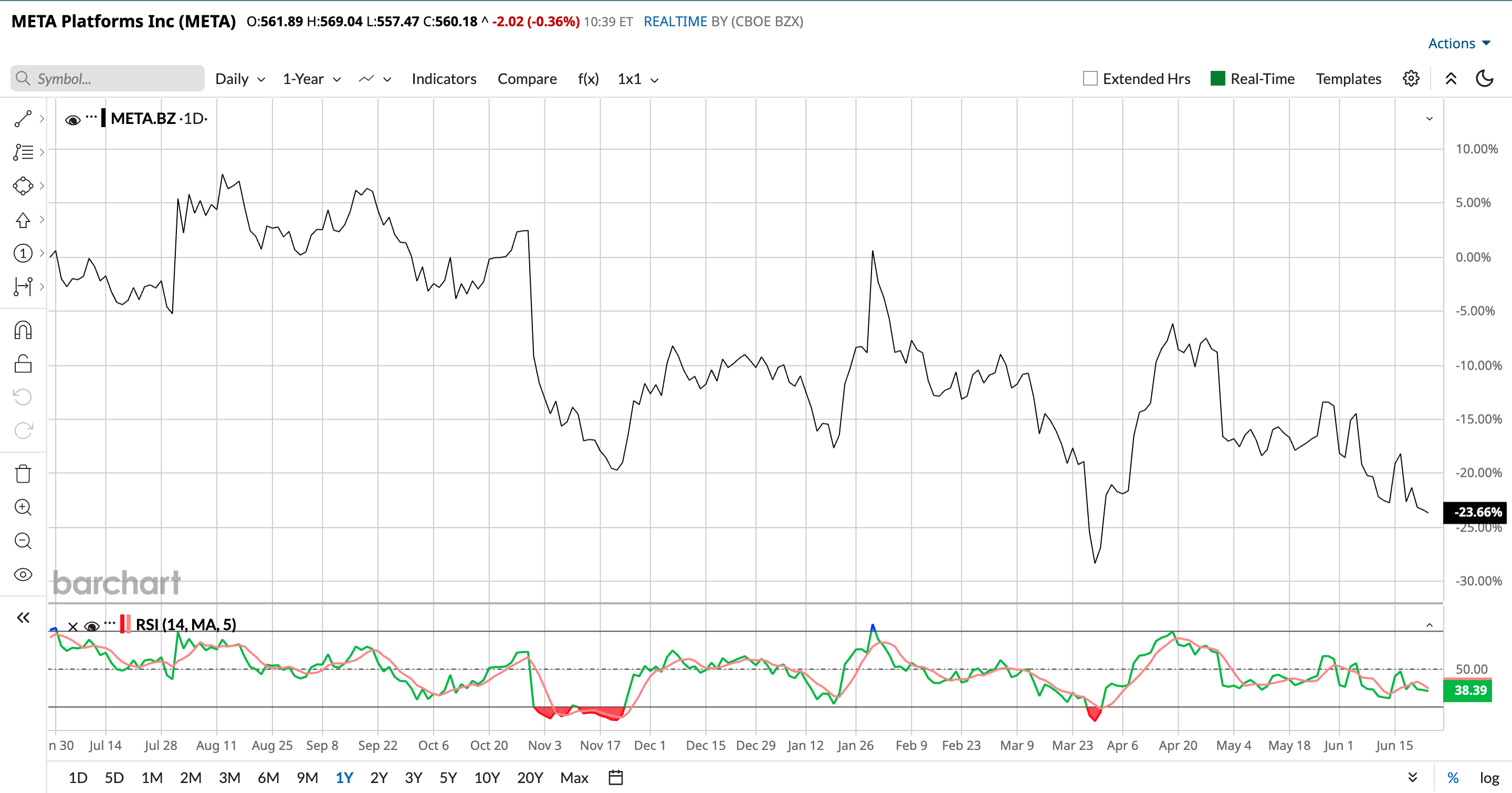

Meta has been down over the past year as investors have become more cautious about heavy AI spending. Over the past 52 weeks, Meta’s stock has dropped 20.96%, and it is down 14.72% year-to-date (YTD). The company’s shares reached a 52-week low of $520.26 on March 27, but are up 7.9% from that level.

Meta’s 14-day relative strength index (RSI) of 38.56 is closer to the oversold territory than the overbought territory. The sell-off has also brought down its valuation. On a forward-adjusted basis, the stock’s non-GAAP PEG ratio of 0.83 times is lower than the industry average of 1.21 times.

Meta Platforms Reported Q1 Results Driven by Ad Growth

For the first quarter of 2026, Meta reported 33% year-over-year (YOY) revenue growth to $56.31 billion, with advertising revenue climbing 33% YOY to $55.02 billion. Family daily active people averaged 3.56 billion in March 2026, up 4% from a year earlier. However, the quarter-over-quarter decline was mainly due to internet outages in Iran and restrictions on WhatsApp access in Russia.

Its Ad impressions across its Family of Apps rose 19% compared with the same period last year. Meta also released the first model from Meta Superintelligence Labs during the quarter. On the other hand, Meta’s operating margin stayed flat YOY at 41%. However, its EPS grew 62% YOY to $10.44. Meta’s capital expenditures continue to grow. For fiscal 2026, the company increased its planned capex to $125 billion to $145 billion, up from its prior range of $115 billion to $135 billion, reflecting additional data center costs to support capacity.

Wall Street analysts have mixed feelings about Meta’s future earnings. For the current fiscal year, EPS is projected to decrease 1.15% annually to $29.35, followed by a 19.32% growth to $35.02 in the next fiscal year. Moreover, analysts expect the company’s EPS to decline marginally YOY to $7.10 for the current quarter.

Here’s What Analysts Think About Meta Platforms’ Stock

This month, analysts at RBC Capital reiterated an “Outperform” rating and an $810 price target. Analysts believe that Meta is positioned at the crossroads of two trends that could expand its total addressable market: specialized computing power that helps uncover unexpressed demand, and a surge in AI-driven entrepreneurship.

Rosenblatt analysts reiterated a “Buy” rating and a $1,015 Street-high price target, as the company announced its plans to introduce subscription offerings for its major consumer services under the Meta One umbrella.

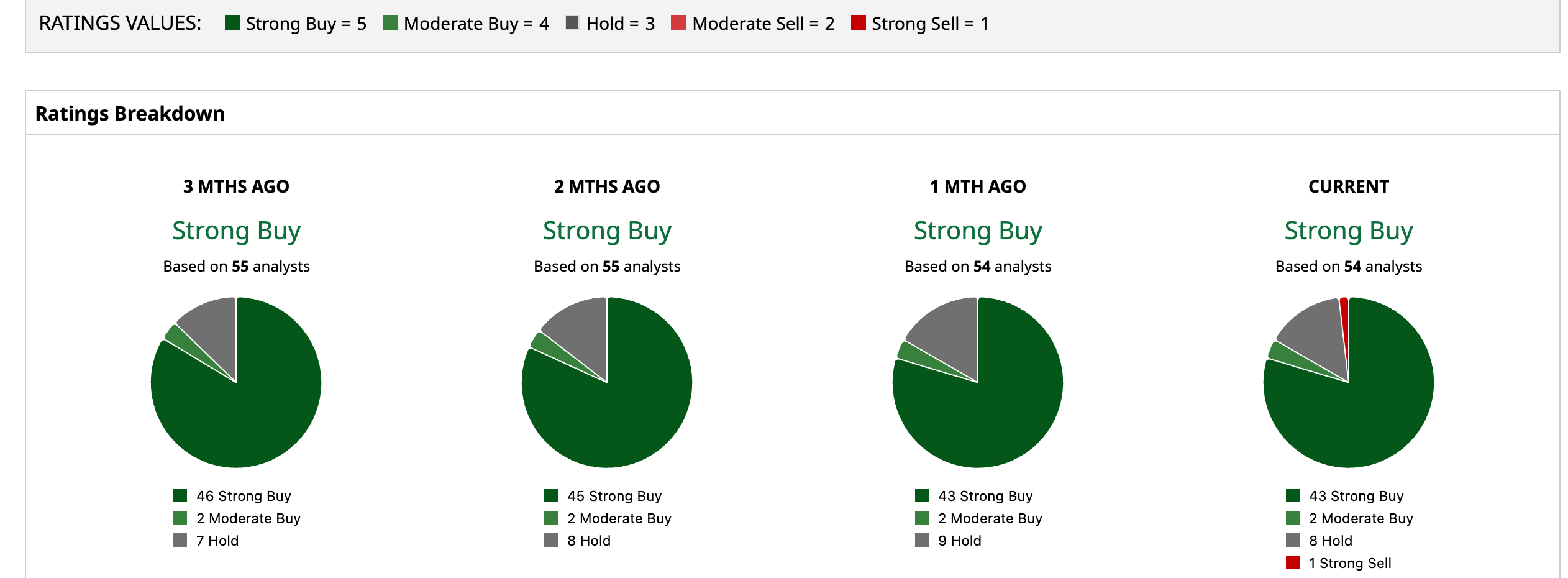

Meta has been in the spotlight on Wall Street, with analysts awarding it a consensus “Strong Buy” rating. Of the 54 analysts rating the stock, a majority of 43 analysts have rated it a “Strong Buy,” two analysts suggest a “Moderate Buy,” while eight analysts are playing it safe with a “Hold” rating, and one suggested “Strong Sell.” The consensus price target of $826.78 represents a 46.3% upside from current levels. The Street-high price target of $1,015 indicates a 79.6% upside.

On the date of publication, Anushka Dutta did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Arista%20sing%20at%20headquarters%20of%20an%20American%20multinational%20technology%20company%20Arista%20Networks%20-%20Santa%20Clara%2C%20California%2C%20USA%20-%202020%20By%20MichaelVi.jpeg)

/AI%20(artificial%20intelligence)/AI%20Data%20Center%20by%20Gorodenkoff%20via%20Shutterstock.jpg)