/AI%20(artificial%20intelligence)/AI%20software%20engineering%20by%20Tapati%20Rinchumrus%20via%20Shutterstock.jpg)

Memory chip giant Micron (MU) and the maker of the Claude generative AI platform, Anthropic, have inked a partnership wherein the latter will make use of the former's infrastructure to strengthen its memory supply. MU stock popped about 7% on the news but yesterday's “AI tech slump” wiped out those gains, for now at least.

That said, two things are not lost on anyone. First, there is a memory shortage around the world, and second, the competition among the likes of OpenAI, Alphabet's (GOOGL) (GOOG) Gemini, and Claude is fierce to be the leader in the AI market.

Within this context, the deal comes as a crucial win for Anthropic as it looks to hold on to its leading position. On the other hand, this marks another feather in the cap for Micron as it looks to embellish itself as the memory partner of choice for the West and thwart competition from South Korean giants like SK Hynix and Samsung.

Overall, the partnership will focus on enhancing memory and storage capabilities, along with energy efficiency, with the end goal of reducing the total cost of ownership, or TCO.

Commenting on the deal, Chief Business Officer at Micron, Sumit Sadana, said, “Micron’s strategic collaboration with Anthropic brings together the industry-leading capabilities of both companies to innovate and scale next-generation AI infrastructure.”

However, does this make the case for owning MU stock even stronger? Or, should this just be looked at as just a routine partnership expansion for Micron? Let's find out.

Micron in an Enviable Place

Amid the demand and supply imbalance in the world of memory chips, there is another steady catalyst working in favor of memory players in general and Micron in particular. It is agentic AI.

Projected to reach a market size of about $139 billion by 2034, agentic AI requires significantly more memory bandwidth than traditional inference workloads. In fact, demand has outpaced supply so severely that Micron's high-bandwidth memory capacity was sold out through the entirety of calendar year 2026, a disclosure made on the company's Q1 2026 earnings call.

Notably, the shift toward agentic AI will demand significantly higher levels of memory and storage capacity across cloud servers, private data centers, and edge computing environments, with this trend expected to expand the overall addressable market for both DRAM and NAND products. Here, Micron stands to benefit substantially as it advances its memory portfolio, including the introduction of its LPDRAM solution featuring the 256-gigabyte SOCAMM2 module that delivers greater memory capacity per central processing unit. Additionally, the industry transition from HBM3 to HBM4 is likely to tighten supply conditions further since these next-generation chips require more wafer area per bit of capacity.

How is Micron looking to meet this demand, though? Through new facilities.

Micron's response to surging memory demand is anchored in the most ambitious domestic fab buildout the company has ever attempted. In Idaho, Micron plans two advanced high-volume fabs co-located with its existing R&D operations in Boise, expected to create over 17,000 new jobs and accelerate time to market for high bandwidth memory, the product category most critical to AI demand. Idaho is the nearer term priority, with Micron reallocating roughly $1.2 billion in federal CHIPS Act support from New York to speed up the second Boise fab, alongside a dedicated advanced packaging facility built specifically to handle HBM and other stacked memory technologies.

Further, the New York campus near Clay is the larger, longer-dated bet. Micron's $100 billion megafab complex near Clay will become the largest semiconductor production facility in the state and one of the largest in the country, designed to produce 40% of the company's total domestic DRAM output once fully built, with construction of the first fab now set to begin in late 2026 and run through the second quarter of 2028, with operations expected to start as early as 2030. The full four fab buildout is now staggered through 2041, a roughly five-year extension from Micron's original schedule, with Fab 2 starting construction in late 2030, Fab 3 in mid 2035, and Fab 4 shortly after.

Solid Q2

Micron posted outstanding results for the second quarter of 2026, with revenue reaching $23.9 billion. This represented a fourfold increase compared with the year-earlier period. Every business segment delivered year-over-year (YoY) growth of more than 150%. The Mobile and Client Unit stood out with a 244% rise to $7.71 billion, while the important Data Center segment advanced 211% to $5.69 billion.

Gross margins nearly doubled to 74.9% from 37.9% in the prior year period, reflecting robust demand and the company's competitive strength. Earnings per share surged to $12.20 from just $1.56 in the year-ago quarter, easily topping consensus estimates. This marked the ninth consecutive quarter in which the company exceeded profit forecasts.

Net cash from operating activities for the six months ended February 26, 2026, totaled $20.3 billion, compared with $7.2 billion in the same period a year earlier. Micron ended the quarter with $13.9 billion in cash, substantially higher than its short-term debt balance of $585 million.

For the third quarter of 2026, Micron guided for revenue between $32.75 billion and $34.25 billion. Earnings per share are projected in the range of $18.75 to $19.55. Analysts currently anticipate revenue of $33.59 billion and earnings per share of $19.15.

On valuation, Micron shares continue to appear relatively attractive. The forward P/E ratio of 18.59 times sits below the sector median, while the forward P/S ratio stands at 11.29 times.

Valued at a market cap of $1.3 trillion, MU stock is up a sensational 324.4% on a year-to-date (YTD) basis. Notably, the company is set to report its Q3 earnings today, June 24, after the markets close.

Analyst Opinion on MU Stock

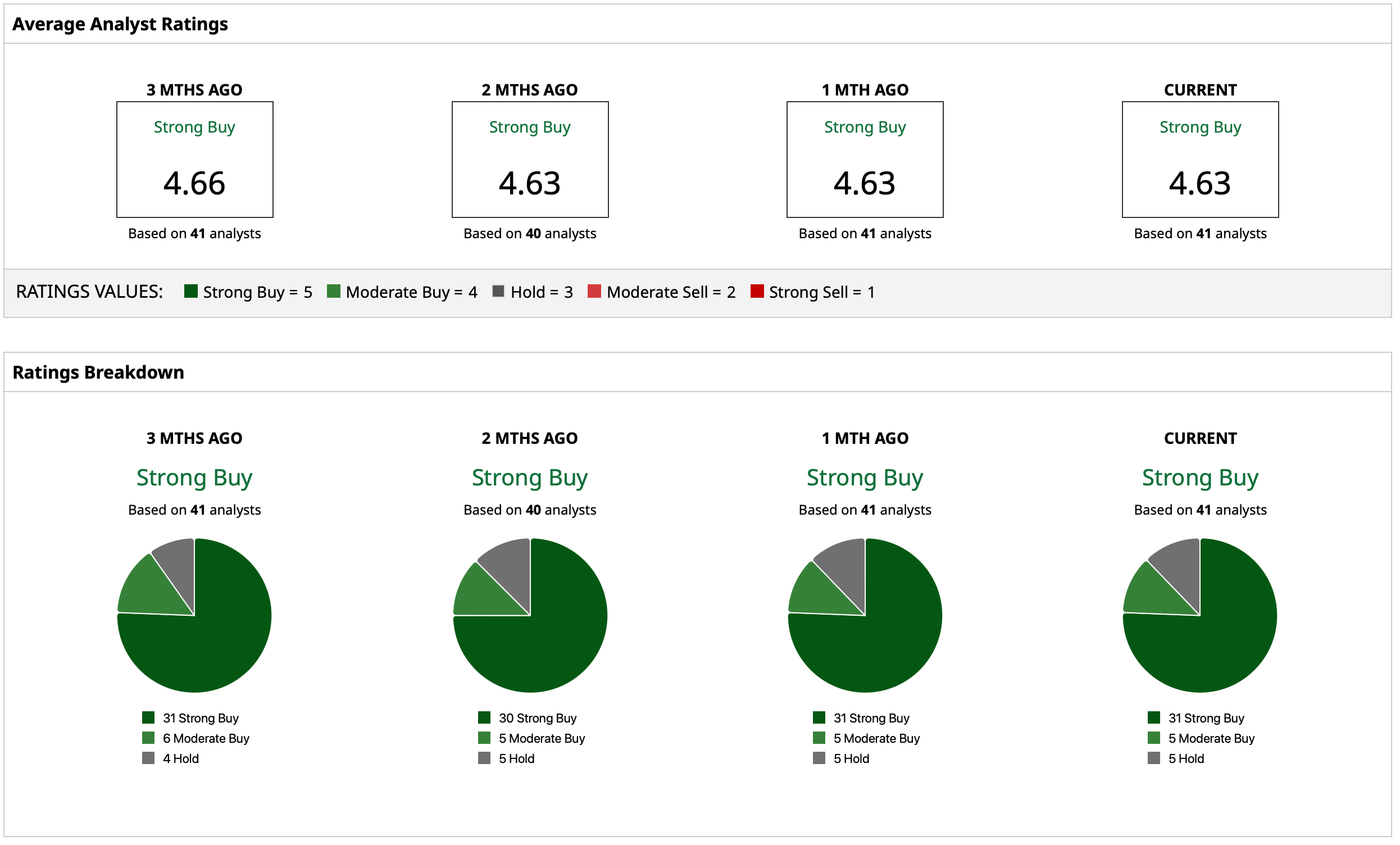

Considering this, analysts have deemed MU stock to be a consensus “Strong Buy” with a mean target price of $1,058.91 that the stock is currently hovering around. The high target price of $1,750 indicates an upside potential of about 67% from current levels. Out of 41 analysts covering the stock, 31 have a “Strong Buy” rating, five have a “Moderate Buy” rating, and five have a “Hold” rating.

On the date of publication, Pathikrit Bose did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/An%20Intel%20sign%20out%20front%20of%20a%20corporate%20office%20by%20wolterke%20via%20Adobe%20Stock.jpeg)

/Alibaba%20by%20testing%20via%20Shutterstock.jpg)

/Alphabet%20(Google)%20Image%20by%20Markus%20Mainka%20via%20Shutterstock.jpg)