/AI%20(artificial%20intelligence)/AI%20technology%20concept%20by%20NMStudio789%20via%20Shutterstock.jpg)

At a quick glance, Qualcomm (QCOM) seems unattractive, with second-quarter fiscal 2026 revenue declining by 3% on a year-over-year (YOY) basis. The negative catalyst for the company was a decline in QCT handset revenue on the back of memory supply constraints. However, even with the headwinds, QCOM stock has trended higher by 47% in the last 52 weeks.

The rally can be attributed to two factors. First, Qualcomm expects QCT handset revenue from China to reach a bottom in Q3, then “return to sequential growth in the following quarter.” Second, QCOM stock is pricing the AI diversification and its impact on growth. As a matter of fact, Qualcomm already has a custom silicon engagement with a major hyperscaler. Initial shipments are expected toward the end of 2026 and its entry into the data-center business is likely to create value.

There seems to be more good news brewing, too. Reports suggest that Qualcomm is in discussions to acquire Tenstorrent, a startup that designs specialized chips for AI models. If the acquisition is finalized, it would support Qualcomm’s diversification efforts. It’s worth noting that Qualcomm also completed the acquisition of Alphawave Semi, which has expertise in improving the speed of data transmission between chips, in late 2025.

About Qualcomm Stock

Headquartered in San Diego, California, Qualcomm is involved in the development and commercialization of foundational technologies for the wireless industry globally. The company derives revenue primarily from the sale of integrated circuit products, system-based solutions, and the licensing of its intellectual property.

Qualcomm’s business segments include Qualcomm CDMA Technologies (QCT), which is its semiconductor business, and Qualcomm Technology Licensing (QTL), which is its licensing business. For the first half of fiscal 2026, the firm reported revenue of $22.9 billion. For the same period, operating cash flow was robust at $7.4 billion.

While the company’s growth has been impacted by headwinds for the handset industry, the AI infrastructure opportunity is significant. As a result, QCOM stock has trended higher by 27% in the last six months.

JPMorgan Expects Significant Growth Acceleration

Ahead of Qualcomm’s upcoming Investor Day on June 24, JPMorgan analyst Samik Chatterjee has a positive view of the company. Chatterjee believes that data-center revenues will swell from $3 billion in fiscal 2027 to $35 billion by fiscal 2031.

At the same time, the analyst expects robust growth in automotive revenue coupled with an “inflection in growth rate for IoT.” Overall, double-digit revenue and earnings compound annual growth rates (CAGR) are likely in the next few years.

Recently, Qualcomm CEO Cristiano Amon also disclosed that the company is working on “over 40 designs of new AI devices.” This is indicative of potential for growth within the consumer electronics segment.

What Do Analysts Say About QCOM Stock?

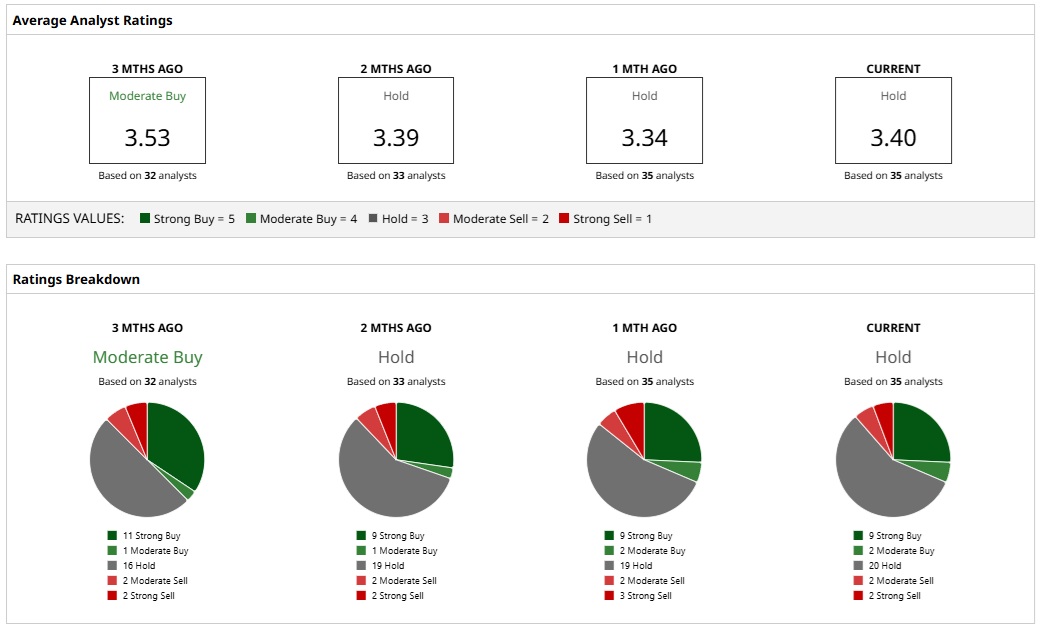

Based on 35 analysts with coverage, QCOM stock has a consensus “Hold” rating. While nine analysts have a “Strong Buy” rating for QCOM stock, two have a “Moderate Buy,” 20 have a “Hold,” two have a “Moderate Sell” rating, and two analysts have a “Strong Sell” rating.

The mean price target of $187.24 represents potential downside of 16% from current levels. However, the most bullish price target of $300 suggests that QCOM stock could climb as much as 35% from here.

Conclusion

Growth has been a concern for Qualcomm, and that is reflected in the forward price-to-earnings (P/E) ratio of 28.2 times. However, with custom silicon ramp-up in the cards coupled with broad-based AI diversification, the growth outlook is positive.

Another important point to note is that Qualcomm is working with industry partners to accelerate the development and global deployment of 6G. The company is designing 6G on an AI native system and commercialization will support growth from 2029.

From a financial perspective, Qualcomm is likely to report annualized operating cash flow of more than $14 billion. This will provide ample flexibility to pursue acquisitions that drive innovation. At the same time, shareholder value creation will continue through dividends and share repurchases. Therefore, with multiple positives, Qualcomm appears to be positioned for value creation.

On the date of publication, Faisal Humayun Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Microsoft%20sign%20at%20the%20headquarters%20by%20VDB%20Photos%20via%20Shutterstock.jpg)