/A%20concept%20image%20showing%20a%20lightbulb%20with%20planet%20earth%20in%20a%20mossy%20green%20background%20by%20Capt_Pic%20via%20Shutterstock.jpg)

Barclays recently upgraded Enphase Energy (ENPH), citing two primary catalysts: the firm’s emerging solid-state transformer business targeting data centers and the commencement of new IQ9S-3P Commercial Microinverter shipments in the U.S.

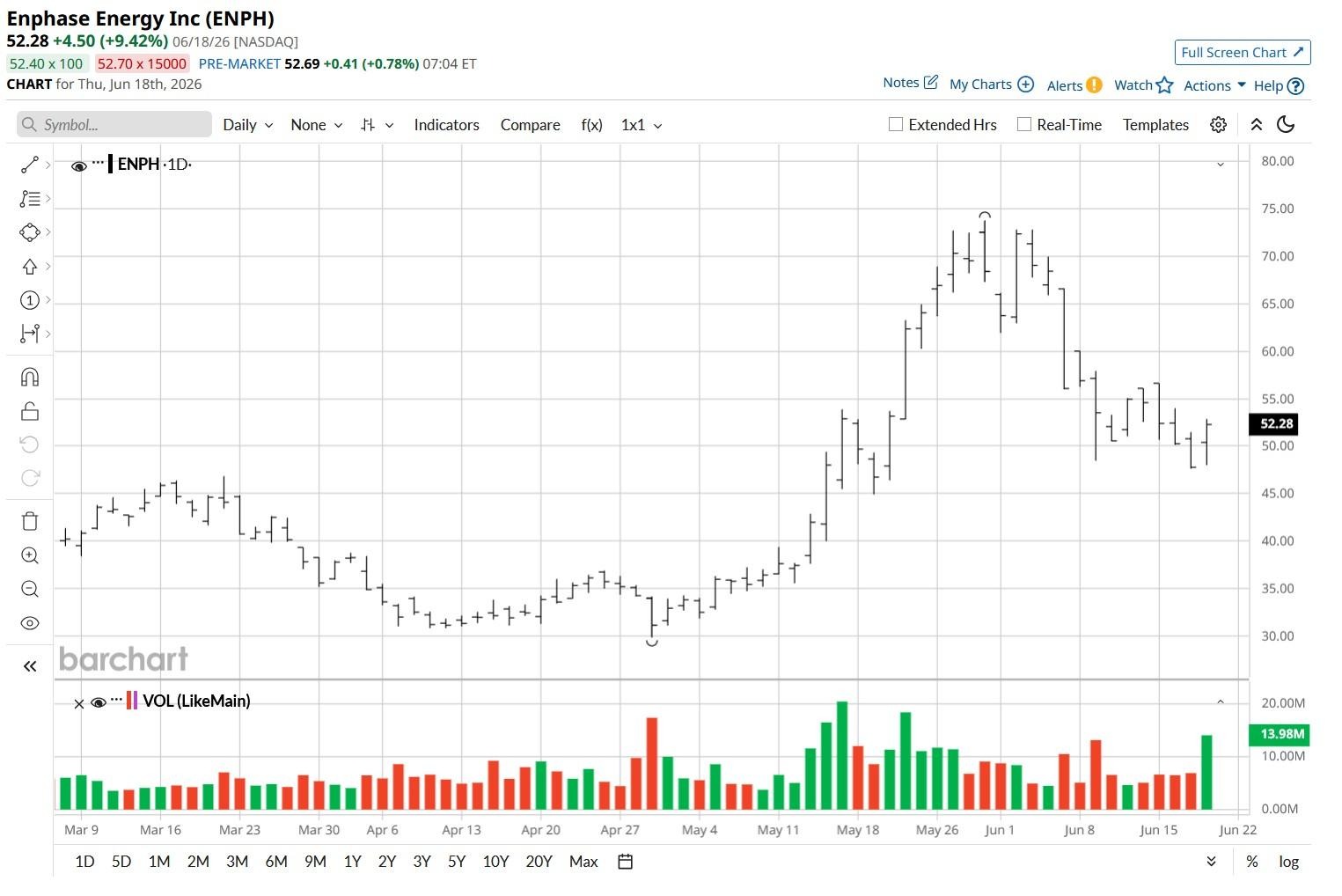

The bullish note arrives at a pivotal moment for Enphase stock, which is down about 27% versus its year-to-date high in the first week of June.

Here’s Why Enphase Stock Is Attractive to Own

The solid-state transformer opportunity positions ENPH at the intersection of two powerful secular trends: the explosive growth in AI-driven data center demand and the need for more efficient power conversion infrastructure.

Globally, the artificial intelligence-driven energy market is projected to grow from $5.1 billion in 2025 to a whopping $22.2 billion by 2033, representing a 20.4% compound annual growth rate, which provides a sustainable addressable market for Enphase’s data center-focused products.

Meanwhile, the IQ9S-3P is positive for ENPH shares as well, given it extends the company’s reach into the higher-capacity commercial solar segment — diversifying revenue beyond the residential market that has been a source of investors' concern.

The bull thesis rests mostly on persistent global electrification trends, including rising utility rates, grid instability, and transportation electrification, all of which are expected to drive demand for Enphase’s integrated solar, battery, and EV charging ecosystem.

These dynamics should support both revenue growth and higher-margin recurring service streams over time. The broader renewable energy integration opportunity remains the largest application segment for AI-enabled energy solutions, accounting for 33% of the global market in 2025.

Owning ENPH Shares Isn’t Free From Risk

However, meaningful risks temper the optimistic outlook. Tariff pressures on hardware imports could compress margins, while a potential slowdown in U.S. residential solar installations threatens the firm’s core revenue base.

The three-year and five-year total shareholder returns remain sharply negative, reinforcing that the recent momentum represents more of a rebound from depressed levels than a sustained recovery to prior highs.

Investors must weigh whether the data center opportunity and commercial microinverter expansion can sufficiently offset these headwinds to justify current valuations.

ENPH shares currently trade at a price-to-earnings ratio (P/E) multiple of about 51x, which stands in stark contrast to peer First Solar’s (FSLR) 16.5x, highlighting the premium the market has assigned to Enphase's growth profile.

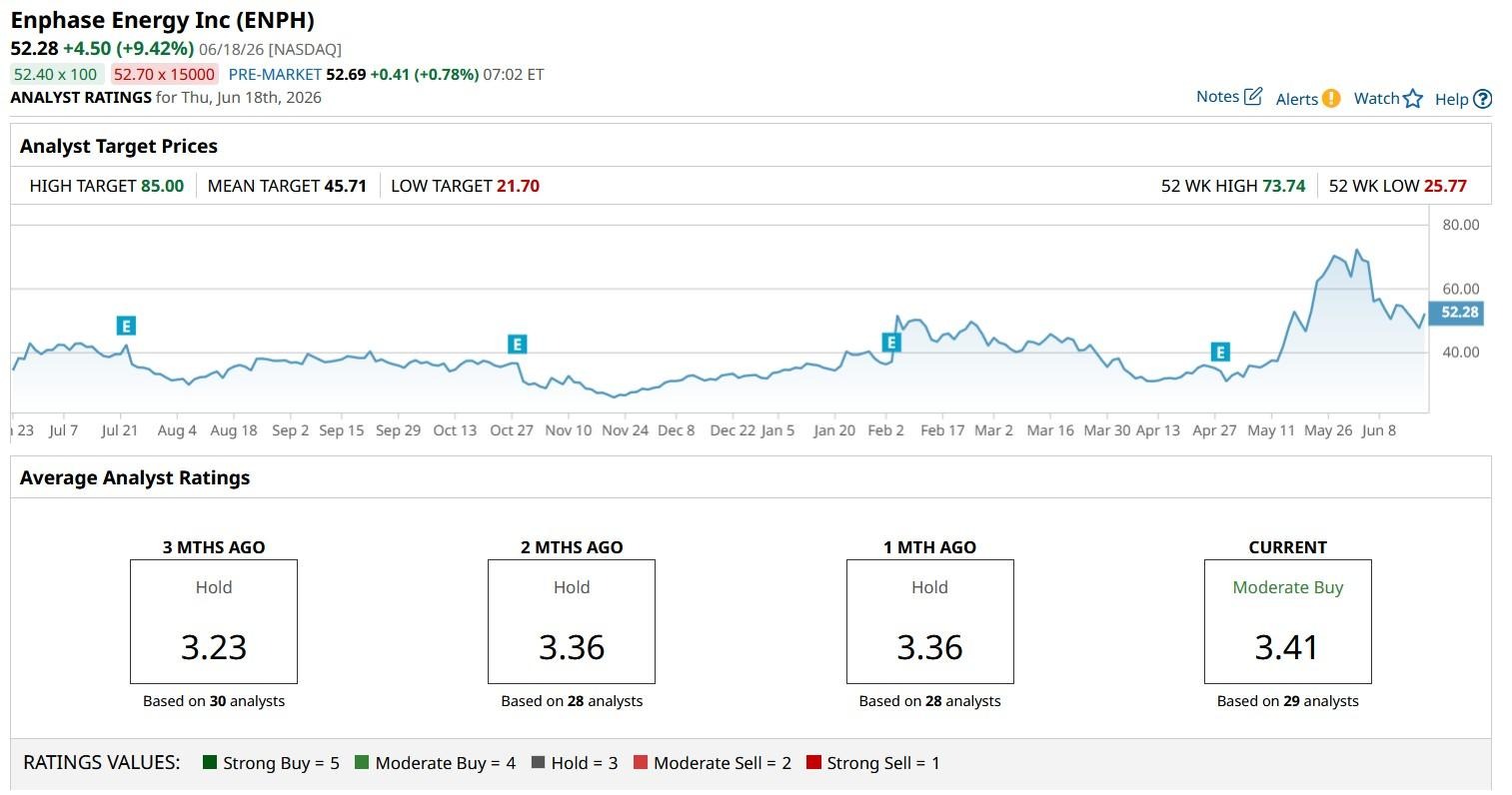

Moreover, while the consensus rating on Enphase shares sits at “Moderate Buy” currently, the mean price target is set at $45.71, implying they’re overvalued by more than 14% at the time of writing.

On the date of publication, Wajeeh Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Microsoft%20sign%20at%20the%20headquarters%20by%20VDB%20Photos%20via%20Shutterstock.jpg)

/Space/Cargo%20spacecraft%20in%20low-Earth%20orbit%20by%20Paopano%20via%20Shutterstock.jpg)