%20destroying%20a%20cancer%20cell%20by%20Alpha%20Tauri%203D%20Graphics%20via%20Shutterstock.jpg)

Born from a healthcare spin-off of 3M Company (MMM), the Eagan, Minnesota-based Solventum Corporation (SOLV) develops a wide range of medical products, dental solutions, and healthcare software. The company’s portfolio stretches across wound care, surgical products, infection prevention solutions, dental and orthodontic treatments, and health information systems.

At roughly $13 billion in market value, Solventum sits comfortably in the “large cap” camp, a category reserved for companies worth more than $10 billion. The financial muscle allows the company to serve hospitals, clinics, dental professionals, and healthcare organizations through direct sales teams, distributors, key accounts, and digital channels.

Despite the reach, the stock has not exactly been firing on all cylinders. Solventum’s shares currently trade 14.5% below their 52-week high of $88.20, a peak it reached in December 2025.

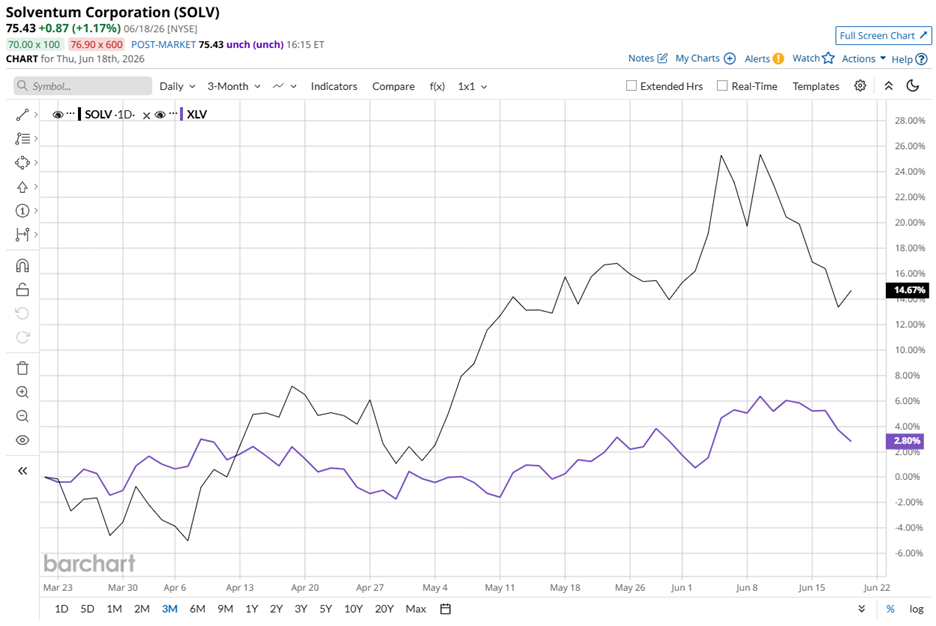

That said, the stock has shown signs of life lately. Over the past three months, SOLV stock climbed 12.4%, while the State Street Health Care Select Sector SPDR ETF (XLV) managed a far more modest gain of 1.5%.

The longer-term numbers, however, tell a different story. Over the past 52 weeks, SOLV stock gained 3.9%, while XLV advanced 12.1%. The gap remains noticeable on a year-to-date basis as well. SOLV stock has slipped 4.8% since the start of the year, while the healthcare ETF has fallen 3.5%. Put simply, Solventum won the recent sprint, yet the sector still holds the lead in the marathon.

The technical picture has become more encouraging in recent months. Since early May, SOLV stock has been trading above both its 50-day moving average of $73.33 and its 200-day moving average of $74.38.

Investors had another reason to cheer on May 5, as the stock gained 2.4% following Solventum’s Q1 FY2026 results. Revenue declined 3% year over year to $2.01 billion, although it still topped analyst estimates of $1.97 billion. Meanwhile, adjusted EPS rose 10.4% from the prior year to $1.48 and exceeded Wall Street's target of $1.35.

The company pointed to ongoing transformation initiatives, portfolio adjustments, and new product launches as key drivers behind its performance. Management believes these efforts still have room to run. CEO Bryan Hanson highlighted nearly 20 new products scheduled to launch over two years.

Management also struck a confident tone for full FY2026. The company expects adjusted EPS to land toward the high end of its existing guidance range of $6.40 to $6.60. Solventum also anticipates generating approximately $200 million in free cash flow for the year.

Even so, investors cannot evaluate Solventum in a vacuum. Competition remains fierce, and one rival has been running circles around much of the field. DaVita Inc. (DVA) delivered a stunning 53.1% gain over the past 52 weeks and has soared 83% YTD. Against numbers like these, Solventum's performance loses some of its shine.

Still, Wall Street has not turned its back on the stock. Among 15 analysts covering Solventum, the overall recommendation stands at “Moderate Buy.” Analysts also have an average price target of $83.54, signaling 10.8% upside from current levels.

On the date of publication, Aanchal Sugandh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20close-up%20of%20a%20SpaceX%20sign%20by%20Sundry%20Photography%20via%20Adobe%20Stock.jpeg)

/Microsoft%20France%20headquarters%20by%20JeanLuclchard%20via%20Shutterstock.jpg)

/A%20photo%20of%20a%20Sandisk%20Solid%20State%20Drive%20by%20Top%20Popular%20Vector%20by%20Shutterstock.jpg)