Happy Father’s Day market watchers!

It is time to thank and celebrate all the dad’s out there! It has been the best blessing in my life to be a dad and let us all spend more time with our families!

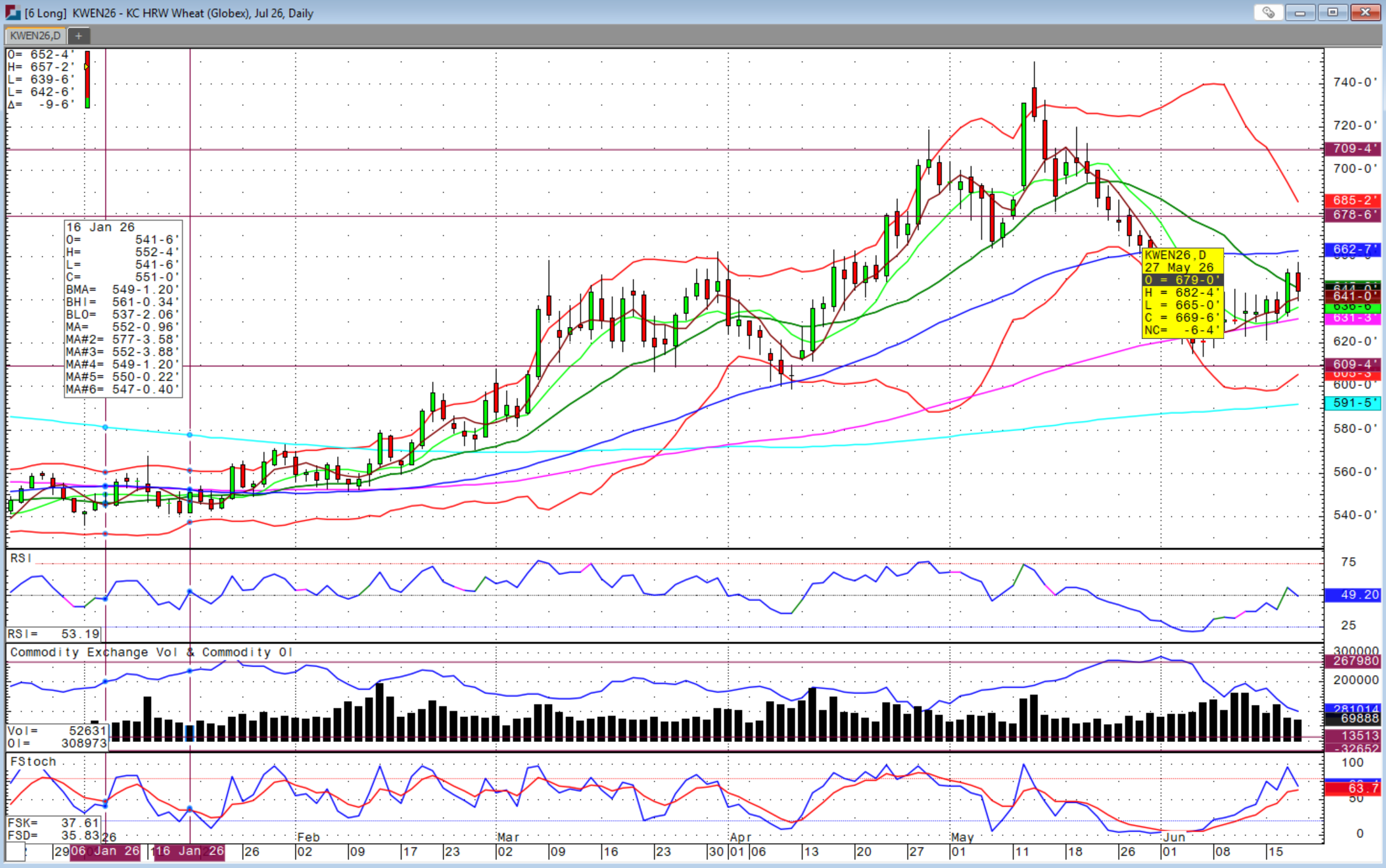

Wheat harvest is wrapping up in the Southern Plains and advancing north in between continued rain and thunderstorms. In the Midwest, torrential rains and even tornados continued to dominate the month of June. While moisture this time of year is great for summer crops, it can also limit root development that will be needed if July and August turn hotter and drier as they often do. Regardless, large crops are expected for the year ahead as conditions have stabilized.

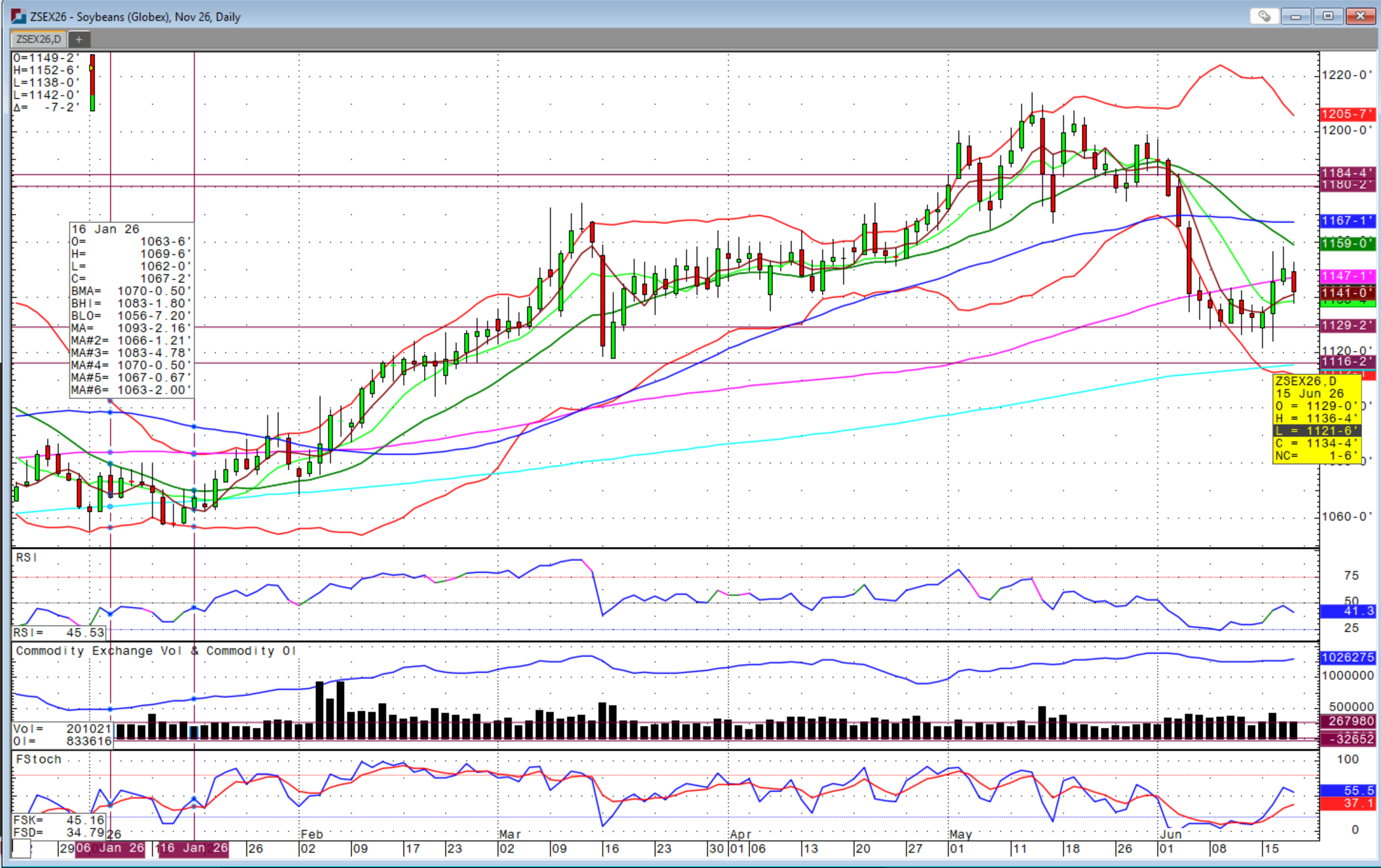

US corn conditions were rated 68 percent Good-to-Excellent as of Sunday, June 14th, which was in line with expectations and a one percent improvement over last week, but still behind last year’s 72 percent. Soybean conditions came in at 66 percent G/E, in line with expectations as well as last year and one percentage point ahead of last week. With 25 percent of the US winter wheat crop harvested, conditions mean less, but improved one percent above last week to 27 percent versus 52 percent last year.

The pace of winter wheat harvest is well ahead of normal given this year’s warmer, dryer conditions with only 13 percent harvested on average.

US spring wheat conditions remain only slightly below average at 55 percent G/E versus last year’s 57 percent. Cotton conditions came in at 50 percent G/E, deteriorating by 3 percent from last week, but still above last year’s 48 percent.

Grain and oilseed futures prices finally started to make higher highs and higher lows this week after a brutal 5-6 weeks of relentless selling by the funds. This price action was largely attributed to China returning to the US market with the first news of confirmed soybean sales in months. We are expecting China interest in wheat and possibly corn and hopefully we will see some activity in the weeks ahead.

Wheat markets found footing this week supported by concerns of heat in parts of Europe and Russia wheat areas as well as disease in US SRW.

Agriculture markets were closed on Friday for Juneteenth while energy and equity indices had an abbreviated session that closed at noon.

The first FOMC meeting and press conference featuring the new Fed Chair Warsh was this Wednesday after the announcement that the committee decided to leave interest rates unchanged. As the page turns to Chair Warsh from Chair Powell, the contrast in style was stark. Firstly, the statement released to the public and the press was very succinct. Similarly, the press conference that followed was that of minimal explanation with multiple references back to the statement. Fed Chair Warsh also refrained from communicating a dot in the dot plot that committee members release to foreshadow interest rate bias for the future.

Bottomline, the level and frequency of communication by Fed Chair Warsh will be less than his predecessor, which is intentional and tactful. One thing for sure is that Fed Chair Warsh intends to ensure price stability, ie, tame inflation, as he alluded to multiple times during the press conference. This means higher interest rates if inflationary pressures remain elevated. The selloff in crude oil this week is what is needed to get the bulk of inflation under control.

While President Trump was at the G7 this week in France, he signed the much anticipated and tweeted “deal” with Iran at the Palace of Versailles. There was a lot of confusion about when and who from the US would actually sign the agreement as it was thought to be Vice President Vance at the end of the week in Switzerland, but then we learned Trump signed in earlier. On Friday, there was talk that follow-up meetings were cancelled that signaled some potential disagreement, likely stemming from Israel’s additional attacks in Lebanon.

Frankly speaking, I do not have a good feeling about this deal. While I of course hope that there will be peace in the Middle East for the sake of families just trying to live their lives, the global economy and the supply of critical energy items around the world, I am concerned we have achieved nothing over these four months and possibly worsened the situation by leaving the same terrorist regime in charge.

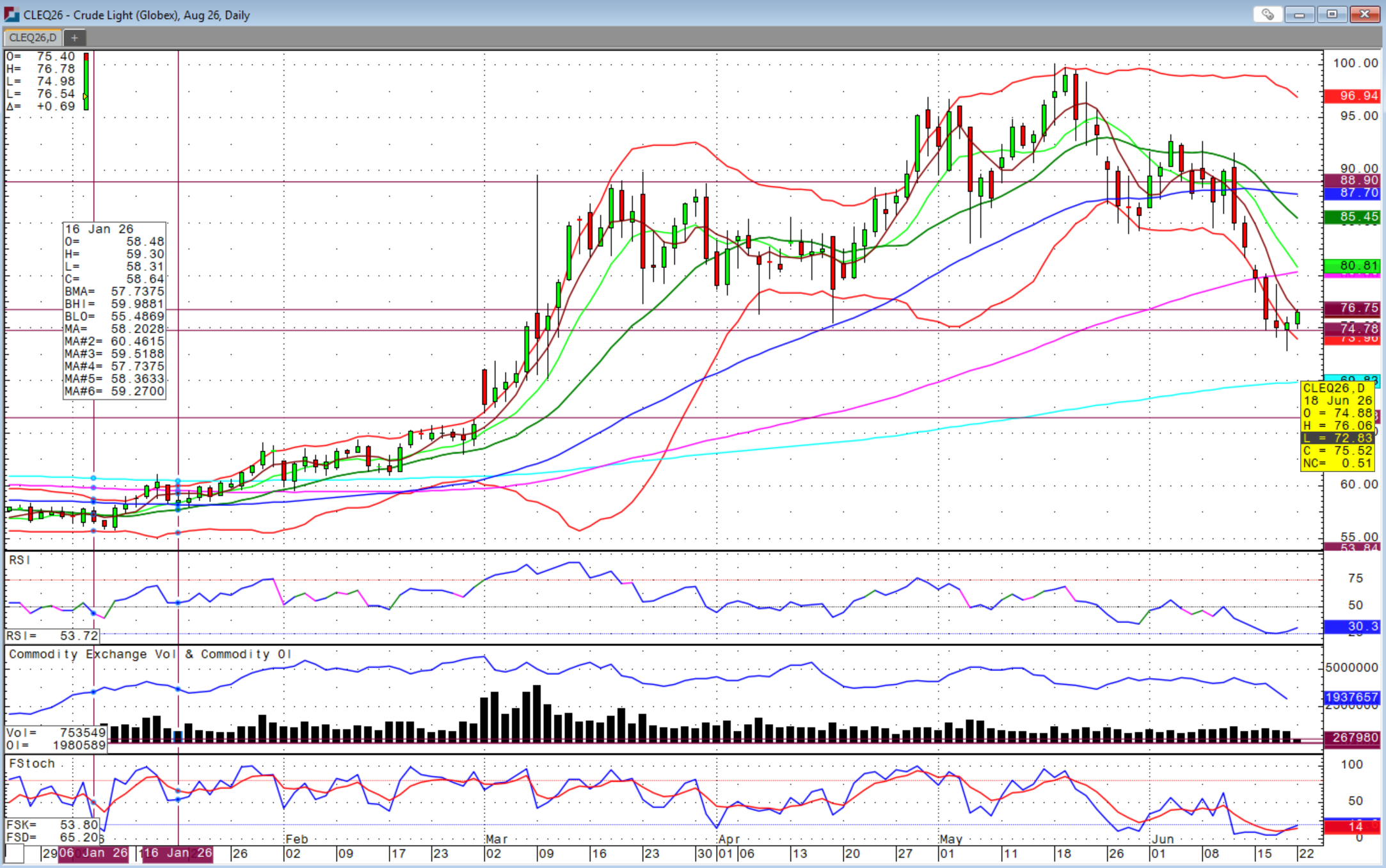

I foresee the Strait of Hormuz will experience on-again, off-again access as the Iranian Regime continues to demand money and the reduction of sanctions or just continue to threaten and toy with the politics and timeliness of elections in global democracies that is not an issue in their system of government. We will just have to see what happens, but I would not trust that the war volatility is over by any means. In fact, crude oil prices rallied Friday after a new low, but then strong, higher close in Thursday’s session. Pay attention to headlines over the weekend for the Sunday evening market opening.

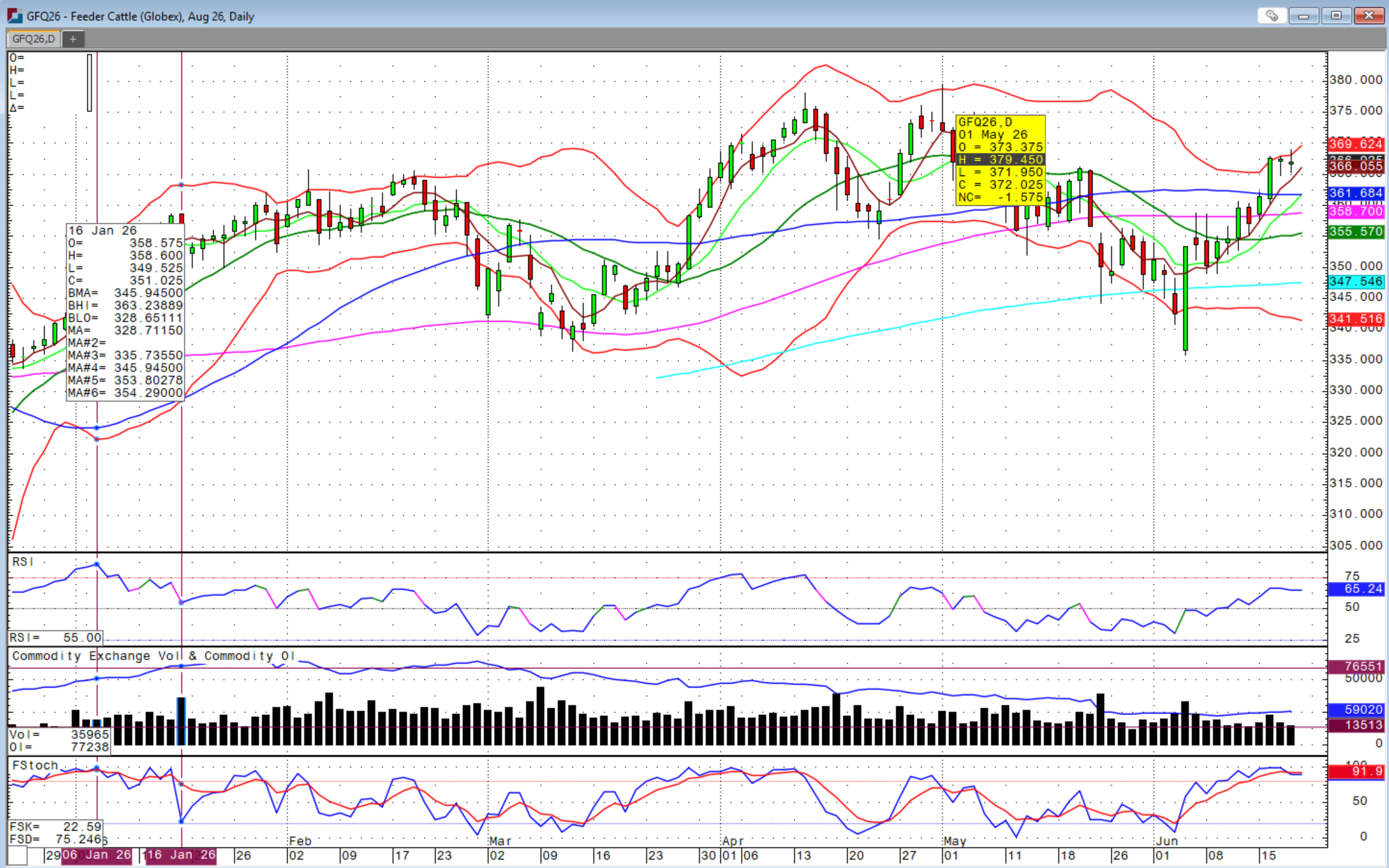

The cattle market has welcomed cheaper corn and stronger equity markets from the selloff in crude. Feeder cattle futures have rallied over $33 per cwt from the low on June 4th to Thursday’s high. The charts still look bullish. The all-time high on August feeders was $379.450 on May 1st versus Thursday’s high at $369.025. August fed cattle futures surged Tuesday, as did feeders, and actually made the 2nd highest close on record at $249.125 versus the all-time high close at $249.475 on April 29th. Thursday’s high came in just shy of the May 18th high at $249.975 versus the all-time high trade at $251.650 on May 1st. With all the headlines in the economy as well as the spreading screwworm, now at 12 confirmed cases in the US, and the recent announcement of JBS shuttering its Pennsylvania packing plant, the cattle market has been extremely resilient.

We have the cash market to thank that surged until late in the day on Friday. We saw light fed cattle cash trade last week as well as this week until Friday. Starting at $254 in Kansas and Nebraska, the trade accelerated quickly hitting $256, then $258 and reaching $260 in Kansas, Oklahoma, Texas and Nebraska. In combination with a bullish Cattle-on-Feed report on Thursday after the market close, I have high hopes for bullish market movements next week that could stay strong through the end of the month if summer demand supports boxed beef prices.

USDA's Cattle-on-Feed report leaned bullish with June 1 on-feed at 102.1 percent, lower than the expected 102.5 percent, May Placements at 90.3 percent, lower than the expected 94.5 percent, although May Marketings did come in at 88.2 percent, lower than the expected 89.4 percent. While higher on-feed and placements were expected, perhaps the most important number for the market was the lower than expected placements. On-feed was above last year, but of course from a low base and so expected.

Optimism that the Iran conflict is over, at least for a few months, should keep crude oil as well as corn futures under pressure and support the equity markets that in-turn, often support the livestock complex. Could we be headed for a new high in the cattle market? We said it many times before only to fail when close, but we could see additional strength if the funds decide to continue buying this market after the recent break that dominated the month of May. Just don’t tell optimism and hope catch you flat-footed without some kind of protection in place as this market is more fast-paced than ever before.

Sidwell Strategies is the one-stop shop to protect cattle with futures, puts, LRP or a combination of all, which is probably the best strategy overall. If you’re ready to trade commodity markets, give me a call at (580) 232-2272 or stop by my office to get your account set up and discuss risk management and marketing solutions to pursue your objectives. Self-trading accounts are also available. It is never too late to start and there is no operation too small to get a risk management and marketing plan in place.

Wishing everyone a successful trading week! Let us know if you'd like to join our daily market price and commentary text messages to stay informed!

Brady Sidwell is a Series 3 Licensed Commodity Futures Broker and Principal of Sidwell Strategies. You’re your Trading Account with Sidwell Strategies at https://portal.stonex.com/prefill/index/BradySidwellU52F112P. Contact us at (580) 232-2272 or at trade@sidwellstrategies.com.

Futures and Options trading involves the risk of loss and may not be suitable for all investors. Review full disclaimer at https://www.sidwellstrategies.com/fccp-disclaimer-21951.

/A%20close-up%20of%20a%20SpaceX%20sign%20by%20Sundry%20Photography%20via%20Adobe%20Stock.jpeg)

/AI%20(artificial%20intelligence)/AI%20chip%20by%203Dsss%20via%20Shutterstock.jpg)