/MGM%20Resorts%20International%20hotel%20by-%20atosan%20via%20iStock.jpg)

Billionaire media mogul Barry Diller has made a bold move that could reshape one of the biggest names in the casino industry. Through his company, People (PPLI), Diller has offered to buy the shares of MGM Resorts International (MGM) that he does not already own, valuing the casino giant at roughly $18 billion, including debt. The deal looks pretty straightforward, as Diller believes MGM is worth more than the market currently recognizes.

But for investors, the crucial question now is what happens if the deal goes through and what if it doesn’t.

What Exactly Is Barry Diller Offering?

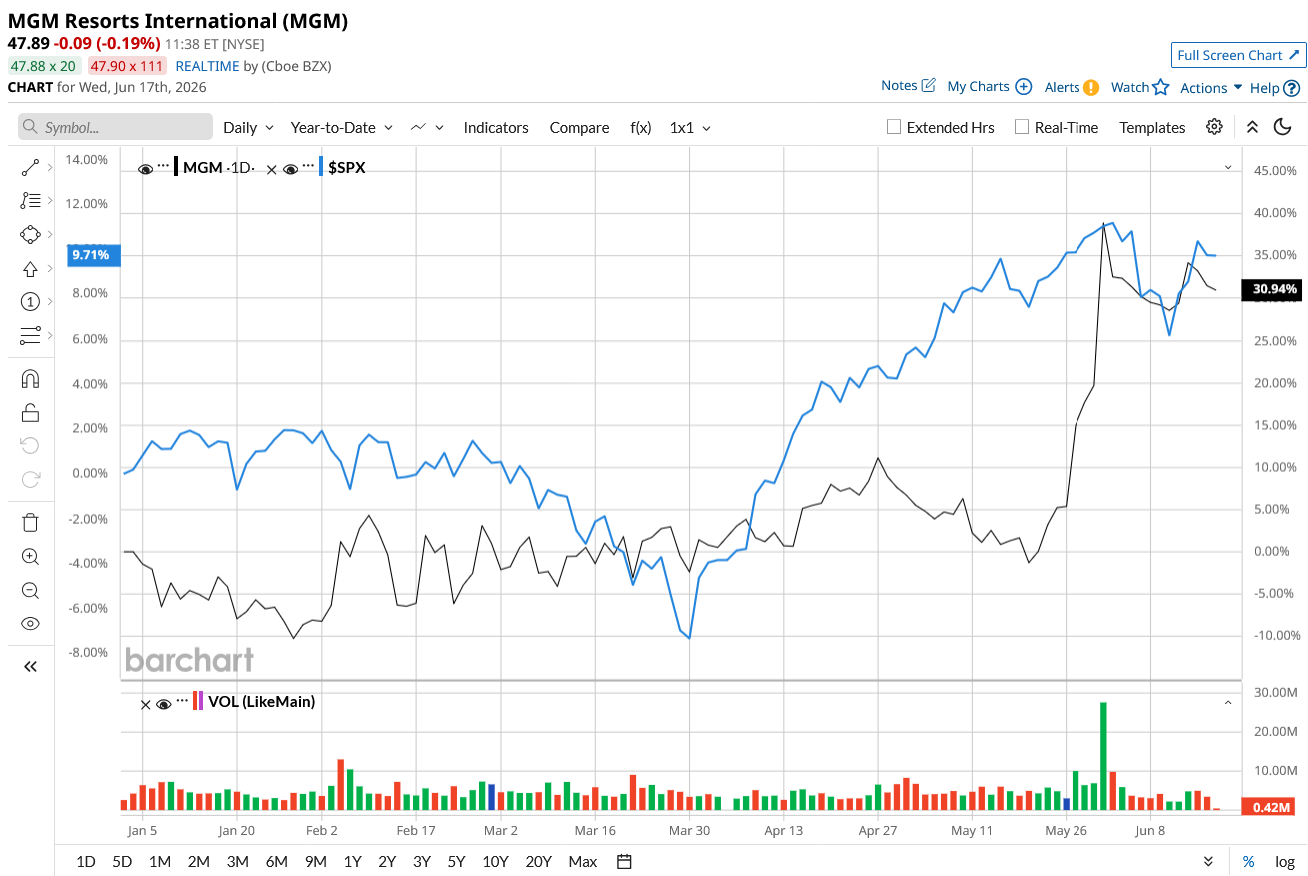

Diller, through this company, People, already owns roughly 26.1% of MGM. Now, Diller has proposed paying $48.30 per share in cash for the remaining shares he does not own. If this deal finalizes, MGM would become a private company controlled by People and will cease trading on the stock market. The offer represented a premium over MGM's share price prior to the announcement. Investors reacted to the news and the stock has climbed 30% year-to-date (YTD), outperforming the broader market.

MGM owns some of the most recognizable casino resorts in Las Vegas, including Bellagio, MGM Grand, Aria, Mandalay Bay, and several other major properties. The company owns a large chunk of the Las Vegas Strip, giving it assets that would be nearly impossible to recreate today. Additionally, it has a growing exposure to digital gambling through BetMGM, one of the largest online sports betting platforms in the U.S. Diller believes the market doesn’t value MGM’s assets and its long-term earnings potential and it could be worth more as a private company.

What Happens If the Deal Goes Through?

Currently, MGM’s board is reviewing the offer. This is a non-binding proposal, meaning neither side is legally obligated to complete the transaction at this stage. If the deal is approved, investors would receive cash for their MGM shares at the agreed price and not the current value of the shares. So, investors have a clear exit opportunity by cashing out at the premium.

Talking about the deal, recently, Stifel analyst Steven Wieczynski stated that Diller's $48.30 per share offer undervalues MGM and that the board could push for a higher bid. Currently, MGM shares are trading above the bid price at $48.62 as of writing, which the analyst believes is because investors think MGM is worth more than Diller's initial proposal. Some investors may even see Diller's bid itself as validation that MGM is a great stock. After all, billionaires do not usually offer $18 billion for companies they consider unworthy.

What Happens If the Deal Falls Apart?

Now, what happens if MGM’s board rejects the offer? Investors planning to cash out will lose out on the acquisition premium. Instead, they will have to just rely on MGM’s underlying business fundamentals. The stock will once again be valued based on its casino operations, hotel performance, digital betting growth, earnings, and debt levels rather than on acquisition speculation.

Let’s take a closer look at these numbers.

In the first quarter, MGM reported revenue growth of more than 4%, while Las Vegas, which is MGM's most important market, saw revenue increase year-over-year (YoY) for the first time in six quarters. Regional casino operations posted 2% revenue growth, while MGM China delivered 9% revenue growth and maintained its 15.4% market share in the quarter. The digital business, BetMGM's North American operations, grew revenue by 6% and adjusted EBITDA by 11%, while MGM Digital reported a striking 43% increase in revenue. While the revenue numbers are impressive, it hasn’t translated to significant bottom-line growth. Adjusted earnings declined 29% to $0.49 per share in Q1.

The balance sheet is another source of concern. MGM's debt-to-equity ratio currently stands at 1.93, meaning the company relies heavily on debt to fund its operations. For a cyclical business tied to travel, tourism, and consumer spending, this level of leverage can become a meaningful risk if economic conditions weaken.

Wall Street's earnings forecasts add another layer of caution. Analysts project earnings per share to decline by roughly 40% in 2026 before rebounding about 20% in 2027. So, if the deal falls apart, investors will have to decide if MGM stock is attractive enough with modest revenue growth, declining near-term earnings, and a relatively leveraged balance sheet.

What Should MGM Investors Watch Next?

Investors should watch out for MGM’s response to the proposal. Eventually, the board may accept or reject the offer, negotiate a higher price, or seek competitive bids from other buyers. Any of these scenarios will have a short-term impact on the stock price.

To summarize, MGM owns valuable casino assets and has promising exposure to online betting through BetMGM. However, I believe investors must balance those strengths against the company's substantial debt burden and relatively modest long-term growth profile before deciding if MGM stock is worth holding onto in case the deal falls apart. MGM has not announced a timeline for reviewing Barry Diller's proposal, so it could take a while before any decision is made.

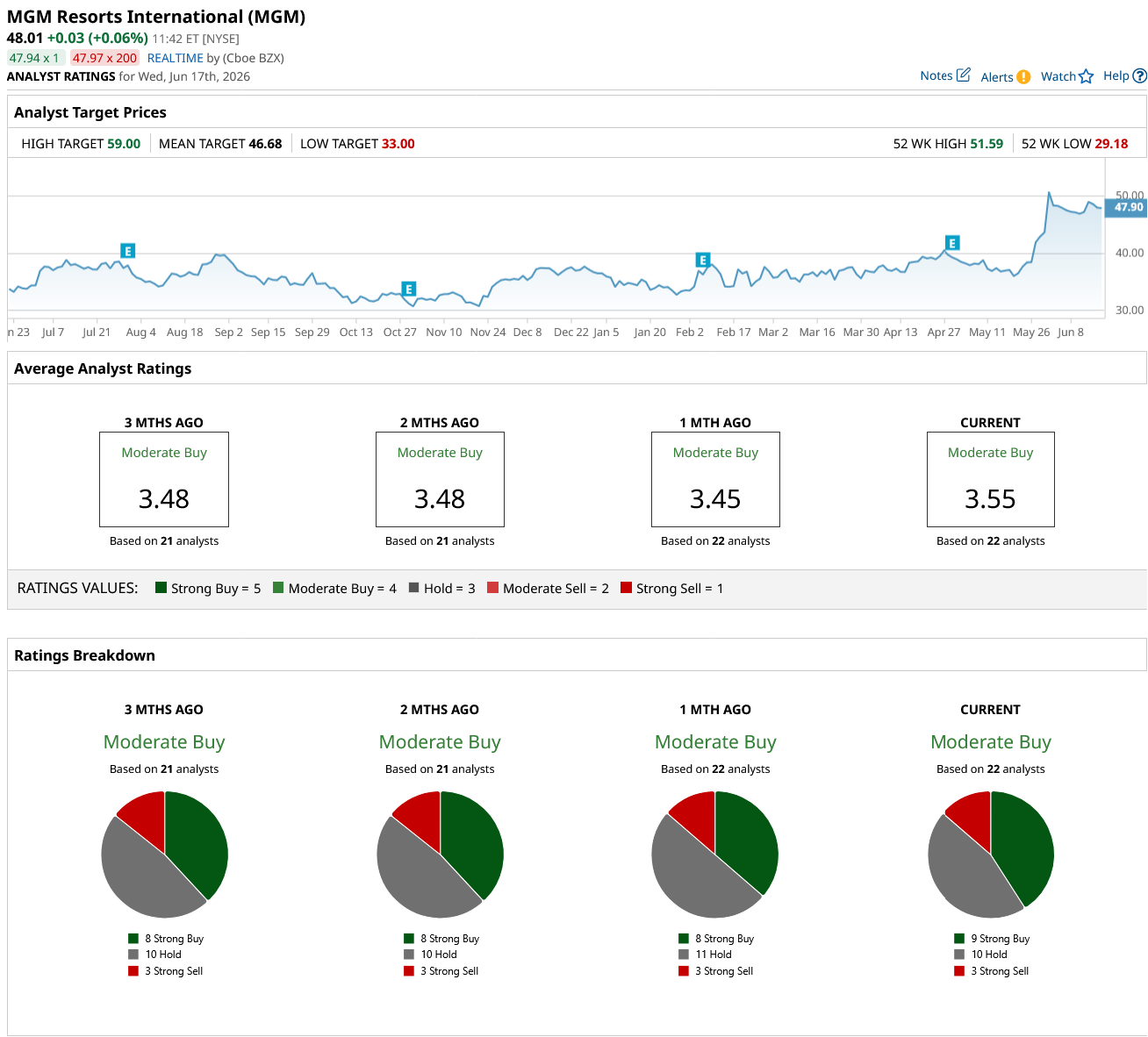

On Wall Street, MGM stock is a consensus “Moderate Buy.” Of the 22 analysts covering the stock, nine rate it as a "Strong Buy," 10 recommend a "Hold," and three analysts rate it a “Strong Sell.” Its high price estimate currently sits at $46.68.

On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20close-up%20of%20a%20SpaceX%20sign%20by%20Sundry%20Photography%20via%20Adobe%20Stock.jpeg)

/AI%20(artificial%20intelligence)/AI%20chip%20by%203Dsss%20via%20Shutterstock.jpg)