Sometimes, the most interesting stocks are the ones investors don't ever think of. That is especially true in a market where many chase the faster-growing names and overlook slower, familiar businesses. When a stock has struggled, growth has cooled, and Wall Street is cautious, it is easy to move on. But if the company still owns brands trusted by millions and keeps selling them over and over again, the story may be worth another look.

That is what makes Clorox such a compelling case. It is not the market’s favorite stock right now, but its trusted brands, high dividend profile, and beaten-down share price make it a rare “5% Dividend King” that income-focused investors may want to revisit.

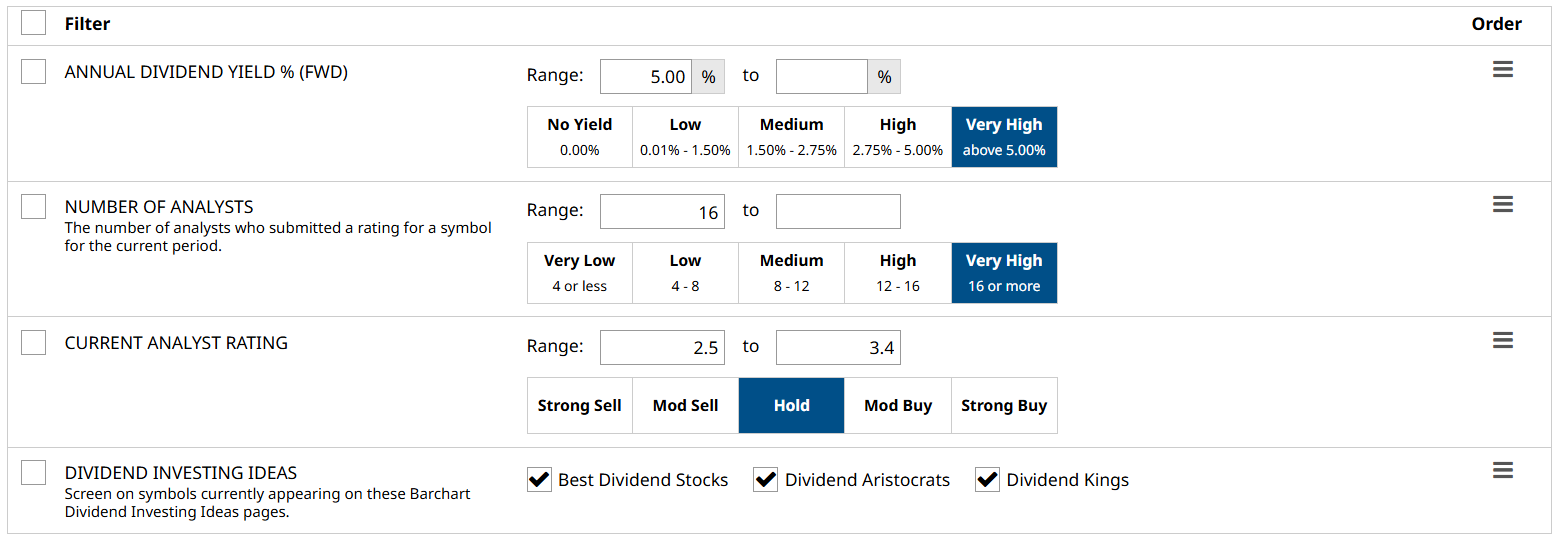

How I found the stock

Using Barchart’s Stock Screener, I selected the following filters to get my list:

- Annual Dividend Yield % (FWD): Very high. I am looking for companies with a yield of 5% or higher.

- Number of Analysts: 16 or more. High analyst coverage can provide stronger confidence in the consensus rating.

- Current Analyst Rating: I’m not looking for the market’s favorite stocks here, but rather for high-yield companies that could be overlooked and worth considering.

- Dividend Investing Ideas: Best Dividend Stocks, Dividend Aristocrats, Dividend Kings.

I set these filters and ran the screen, and only one company stood out.

So let’s get into it.

Clorox (CLX)

Clorox is a well-known consumer products company that sells cleaning, household, lifestyle, and international products. Aside from its flagship "Clorox" bleach, the company is also behind a wide range of products, including Pine-Sol, Glad, Hidden Valley, and more.

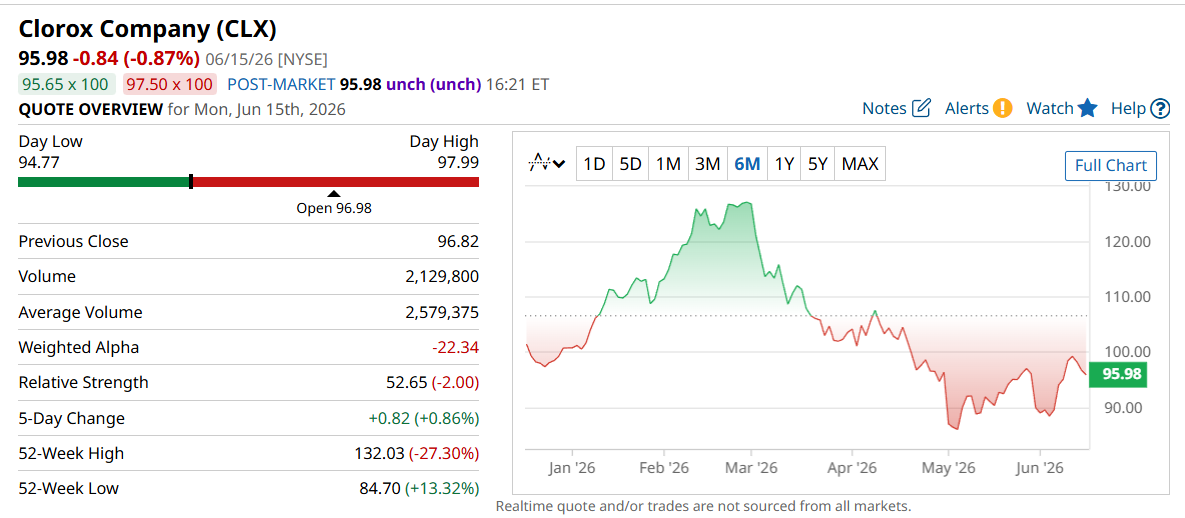

At the time of publication, the company has a market cap of $11.7 billion, and the stock has traded between $85 and $132 over the past 52 weeks, but now sits near the lower end of that range after falling just over 22% over the past year.

Clearly, some investors are wary of Clorox today - but to me, I see opportunity.

Why Clorox's repeat-purchase model makes it defensive

Clorox's business model is simple: It builds and sells trusted household brands through its four verticals, which are Health and Wellness, Household, Lifestyle, and International. The majority of its products are repeat purchases, which gives the company a stable presence in the market rather than exposure to big-ticket or one-time purchases.

But that does not exempt the company from pressure as higher costs, weaker demand, and market headwinds can still affect sales and margins. The risks remain, but at its core, Clorox maintains a strong foothold in products people use regularly, which is why it has long been viewed as a relatively defensive business.

Clorox's numbers tell a mixed story

The question now is: Does that “foothold” translate to the company’s latest quarterly reported number?

| Metric | Figure |

| Sales | $1.67 billion (0%) |

| Net Income | $187 million (+1%) |

| Operating Cash Flow (YTD) | $282 million (-59%) |

| Forward P/E | 17.53x (Consumer Staples Avg: 18.74x) |

Clorox did not have the strongest performance, but it is holding steady. Its sales remained unchanged YOY at $1.67 billion, while net income was up 1% YOY to $187 million.

The weaker point was cash flow. Specifically, year-to-date net cash provided by operations fell 59% year over year to $282 million. This decline was partly tied to a payment related to the termination of the Glad joint venture agreement, so it may not fully reflect the company’s normal cash generation.

In terms of valuation, Clorox trades at a forward price-to-earnings (P/E) ratio of 17.53x, compared with the consumer staples average of 18.74x. The P/E ratio tells us how much the market is willing to pay for each dollar of a company’s earnings. Trading below the sector average suggests the stock is undervalued, though investors should also consider its slower growth and recent business pressures when making that distinction.

Clorox's 5% yield is the real draw

Clorox pays a forward annual dividend of $4.96, translating to a yield of just over 5%, which is incredibly rare for a Dividend King, a company that has increased their dividends for at least 50 straight years.

However, that 5% yield comes with a 72% payout ratio, which means the company uses 72% of its income to pay out to shareholders. From a purely income perspective, that seems like a good deal, though it means the company has only 28% of its income left to invest in itself, which could slow future plans to grow the dividend. Still, 5% is 5%.

What could drive Clorox stock higher, or derail it

Its recent figures suggest that the company has been stagnant over the past year, but that trend might change.

One of the biggest potential drivers for Clorox is its GOJO acquisition, which brings Purell into its portfolio. If integrated well, Purell could strengthen Clorox’s position in hand hygiene and professional cleaning.

The risk is that Clorox still needs to prove it can return to growth. If sales remain flat, costs remain high, or margins remain under pressure, investors may continue to treat the stock with caution despite its dividend and lower valuation.

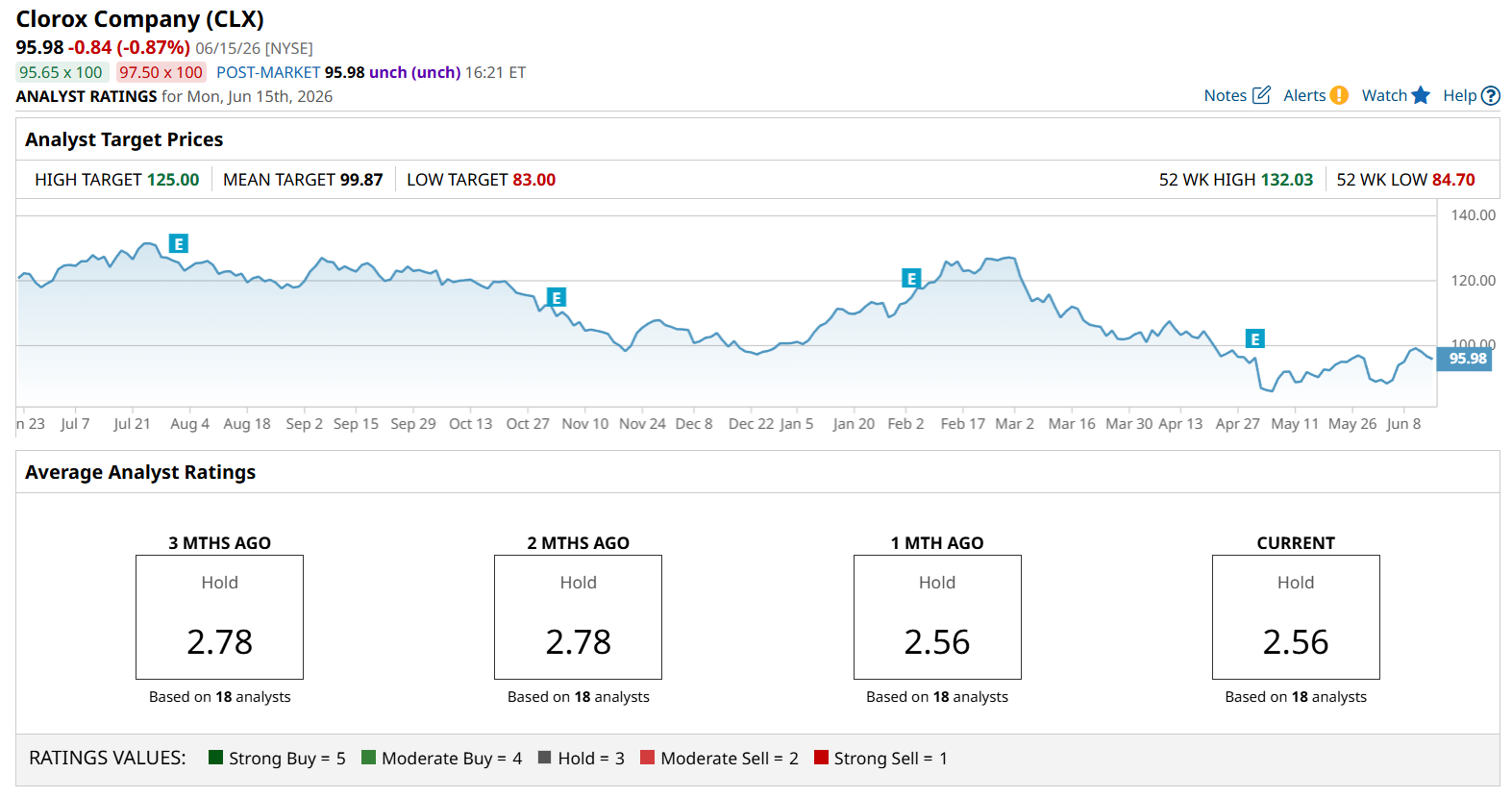

Where Wall Street stands on CLX stock

That risk is evident in Wall Street analysts, who take a cautious stance, with a consensus of 18 analysts rating the stock a “Hold.” Meanwhile, its target prices suggest there's as much as 30% upside if Clorox’s turnaround plays out as expected.

Final thoughts

Clorox is not a flashy AI stock, but its dividend record stands out. A 5% yield is attractive on its own, but a 5% yield from a company that has raised its dividend for generations is much harder to ignore. For dividend-growth investors, I see Clorox as a buy. The company still needs to return to growth, but its resilient brand portfolio, Dividend King status, and reliable dividend history make it a compelling income stock at current levels.

On the date of publication, Rick Orford did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Autodesk%20Inc_%20Portland%20office-by%20hapabapa%20via%20iStock.jpg)

/Alphabet%20(Google)%20Image%20by%20Markus%20Mainka%20via%20Shutterstock.jpg)