/Meta%20by%20creativeneko%20via%20Shutterstock.jpg)

Meta Platforms (META) has had a disappointing start to 2026. The social media giant's stock is down 10% year-to-date (YTD) and now trades roughly 25% below its 52-week high. The decline reflects investors’ concern around Meta's aggressive spending on artificial intelligence (AI) infrastructure and uncertainty about when those investments will begin generating meaningful returns.

The company recently raised its 2026 capital expenditure forecast to between $125 billion and $145 billion, up from its previous guidance of $115 billion to $135 billion. Management cited higher component costs and investments to support future AI capacity.

These massive outlays have fueled concerns that profit margins could come under pressure and raised questions about how Meta plans to finance its ambitious AI expansion.

Despite those concerns, the recent pullback has made Meta's valuation hard to ignore. Meanwhile, the company's core advertising business remains strong, and high-margin subscription revenue continues to grow at a healthy pace.

Meta’s Ad and Subscription Revenue Are Soaring

While Meta Platforms’ stock has lagged the broader market this year, the company's underlying business is firing on all cylinders. Meta's first-quarter results highlight stronger advertising revenue and solid momentum in its high-margin subscription offering.

Meta's Family of Apps segment generated $55.9 billion in revenue in the first quarter, up 33% year-over-year (YoY). Advertising accounted for $55 billion of that total, also increasing 33%.

The strong performance was driven by both higher user engagement and improved monetization. Ad impressions across Meta’s platforms increased 19%, while the average price per ad rose 12%. Management credited the pricing gains to improved ad performance, a healthier advertising market, and favorable foreign-exchange conditions.

User engagement across Meta’s ecosystem continued to strengthen. Both Instagram and Facebook reached record levels of video consumption during the quarter. On Instagram, enhancements to recommendation algorithms increased time spent watching Reels by 10%, while Facebook’s total video watch time grew by more than 8% globally.

WhatsApp also maintained strong momentum, giving Meta another platform with significant monetization potential.

One of the most underappreciated parts of Meta's quarter was the performance of non-advertising revenue. Family of Apps' other revenue increased 74% YoY to $885 million. Growth was primarily driven by WhatsApp paid messaging and subscription products.

Although this segment remains small compared to advertising, it is strategically important. These revenue streams tend to carry attractive margins and reduce Meta's dependence on advertising alone. As Meta ramps up investment in AI infrastructure, these higher-margin businesses could help offset rising capital expenditures.

Meta Expands Monetization via AI and Commerce

While Meta continues to boost engagement across its platforms, it is focused on turning that engagement into revenue. The company is using AI to improve ad performance, deliver better results for advertisers, and unlock new monetization opportunities.

Meta is refining how and where ads appear across its ecosystem while expanding advertising inventory on newer platforms such as Threads and WhatsApp Status. At the same time, it is rolling out AI-powered tools that help businesses get more value from their advertising budgets.

One notable example is Meta's Value Optimization suite. Adoption has grown rapidly, with management reporting that the product now generates an annual revenue run rate of more than $20 billion, more than double its level a year ago. This strong growth indicates that Meta's investments in AI are delivering meaningful financial benefits.

Meta is also seeing momentum in its commerce ecosystem, with the Partnership Ads product becoming a major growth driver. The product is now generating an annualized revenue run rate of over $10 billion, more than twice the level reported a year earlier.

Meta’s Valuation Looks Compelling

While Meta is expected to deliver solid revenue growth, earnings may remain under pressure in the near term. Wall Street analysts currently forecast earnings of $29.35 per share this year, representing a 1.2% YoY decline.

However, the outlook improves significantly beyond 2026. Analysts expect Meta's earnings growth to reaccelerate in 2027, with EPS projected to rise 19.3% YoY as investments in AI begin to generate stronger returns and subscription revenues expand.

Despite this favorable long-term outlook, Meta shares trade at 19.4 times forward earnings following the recent pullback. That valuation appears reasonable considering Meta’s solid growth potential.

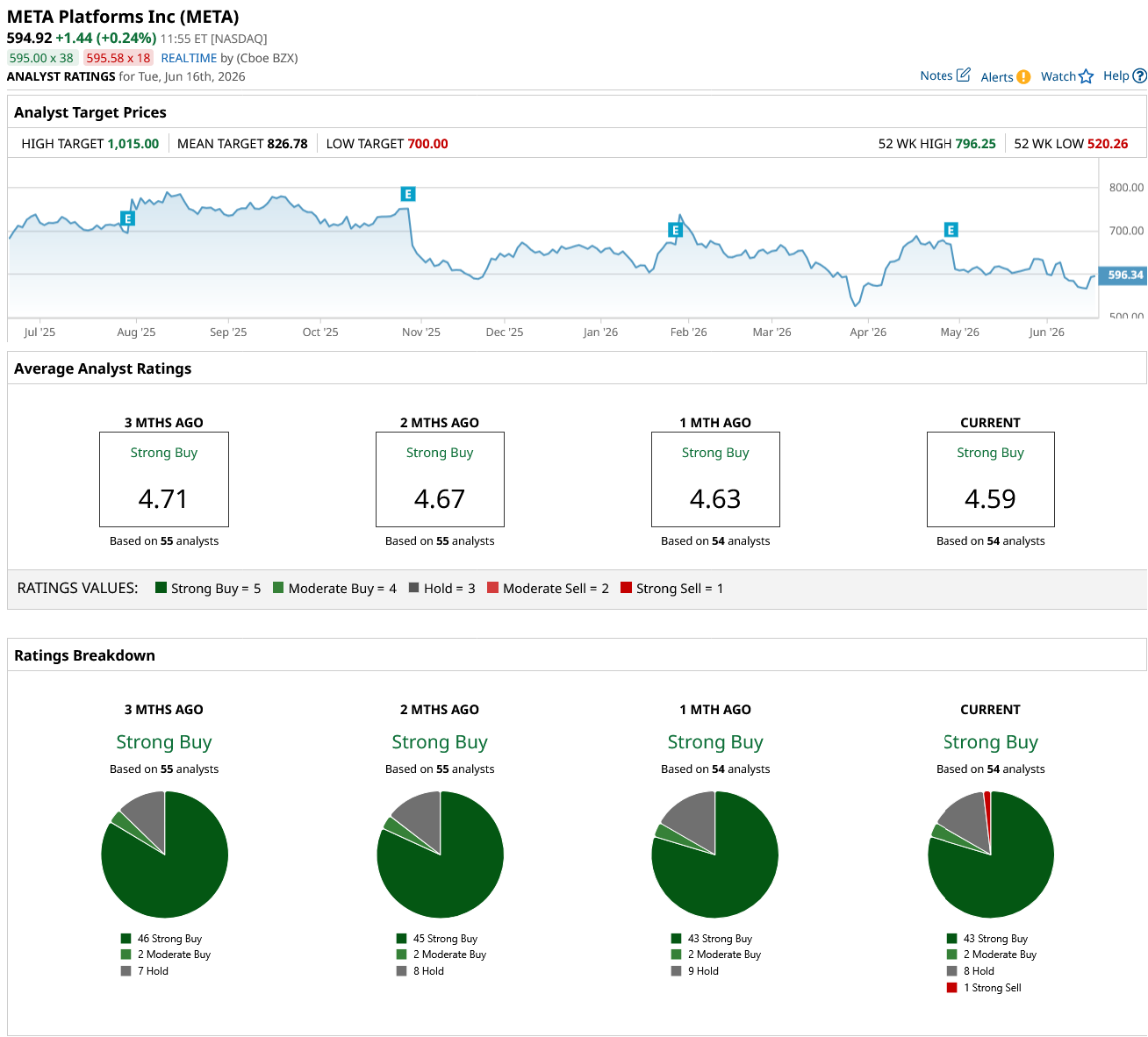

Analysts currently maintain a "Strong Buy" consensus rating on META stock, indicating the recent weakness as a buying opportunity.

On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20corporate%20sign%20for%20SK%20Hynix%20by%20Tada%20Images%20via%20Adobe%20Stock.jpeg)

/Netflix%20open%20on%20tablet%20by%20rswebsols%20via%20Pixabay.jpg)