Howdy market watchers!

We are days away from the primary elections around the country with early voting already underway. The political ads and unfortunate mudslinging have intensified as voting day nears, and I think we’re all ready for them to end. With greater polarization seemingly in all aspects of our lives in recent years, there has been a resurgence in political newcomers throwing their hat in the ring for elected positions at all levels of our society. This is healthy for a democracy, but also makes it increasingly clear of the wide-ranging perspectives and disagreements throughout our counties, cities, states and country, even within the same political party.

I continue to be fascinated by the lack of candidates with middle-of-the-road politics versus extreme left or right of center. The more people I speak with, the more desire there is for a blended candidate that can navigate many of the most diverging opinions that separate our country. In this age of emboldened criticism via social media platforms, that is of course easier said than done. However, we remain optimistic that the best candidates, reflecting the truth will emerge victoriously.

One of the most contentious topics emerging in this campaign, but will be more elevated in the general election is that of inflationary pressures from the war in Iran. It has now been 4 months since the US and Israeli pursuit in denuclearizing Iran. While much progress has been made in disarming and weakening the Iranian regime, the efforts have not neutralized the threat. In fact, we continue to negotiate with the same regime that is now more beleaguered and desperate.

The inconvenient truth is that they continue to wield power over global access to the critical energy components that traverse the Strait of Hormuz. Interestingly, oil prices have remained relatively tame despite the lack of peace progress amidst escalating threats that returned mid-week before easing by week’s end as President Trump yet again talks of a nearly complete agreement. Perhaps one of the reasons is that there is more ship activity through the Strait that is reported given that ships are turning off transponders in order to avoid detection.

Regardless of the White House rhetoric, the situation seems to still be very volatile with both Iran and Israel commenting that no agreements nor language had been settled. Without regime change, I really find it hard to believe that any “deal” will be a good deal for the US, Israel or the world unless and until the current regime in Iran is overthrown. The impact of uncertainty on the market is visible through its volatility, which is wearing, but very tradeable. Suffice it to say, the war premium is slowly coming out of various commodities. Late on Friday, both the Trump Administration and Iranian Regime were saying that the terms of the MOU were close with a potential signing next week in Europe. I do think President Trump would like to celebrate America's 250th birthday on July 4th claiming victory “over” Iran and so consider that timeline at least for some kind of agreement.

The historic SpaceX IPO on the Nasdaq on Friday created the first trillionaire with Elon Musk’s net worth surging with his ownership in what is the largest public offering in history. There are more IPOs coming in the AI and technology field, which will likely create more frothiness in equity markets. However, buyer beware as there feels to be increasing exuberance among retail investors that this market is unstoppable and yet, new highs were made again this week.

The first FOMC meeting of newly appointed Federal Reserve Chairman Warsh begins on Wednesday with his first press conference beginning on Thursday after the interest rate announcement that day at 1 PM CDT. A pause in interest rate changes is widely expected, but with hints of increases to come later in the year. Such forecast can be seen in the strengthening US dollar index. This all depends on the progress of inflation largely driven by energy prices.

This week’s CPI and PPI reports for the month of May both showed price pressures increasing above expectations. The CPI came in at an annualized rate of 4.2 percent, the highest in three years. Excluding the volatile segments of food and energy, the “core” CPI was at 2.9 percent annualized, which was in line with expectations, shedding light on where inflationary pressures are coming from. The Producer Price Index (PPI) increased 1.1 percent month-over-month, and meaningfully above the 0.7 percent expected, the largest increase since March 2022. Core PPI, excluding food and energy, came in surprising below expectations at 0.4 percent versus the forecast 0.5 percent. The PPI on finished goods grew 2.6 percent month-over-month in May, up from 1.6 percent in April and the largest monthly increase since June 2022.

Again, the higher cost and uncertainty in energy prices compounds throughout the supply chain as a critical component of every step of the supply chain including consumption. While agriculture commodity prices have moved in the opposite direction to the downside, there is growing concern that higher priced fertilizers and fuel could begin to limit planting and fertility decisions and alter production plans altogether. Furthermore, the threat of an increasingly likely mega El Nino is swelling concerns of the potential impact on disruptions to the global food supply chain. Once these factors begin to emerge and evolve after current favorable weather are fully discounted, we could see some healthy moves across the grain and oilseed complex.

US corn conditions this week remained unchanged from last week at 67 percent Good-to-Excellent while an increase to 69 percent was expected, compared to 71 percent last year. Soybean conditions declined one percent from last week to 65 percent while a two percent increase to 68 percent was expected. Rains in the Midwest have been favorable, but there are some areas receiving too much rain.

Winter wheat conditions in the US declined another percentage point to 25 percent Good-to-Excellent while an increase to 27 percent was expected and compared to 54 percent last year. The US wheat harvest progressed rapidly this week with dryer weather finally cooperating to get wheat out of the field with more rain coming. The USDA called winter wheat harvest 11 percent completed as of last Sunday and we should see a significant jump to this week’s rating released on Monday at 3 PM CDT. Spring wheat conditions came in at 52 percent Good-to-Excellent, above expectations and above last week.

The USDA released its monthly WASDE and Crop Production reports on Thursday at 11 AM CDT. New crop US wheat ending stocks lowered to 744 million bushels, below average trade estimates of 761 million bushels. Old crop wheat stocks were also trimmed by 5 million bushels. New crop US corn ending stocks were higher than expected at 1.960 billion bushels versus 1.946 billion bushels. US soybean ending stocks were slightly lower than expected at 310 million bushels versus 312 million bushels expected.

US wheat production was lowered to 1.543 billion bushels versus 1.557 billion bushels expected. All winter wheat production in the US was revised down to 1.030 billion bushels versus 1.041 billion bushels expected and compared to the previous month of 1.048 billion bushels. HRW specifically reduced to 497 million bushels versus 508 million bushels expected and down from USDA's last month estimate of 515 million bushels.

Brazil corn production increased while soybeans were trimmed slightly. Argentine corn production was reduced slightly while soybean production was increased.

World wheat ending stocks were adjusted slightly higher than expected at 275.4 million metric tons versus 274.3 MMT. World corn ending stocks were increased to 281.2 MMT versus 278.5 MMT. World soybean ending stocks were lowered to 124.9 MMT versus 125.3 MMT expected, but slightly higher than last month's 124.8 MMT.

New recent lows were made in both corn, back to October 2025 lows, and soybean markets while wheat futures are trying desperately to put in bottoming action after the recent onslaught. Harvest pressure however may continue into next week with better support typically in late June to early July.

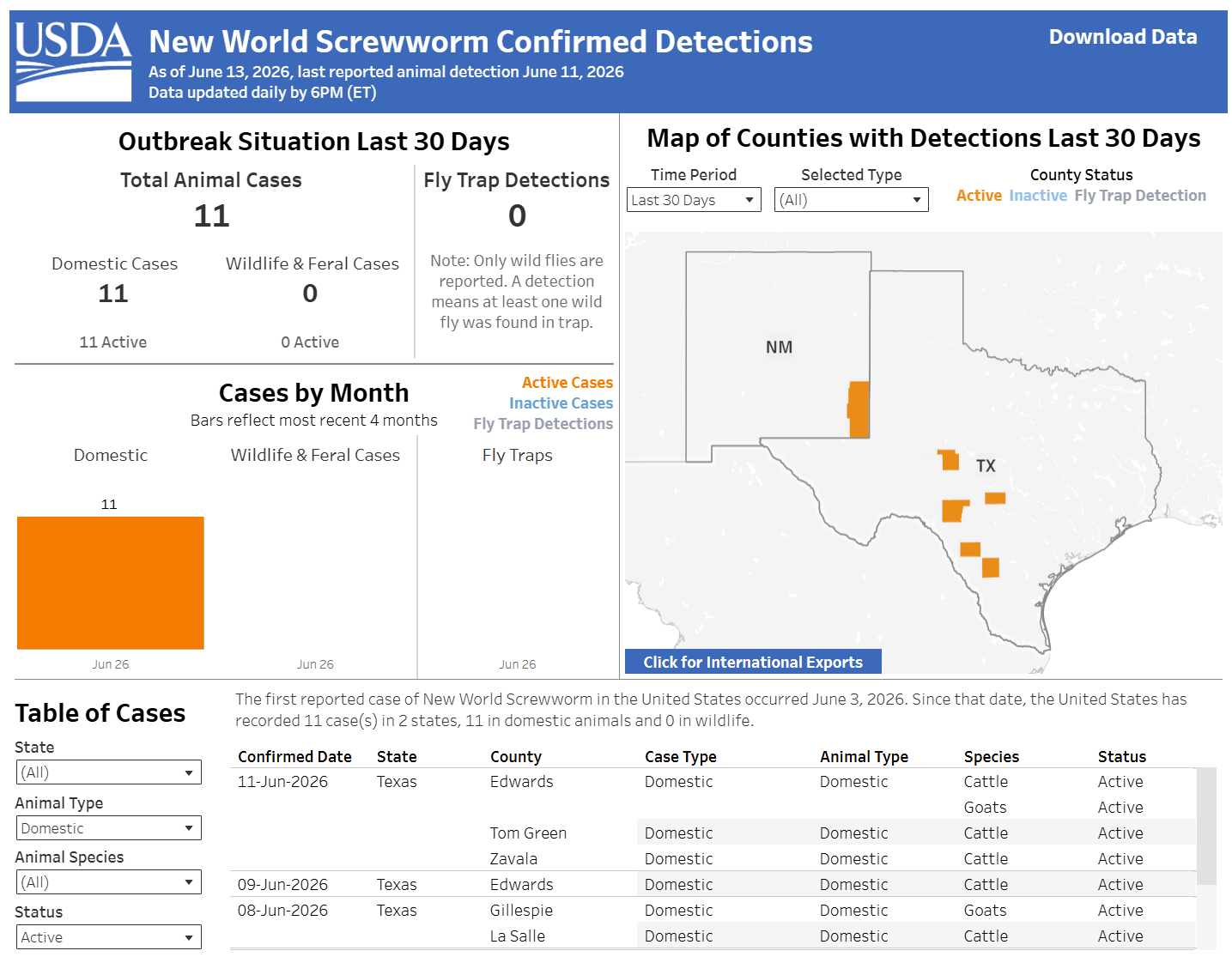

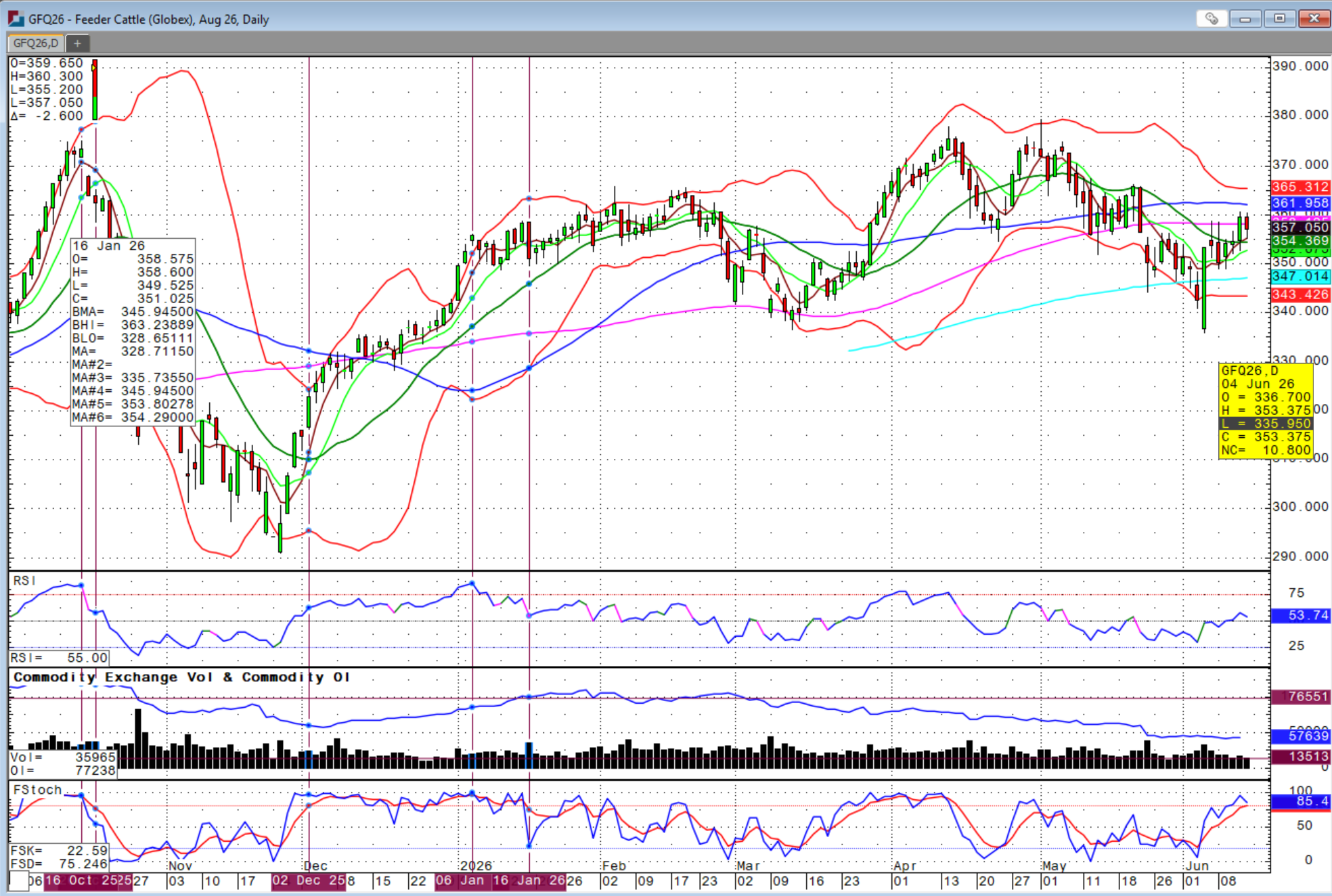

The cattle market has again become the bright spot across the agriculture complex in recent weeks despite the detections of multiple cases of New World Screw Worm in the US. As is often the case, the market has been conditioned of this potential threat in recent weeks and months, once the news was finally released, the market gapped lower only to bottom seconds later and has continued to surge higher in a choppy fashion ever since.

Fed cattle cash trade returned this week with highs reported late on Friday at $256 in Kansas and Western Nebraska and $255 in Texas. The downward sloping trendline in place since early May in feeder contracts that finally been closed above on Thursday as well as Friday despite the lower close to end the week. Both feeder and fed cattle futures had a wide trading range during Friday’s session, but managed to close off the lows at/above support levels.

With boxed beef prices climbing back with an upward seasonal trend through the July 4th holiday, I believe we could see firmer futures as well as cash markets for the next couple of weeks.

Additional NWSW cases that could result in greater restrictions on the movement of cattle between states could only serve to further limit supply and support prices. If consumers can continue to support higher fuel prices while buying beef, we could begin to see cattle prices move higher with ever cheaper corn. Time will tell.

Sidwell Strategies is the one-stop shop to protect cattle with futures, puts, LRP or a combination of all, which is probably the best strategy overall. If you’re ready to trade commodity markets, give me a call at (580) 232-2272 or stop by my office to get your account set up and discuss risk management and marketing solutions to pursue your objectives. Self-trading accounts are also available. It is never too late to start and there is no operation too small to get a risk management and marketing plan in place.

Wishing everyone a successful trading week! Let us know if you'd like to join our daily market price and commentary text messages to stay informed!

Brady Sidwell is a Series 3 Licensed Commodity Futures Broker and Principal of Sidwell Strategies. You’re your Trading Account with Sidwell Strategies at https://portal.stonex.com/prefill/index/BradySidwellU52F112P. Contact us at (580) 232-2272 or at trade@sidwellstrategies.com.

Futures and Options trading involves the risk of loss and may not be suitable for all investors. Review full disclaimer at https://www.sidwellstrategies.com/fccp-disclaimer-21951.

/Space/Planet%20earth%20with%20flying%20rocket%20by%20Sergey%20Mironov%20via%20Shutterstock.jpg)

/Alphabet%20(Google)%20Image%20by%20Markus%20Mainka%20via%20Shutterstock.jpg)

/Jen-Hsun%20Huan%20NVIDIA's%20Founder%2C%20President%20and%20CEO%20by%20jamesonwu1972%20via%20Shutterstock.jpg)

/Robinhood%20app%20on%20phone%20by%20Andrew%20Neel%20via%20Unsplash.jpg)