Wrapping up Q1 earnings, we look at the numbers and key takeaways for the shelf-stable food stocks, including J. M. Smucker (NYSE:SJM) and its peers.

As America industrialized and moved away from an agricultural economy, people faced more demands on their time. Packaged foods emerged as a solution offering convenience to the evolving American family, whether it be canned goods or snacks. Today, Americans seek brands that are high in quality, reliable, and reasonably priced. Furthermore, there's a growing emphasis on health-conscious and sustainable food options. Packaged food stocks are considered resilient investments. People always need to eat, so these companies can enjoy consistent demand as long as they stay on top of changing consumer preferences. The industry spans from multinational corporations to smaller specialized firms and is subject to food safety and labeling regulations.

The 17 shelf-stable food stocks we track reported a mixed Q1. As a group, revenues were in line with analysts’ consensus estimates while next quarter’s revenue guidance was 1.8% below.

Amidst this news, share prices of the companies have had a rough stretch. On average, they are down 5.5% since the latest earnings results.

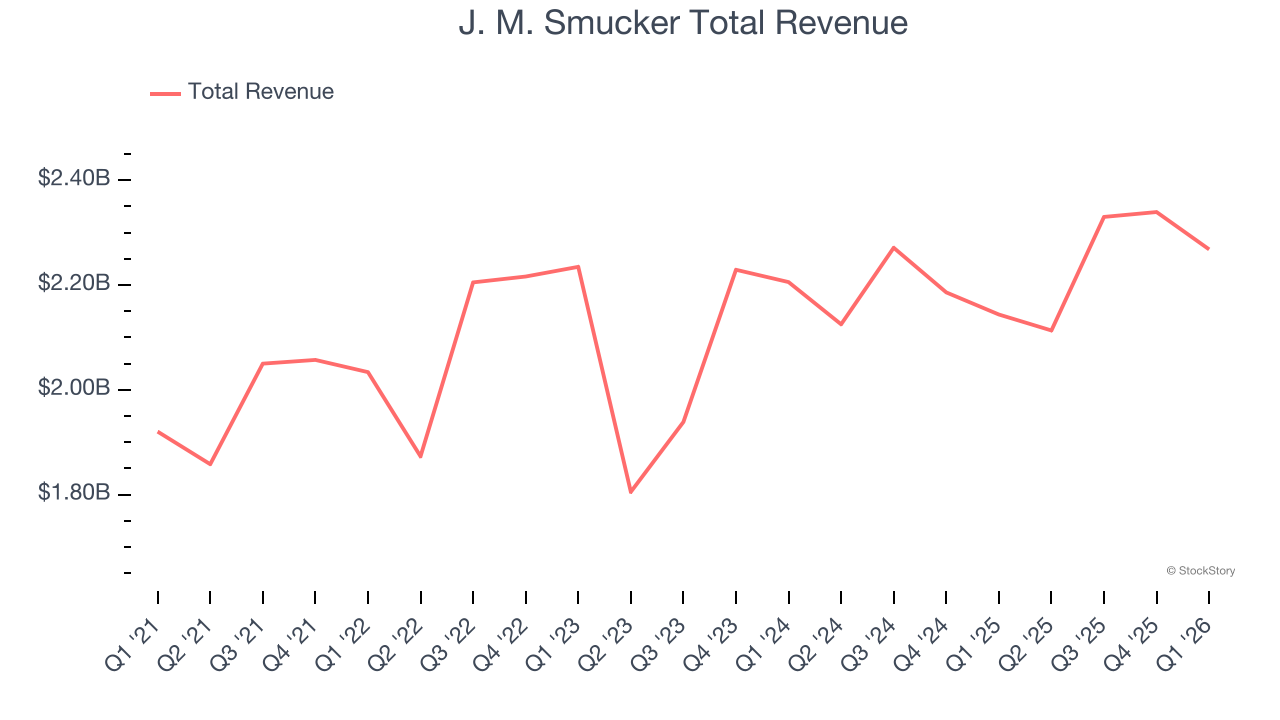

J. M. Smucker (NYSE:SJM)

Best known for its fruit jams and spreads, J.M Smucker (NYSE:SJM) is a packaged foods company whose products span from peanut butter and coffee to pet food.

J. M. Smucker reported revenues of $2.27 billion, up 5.8% year on year. This print was in line with analysts’ expectations, and overall, it was a satisfactory quarter for the company with a decent beat of analysts’ gross margin estimates.

"Our strong fourth quarter results demonstrate the continued strength of our focused strategy and portfolio enhancement efforts, which have transformed the Company over time," said Mark Smucker, Chief Executive Officer, President and Chair of the Board.

Interestingly, the stock is up 14.4% since reporting and currently trades at $116.42.

Is now the time to buy J. M. Smucker? Access our full analysis of the earnings results here, it’s free.

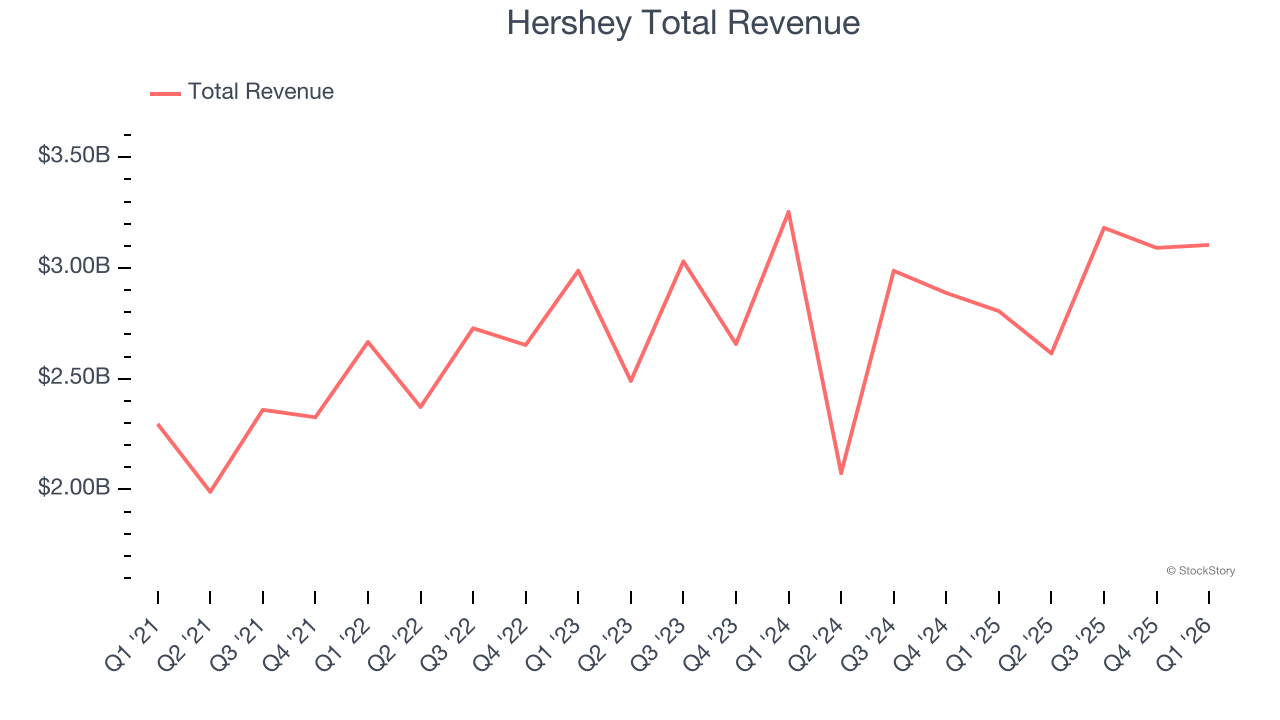

Best Q1: Hershey (NYSE:HSY)

Best known for its milk chocolate bar and Hershey's Kisses, Hershey (NYSE:HSY) is an iconic company known for its chocolate products.

Hershey reported revenues of $3.10 billion, up 10.6% year on year, outperforming analysts’ expectations by 2.4%. The business had a very strong quarter with an impressive beat of analysts’ EBITDA and organic revenue estimates.

Although it had a fine quarter compared to its peers, the market seems unhappy with the results as the stock is down 4.7% since reporting. It currently trades at $180.25.

Is now the time to buy Hershey? Access our full analysis of the earnings results here, it’s free.

Weakest Q1: BellRing Brands (NYSE:BRBR)

Spun out of Post Holdings in 2019, Bellring Brands (NYSE:BRBR) offers protein shakes, nutrition bars, and other products under the PowerBar, Premier Protein, and Dymatize brands.

BellRing Brands reported revenues of $598.7 million, up 1.8% year on year, falling short of analysts’ expectations by 1.7%. It was a disappointing quarter as it posted full-year EBITDA guidance missing analysts’ expectations.

As expected, the stock is down 49.6% since the results and currently trades at $8.75.

Read our full analysis of BellRing Brands’s results here.

The Marzetti Company (NASDAQ:MZTI)

Known for its frozen garlic bread and Parkerhouse rolls, The Marzetti Company (NASDAQ:MZTI) sells bread, dressing, and dips to the retail and food service channels.

The Marzetti Company reported revenues of $451.8 million, flat year on year. This print came in 2.6% below analysts’ expectations. Overall, it was a disappointing quarter as it also produced a significant miss of analysts’ EPS estimates and a miss of analysts’ EBITDA estimates.

The stock is down 12.1% since reporting and currently trades at $109.38.

Read our full, actionable report on The Marzetti Company here, it’s free.

Lamb Weston (NYSE:LW)

Best known for its Grown in Idaho brand, Lamb Weston (NYSE:LW) produces and distributes potato products such as frozen french fries and mashed potatoes.

Lamb Weston reported revenues of $1.56 billion, up 2.9% year on year. This result beat analysts’ expectations by 5.2%. Overall, it was a very strong quarter as it also logged an impressive beat of analysts’ organic revenue estimates.

Lamb Weston scored the biggest analyst estimate beat but had the weakest full-year guidance update among its peers. The stock is up 6% since reporting and currently trades at $44.80.

Read our full, actionable report on Lamb Weston here, it’s free.

Market Update

Late in 2025 into early 2026, there was hand-wringing around artificial intelligence. For software companies, the fear was that AI would erode pricing power and compress margins as new tools made it easier to replicate what once required expensive enterprise platforms. Crypto investors had their own version of the same anxiety: if AI agents could trade, allocate capital, and manage wallets autonomously, what exactly was the long-term value of today’s crypto infrastructure?

These concerns triggered a noticeable rotation away from these sectors and into safer havens. But markets rarely dwell on one narrative for long. Spring 2026 came, and the focus shifted abruptly from technological disruption to geopolitical risk. The US’ conflict with Iran became the dominant driver of market psychology, and when geopolitics takes center stage, the script changes quickly. Investors stop debating growth rates and start worrying about oil supply, inflation, and global stability.

Want to invest in winners with rock-solid fundamentals? Check out our Top 6 Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory’s analyst team — all seasoned professional investors — uses quantitative analysis and automation to deliver market-beating insights faster and with higher quality.

/Space/Planet%20earth%20with%20flying%20rocket%20by%20Sergey%20Mironov%20via%20Shutterstock.jpg)

/Alphabet%20(Google)%20Image%20by%20Markus%20Mainka%20via%20Shutterstock.jpg)

/Robinhood%20app%20on%20phone%20by%20Andrew%20Neel%20via%20Unsplash.jpg)