Tyson Foods currently trades at $58.73 per share and has shown little upside over the past six months, posting a middling return of 4.5%. The stock also fell short of the S&P 500’s 10.7% gain during that period.

Is now the time to buy Tyson Foods, or should you be careful about including it in your portfolio? Check out our in-depth research report to see what our analysts have to say, it’s free.

Why Do We Think Tyson Foods Will Underperform?

We’re sitting this one out for now. Here are three reasons why TSN doesn’t excite us, plus one stock we’d rather own.

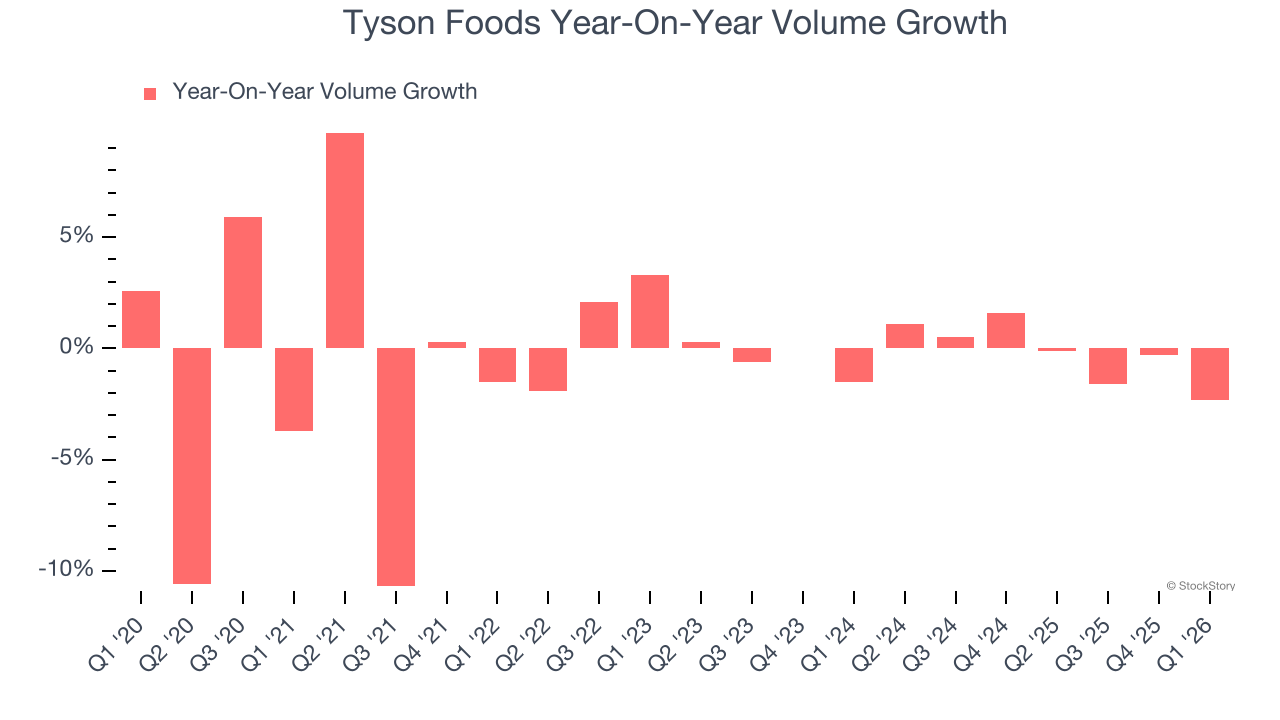

1. Sales Volumes Stall, Demand Waning

Revenue growth can be broken down into changes in price and volume (the number of units sold). While both are important, volume is the lifeblood of a successful staples business as there’s a ceiling to what consumers will pay for everyday goods; they can always trade down to non-branded products if the branded versions are too expensive.

Tyson Foods’s quarterly sales volumes have, on average, stayed about the same over the last two years. This stability is normal because the quantity demanded for consumer staples products typically doesn’t see much volatility.

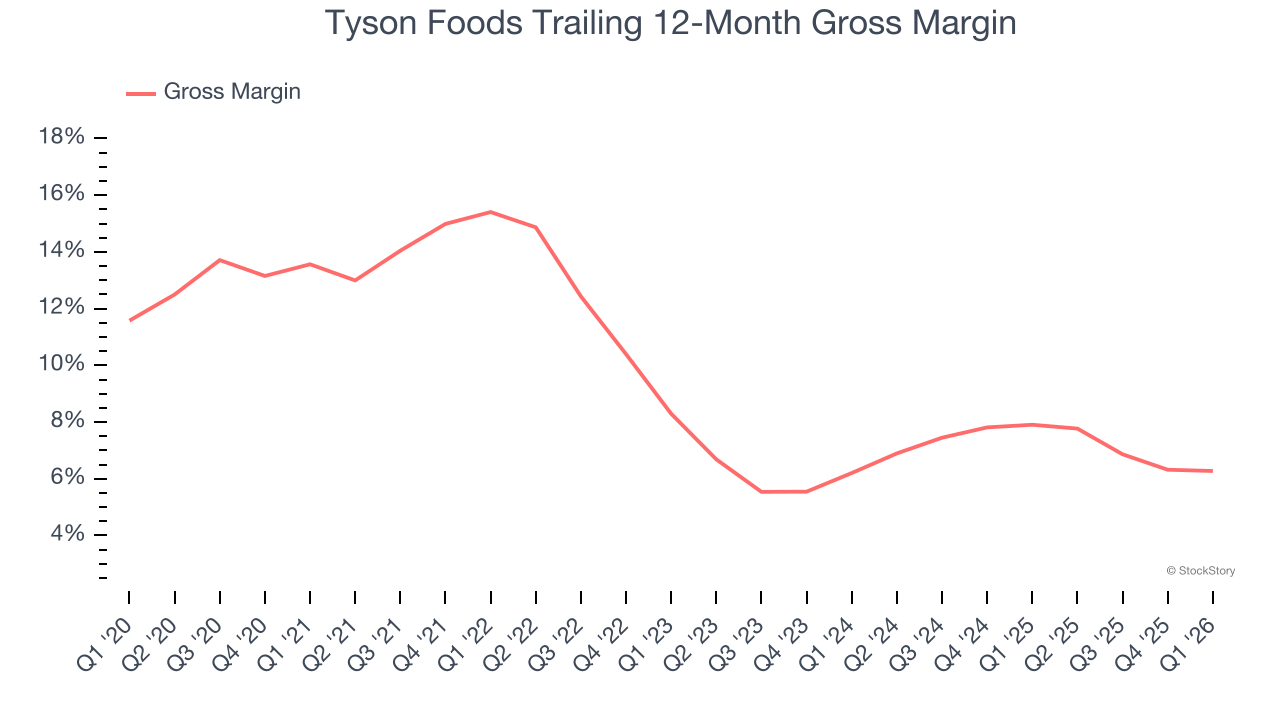

2. Low Gross Margin Reveals Weak Structural Profitability

At StockStory, we prefer high gross margin businesses because they indicate pricing power or differentiated products, giving the company a chance to generate higher operating profits.

Tyson Foods has bad unit economics for a consumer staples company, signaling it operates in a competitive market and lacks pricing power because its products can be substituted. As you can see below, it averaged a 7.1% gross margin over the last two years. Said differently, for every $100 in revenue, a chunky $92.92 went towards paying for raw materials, production of goods, transportation, and distribution.

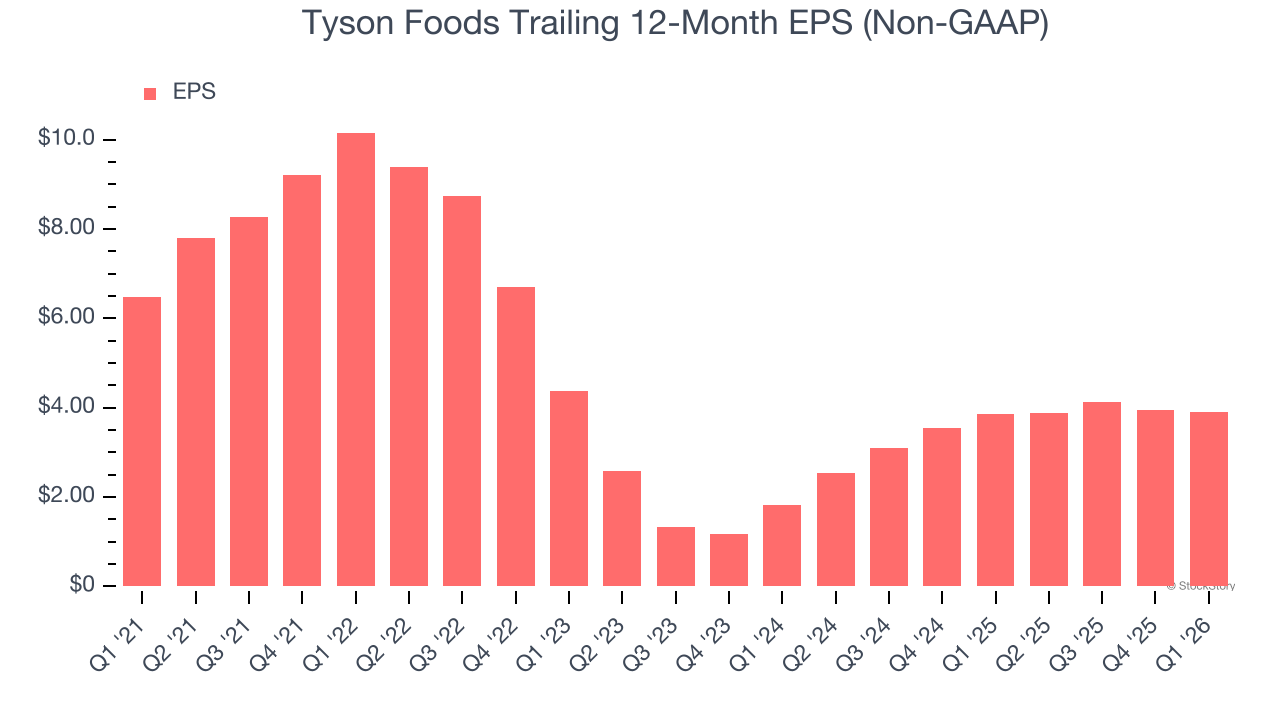

3. EPS Trending Down

We track the long-term change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

Sadly for Tyson Foods, its EPS declined by 3.8% annually over the last three years while its revenue grew by 1.3%. This tells us the company became less profitable on a per-share basis as it expanded.

Final Judgment

Tyson Foods falls short of our quality standards. With its shares trailing the market in recent months, the stock trades at 12.6× forward P/E (or $58.73 per share). This valuation multiple is fair, but we don’t have much confidence in the company. There are more exciting stocks to buy at the moment. Let us point you toward a dominant aerospace business that has perfected its M&A strategy.

Stocks We Would Buy Instead of Tyson Foods

ONE MORE THING: Top 6 Stocks for This Week. This market is separating quality stocks from expensive ones fast. AI is taking down whole sectors with no warning. In a rotation this fast, you need more than a list of good companies.

Our AI system flagged Palantir before it ran 1,662%. AppLovin before it ran 753%. Nvidia before it ran 1,178%. Each week it produces 6 new names that pass the same tests. Get Our Top 6 Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.

/An%20Intel%20sign%20out%20front%20of%20a%20corporate%20office%20by%20wolterke%20via%20Adobe%20Stock.jpeg)

/United%20Parcel%20Service%2C%20Inc_%20logo%20on%20truck-by%20100pk%20via%20iStock.jpg)

/A%20close-up%20of%20the%20SpaceX%20sign%20on%20a%20black%20building%20by%20IanDewarPhotography%20via%20Adobe%20Stock.jpeg)