/Technology%20by%20Alexandre%20Debieve%20via%20Unsplash-2.jpg)

Rumble Inc. (RUM) is a Longboat Key, Florida-based "Freedom-First" technology platform that is no stranger to controversy. The company operates a rapidly growing video sharing, live streaming, and cloud services ecosystem. Founded in 2013 by CEO Chris Pavlovski, Rumble has emerged as the leading alternative digital media platform and is now aggressively pivoting toward AI cloud infrastructure. The proposed combination with equally controversial Northern Data AG unites Rumble's video platform, advertising network, and cloud services with Northern Data's approximately 22,000 GPUs and nine data center facilities, positioning the combined entity at the intersection of digital media, AI compute, and cloud infrastructure.

Backed by nearly $1 billion in strategic investment from Tether, Rumble is transforming from a niche video platform into a diversified, AI-powered technology company with a significantly expanding total addressable market.

Rumble Stock Performance

RUM's 52-week range spans from a low of $4.62 to a high of $10.99, reflecting significant volatility driven by the Northern Data acquisition announcement, Tether partnership milestones, and shifting sentiment around the company's AI cloud pivot. The stock has underperformed significantly over its IPO lifetime, delivering an annualized return of approximately -4.5% since its February 2021 listing at $10.71.

Against the Nasdaq Composite's ($NASX) approximately 13% year-to-date (YTD) gain in 2026, RUM has done quite well at 24%. However, it has lagged the broader tech index significantly over the last 52 weeks, down 12% in that timeframe. Though the pending Northern Data closing, Tether advertising ramp, and Rumble Shorts monetization in H2 2026 represent meaningful re-rating catalysts that could sharply alter the trajectory over the long run.

Rumble Posts Mixed Results

Rumble reported Q1 2026 revenue of $25.5 million, up 7% year-over-year (YoY) from $23.7 million in Q1 2025, narrowly missing the analyst consensus estimate of approximately $34.83 million, while GAAP EPS came in at a loss of $0.12 per share, missing the forecast loss of $0.06. Despite the dual miss on revenue and EPS, the company's revenue beat the Zacks consensus estimate by 2.29%, with high marketing spend and non-cash acquisition-related charges being the primary drivers of the wider-than-expected net loss.

Rumble posted a net loss of $30.3 million in Q1 2026, compared to just $2.7 million in Q1 2025, primarily driven by non-cash items and costs tied to the Northern Data acquisition process. The cost of services declined 10% YoY to $27 million, while general and administrative expenses fell sharply by 37% to $10.4 million, though sales and marketing expenses surged 134% to $8.5 million, reflecting aggressive brand-building investment ahead of the combined entity's launch. The adjusted EBITDA loss for the quarter was $21 million.

The Northern Data acquisition is on track to close in mid-June 2026, with Northern Data shares to be delisted promptly thereafter. CEO Chris Pavlovski stated, "While we are disappointed with our financial results, we remain committed to our strategic initiatives, including the monetization of Rumble Shorts and expansion of our cloud services." The company plans to begin monetizing Rumble Shorts in H2 2026 and accelerate its Tether advertising commitment, which has already commenced scaling in Q2 2026.

Rumble Partners With Nvidia

Rumble shares surged more than 23% to an 11-month high after the company announced its largest customer commitment to date, a significant milestone in its ongoing pivot toward AI cloud infrastructure. According to an SEC filing, a third-party cloud customer has committed to purchasing dedicated GPU cloud capacity from Rumble, powered by Nvidia's (NVDA) next-generation Blackwell B300 systems.

The agreement represents a substantial and emerging new revenue stream for Rumble beyond its advertising business, with the contract also carrying provisions for increased value and extended duration based on market success, signaling strong confidence in Rumble's growing cloud capabilities and long-term AI infrastructure ambitions.

Should You Get Rumble?

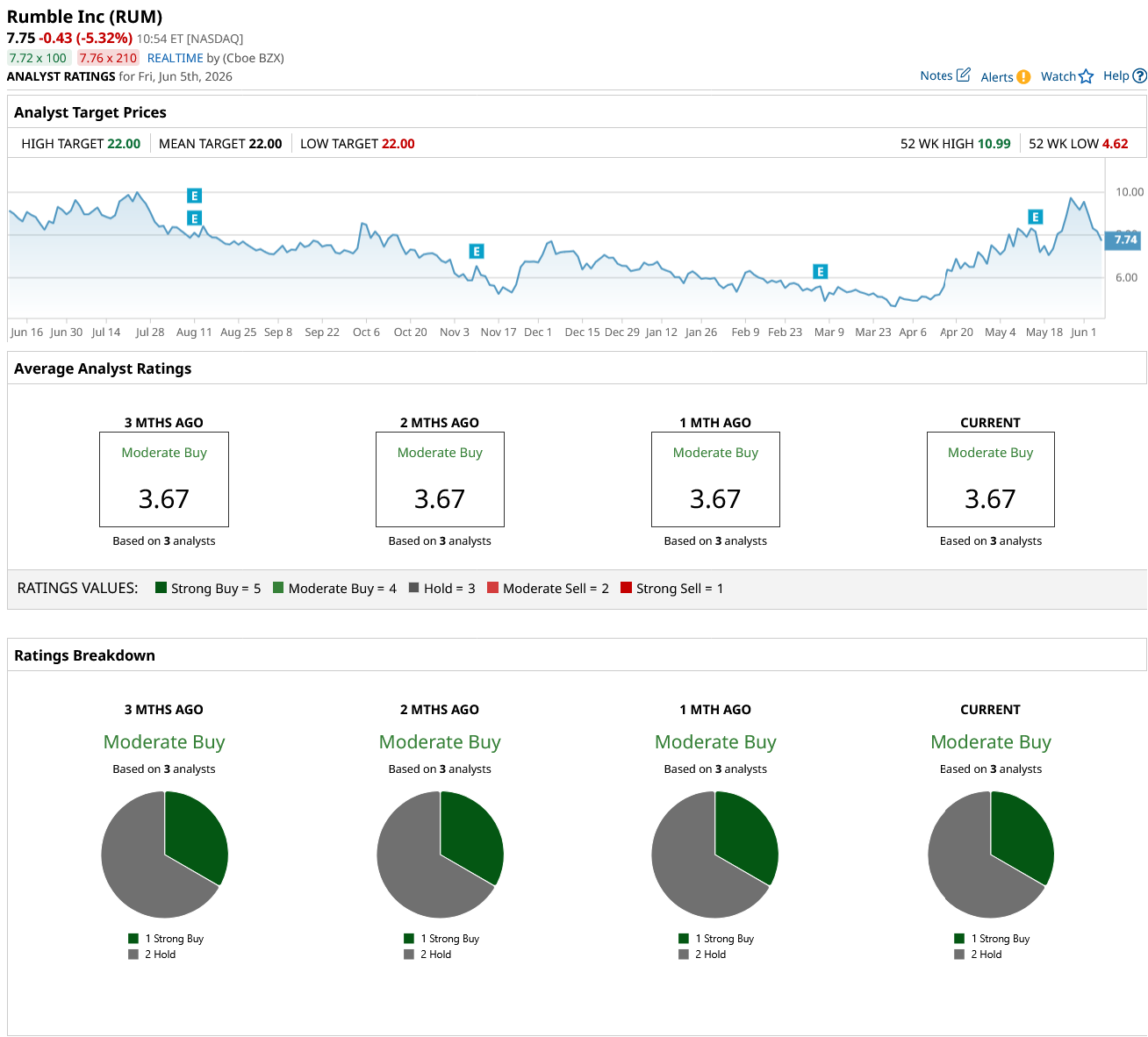

With Rumble's landmark Nvidia Blackwell B300-powered cloud contract marking its largest customer commitment to date, the company's AI infrastructure pivot is rapidly shifting from narrative to reality. Wall Street's consensus stands at "Moderate Buy" across three analyst ratings, comprising one "Strong Buy" and two "Hold," with a mean price target of $22, implying a staggering approximately 184% upside from current levels.

While the thin analyst coverage and pre-profitability status demand caution, the Northern Data acquisition closing, Tether advertising ramp, and now a landmark GPU cloud contract collectively make RUM one of the most asymmetric risk-reward opportunities in the small-cap AI space today.

On the date of publication, Ruchi Gupta did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/NVIDIA%20Corp%20video%20chip-by%20Antonio%20Bordunovi%20via%20iStock.jpg)

/Space/Rocket%20lift%20off%20by%20Alones%20via%20Shutterstock.jpg)

/A%20close-up%20of%20an%20AMD%20office%20by%20gehapromo%20via%20Adobe%20Stock.jpeg)