/Alphabet%20(Google)%20Image%20by%20Markus%20Mainka%20via%20Shutterstock.jpg)

The artificial intelligence (AI) boom is turning into one of the most expensive technology buildouts Wall Street has ever seen. From giant data centers packed with advanced chips to the massive computing power needed to train and run AI models, tech companies are pouring tens of billions of dollars into infrastructure. And if recent signals are any indication, that spending spree is far from over.

That reality came into sharper focus this week when Alphabet (GOOG) (GOOGL) found itself under pressure after unveiling for its financing plans to help fund its AI ambitions. The Google parent aims to raise about $84.75 billion. In a filing dated June 2, Alphabet announced plans to raise $18 billion through the sale of Class A and C shares and $16.75 billion from depositary shares, along with a $40 billion at-the-market (ATM) program that will allow the company to gradually sell shares beginning in Q3.

Investors have largely cheered AI investments so far, but seeing one of the world’s richest tech companies tap the equity market reminded Wall Street just how costly this race is becoming. The news weighed on Alphabet stock, as investors digested not only the dilution concerns but also the company’s eye-popping capital spending plans for this year and the next.

Yet buried beneath the market’s initial reaction was a notable vote of confidence. Berkshire Hathaway (BRK.A) (BRK.B), now led by Greg Abel, agreed to take a $10 billion stake through a private placement, deepening a bet that has quickly become one of the conglomerate’s largest stock holdings.

So while Alphabet's fundraising sparked fresh questions about the rising cost of AI, Berkshire’s growing commitment may be pointing investors toward a different story altogether.

About Alphabet Stock

Alphabet hardly needs an introduction in global technology circles. Headquartered in California and valued at $4.35 trillion by market cap, it’s one of Silicon Valley’s most influential forces. Far beyond Search, Alphabet has expanded into AI, cloud infrastructure, autonomous mobility through Waymo, and advanced research led by DeepMind. Its Gemini models reflect an ambition not just to join the AI race, but to define it.

Investors have rewarded that progress. Strong execution in AI, accelerating cloud growth, and confidence in Google’s long-term strategy have helped drive the stock higher, reinforcing Alphabet’s standing among the world's most valuable and closely watched companies.

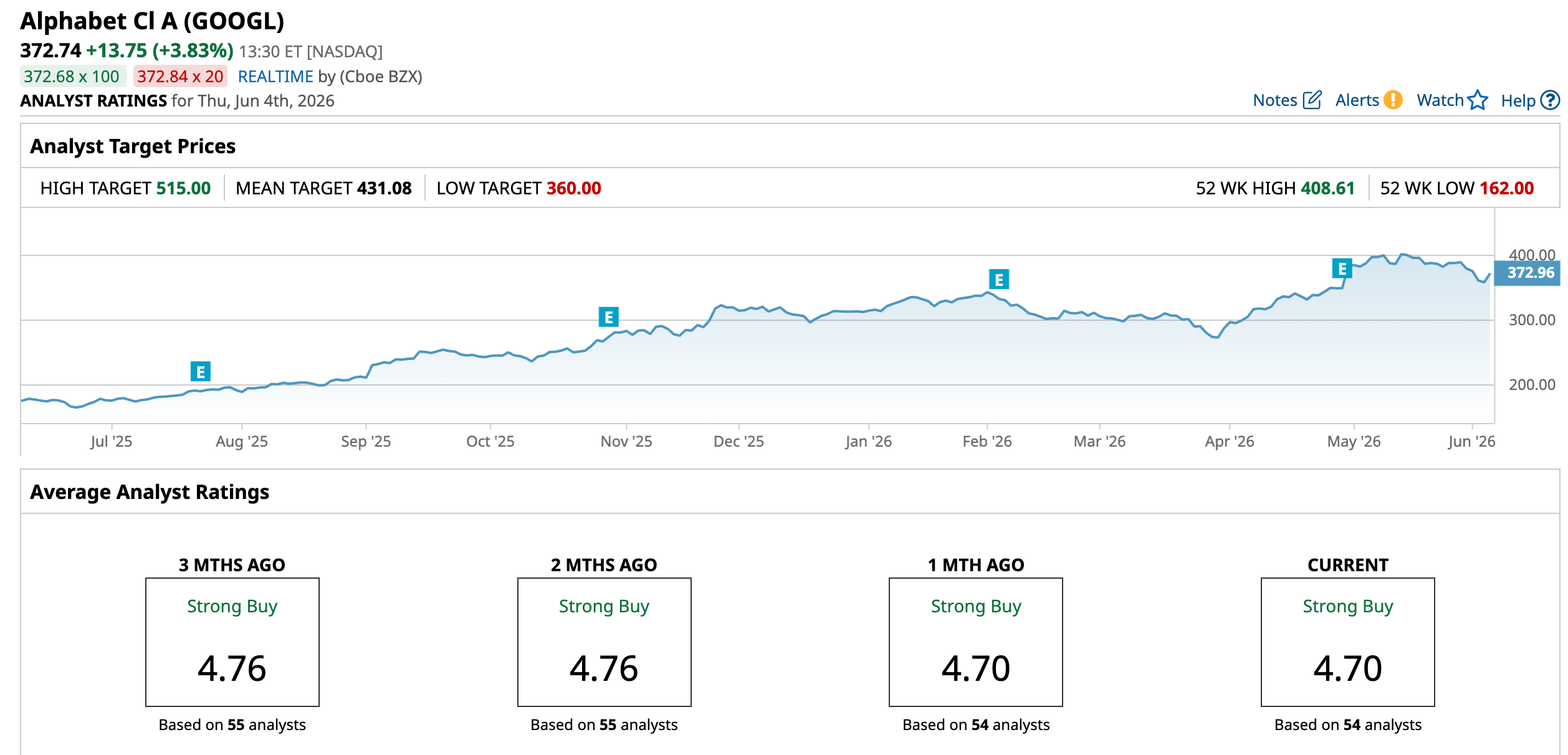

Shares of the Google parent have had quite a ride over the past year. The stock spent much of that period climbing steadily higher as investors embraced the company’s growing role in the AI boom. That optimism helped push shares to a 52-week high at $408.61 in May, as Wall Street cheered everything from Google’s AI-powered Search upgrades to the explosive growth coming out of Google Cloud.

The story has become a little more complicated in recent weeks. Shares have pulled back about 8.78% from their peak after the company unveiled plans for a massive equity raise to help fund its AI ambitions. For some investors, the announcement was a reminder that winning the AI race requires enormous amounts of capital along with great technology.

Still, even after the recent decline, GOOGL stock is up roughly 19.14% so far this year, has gained over 23% over the past three months, and has surged 121.91% over the past 52 weeks. Those gains reflect growing confidence that Alphabet is turning its AI investments into real business momentum.

The company’s challenge now is scale. Demand for Google Cloud, AI infrastructure, and Gemini-powered services continues to outpace available capacity. To keep up, Alphabet expects capex to rise this year, with spending projected to climb even higher in 2027. That’s staggering, but management clearly believes the opportunity justifies the investment.

Technically, the stock appears to be catching its breath after a powerful rally. The 14-day RSI has cooled to 49.10 after spending time in overbought territory earlier last month, suggesting much of the speculative enthusiasm has eased. Meanwhile, the MACD indicator has turned negative, with the MACD line crossing below the signal line and red histogram bars emerging, pointing to softer near-term momentum.

The recent pullback looks less like a collapse and more like a market pausing to digest both Alphabet’s huge run and the equally huge bill that comes with building the future of AI.

After its strong rally over the past year, Alphabet is no longer the obvious bargain it once was. On the surface, the stock looks a little expensive, trading at roughly 25.33 times forward adjusted earnings and 8.93 times sales. That has naturally made some investors wonder whether most of the good news is already priced in.

But valuation is only one side of the equation. The bigger question is what investors are getting for that price. Google Cloud is growing at an impressive clip, Search remains a cash-generating powerhouse, and AI is opening up new opportunities across the company’s ecosystem. Adding in Alphabet’s massive cash reserves and strong balance sheet, the company still has plenty of firepower to invest for the future.

Dividend is another piece of the puzzle that makes Alphabet stock a compelling buy now. The tech giant recently boosted its quarterly dividend by 5% to $0.22 per share, which is payable to the shareholders on June 15. This brings the annualized payout to $0.88 per share. The dividend yield may not grab headlines at a modest 0.24%, but with a forward payout ratio of just 6.4%, Alphabet has plenty of flexibility to keep raising that payout while continuing to invest heavily in growth.

A Closer Look at Alphabet’s Stellar Q1 Report

Alphabet started 2026 on a powerful note. It released first-quarter report for fiscal 2026 on April 29, delivering one of its strongest performances in years. Revenue climbed 22% year-over-year (YOY) to $109.9 billion, while EPS surged 82% annually to $5.11. Both top and bottom lines beat Wall Street’s projections.

What’s impressive is that Alphabet delivered those numbers while continuing to spend aggressively on AI. In fact, operating margins expanded to 36.1%, showing that the company is still finding ways to grow profits even as it pours billions into future projects.

Google Cloud was the standout performer. Revenue for the segment surged 63% YOY to $20 billion as businesses flocked to Google’s AI infrastructure, Gemini-powered services, cybersecurity tools, and data analytics offerings. Demand was so strong that Google Cloud’s backlog nearly doubled from the prior quarter to $462 billion. More than half of that backlog is expected to turn into revenue over the next two years, giving investors a clear view of the road ahead.

At the same time, Google’s bread-and-butter Search business continued to deliver. Search revenue rose 19% annually, helped by growing engagement with AI features such as AI Overviews and Gemini. The company said its Gemini models are now processing more than 16 billion tokens every minute through its API, a sign that adoption is accelerating rapidly across customers and developers.

Alphabet’s financial position remains enviable. The company ended the quarter with $126.8 billion in cash, cash equivalents, and marketable securities. Operating cash flow reached $45.8 billion, although heavy investments in AI infrastructure pushed capital expenditures to $35.7 billion, leaving free cash flow at $10.1 billion.

And Alphabet is not slowing down. Management raised its expected capital spending for the year to between $180 billion and $190 billion as it builds more AI infrastructure and integrates cybersecurity company Wiz into its ecosystem. While the Wiz acquisition may weigh slightly on Google Cloud margins in the near term, management appears focused on the much bigger prize, which is to capture a larger share of the rapidly expanding AI market.

Wall Street analysts tracking Alphabet see its earnings rising. For fiscal 2026, EPS is projected to rise about 32.1% YOY to $14.28, before growing by another 3.3% annually to $14.75 in fiscal 2027.

Why Alphabet Is Reaching for Fresh Capital

Alphabet’s fundraising plan did not come out of nowhere. The tech giant is in the middle of one of the biggest spending cycles in its history as it races to expand AI infrastructure. Management capex guidance for fiscal 2026 is roughly double of what it spent in fiscal 2025.

The reason is that demand keeps growing. Google Cloud is expanding rapidly, AI services are attracting more customers, and the company’s contract backlog has ballooned to record levels. Building enough data centers, servers, and computing capacity to keep up requires enormous amounts of capital.

Rather than relying entirely on debt, Alphabet is choosing to bring in fresh equity resources. The move provides long-term funding at a time when AI investments are soaking up cash across the tech sector and putting pressure on FCF.

A Powerful Endorsement from Berkshire

Berkshire Hathaway continues to deepen its commitment to Alphabet. The conglomerate had already more than tripled its Alphabet position during the first quarter of 2026, building the stake to roughly 58 million shares worth about $17 billion.

Under the planned fundraising, Berkshire agreed to buy another $10 billion of Alphabet stock, split evenly between Class A and Class C shares. If completed, that would make Berkshire one of Alphabet’s largest outside shareholders and give the company’s AI expansion plans a very visible endorsement.

The investment also offers an early look at how Berkshire is operating under Greg Abel’s leadership. Rather than sitting on the sidelines as AI spending accelerates, Berkshire appears willing to back one of the industry’s biggest players. For Alphabet, that kind of support sends a strong message that one of the world’s most respected long-term investors still sees substantial value despite the rising costs of the AI race.

What Do Analysts Expect for Alphabet Stock?

Wall Street was not exactly expecting Alphabet to announce a capital raise, and the news initially caught investors off guard. But while the market focused on the headline, analysts largely viewed the move through a different lens.

HSBC analyst Paul Rossington called the timing “unexpected,” especially since Alphabet had already tapped the bond market, scaled back buybacks, and signaled higher spending ahead. He trimmed his price target to $420 from $435 to reflect the higher share count from the planned stock offerings, but maintained a “Buy” rating. Importantly, Rossington did not change his underlying business forecasts and continues to see Alphabet as one of the companies best positioned to benefit from the AI boom.

Meanwhile, Wells Fargo’s Ken Gawrelski sees the capital raise as a statement of intent. In his view, Alphabet is signaling to investors, competitors, and suppliers that it plans to spend aggressively to maintain its lead in AI infrastructure. With Google Cloud demand surging and backlog over $460 billion, Gawrelski believes Alphabet may need significantly more computing capacity than previously expected. He argues the company is likely to keep exploring multiple funding options to capitalize on its custom TPU advantage and expanding AI opportunity. Wells Fargo maintains an “Overweight” rating and a $435 price target.

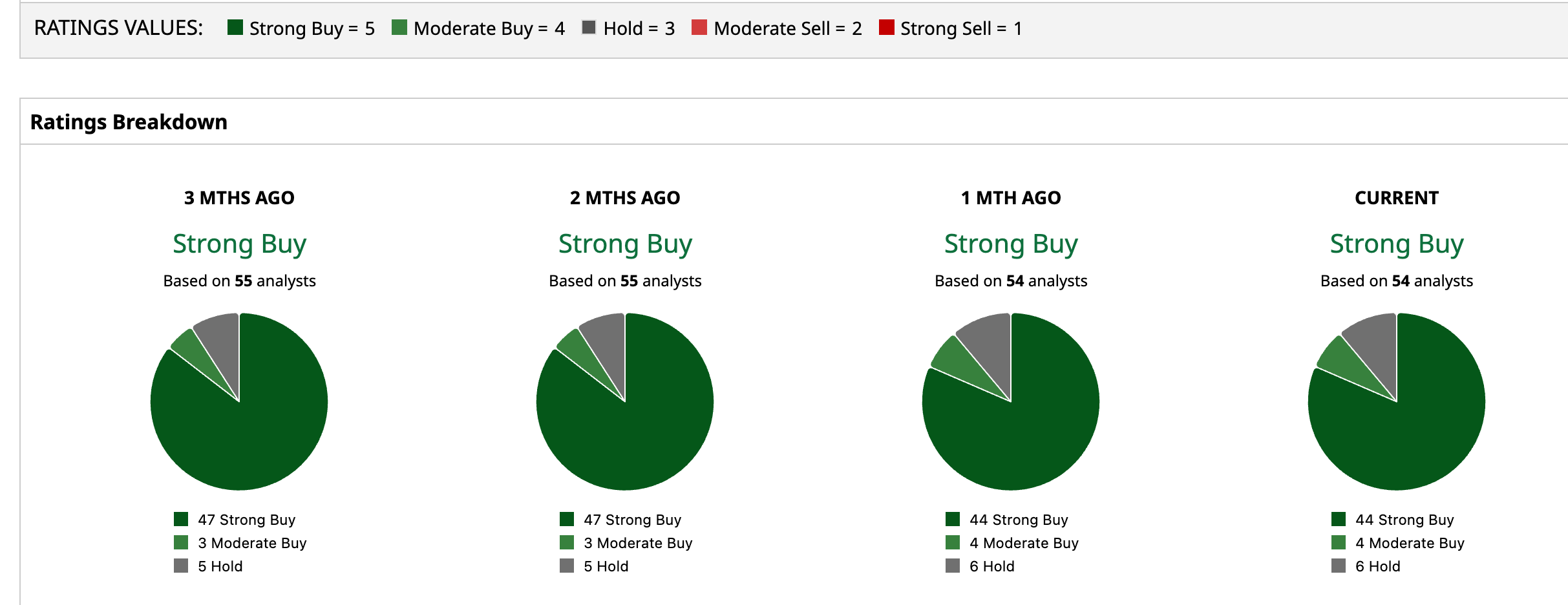

Analysts monitoring GOOGL are bullish, with a consensus rating of “Strong Buy” overall. Out of 54 analysts, 44 recommend a “Strong Buy,” four suggest a “Moderate Buy,” and six are playing it safe with a “Hold” rating. The average price target of $431.08 suggests a 15.65% upside potential from here. Meanwhile, the Street-high target of $515 suggests GOOGL stock could rise as much as 38.17%.

Conclusion

In many ways, Alphabet’s latest move could mark the beginning of a new chapter in the AI story. For years, investors have focused on the opportunities AI could create. Now, attention is shifting to the massive price tag required to capture those opportunities.

The share sale may create dilution, giving existing investors a slightly smaller ownership stake and raising the bar for future returns. But it also gives Alphabet additional firepower to keep expanding its AI infrastructure. Whether that proves to be a smart trade-off will depend on how effectively Google turns spending into growth. For now, Wall Street sees the costs. Berkshire Hathaway appears to be focused on the value and worth of those investments down the road.

On the date of publication, Sristi Suman Jayaswal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/NVIDIA%20Corp%20video%20chip-by%20Antonio%20Bordunovi%20via%20iStock.jpg)

/An%20Intel%20sign%20out%20front%20of%20a%20corporate%20office%20by%20wolterke%20via%20Adobe%20Stock.jpeg)

/A%20close-up%20of%20an%20AMD%20office%20by%20gehapromo%20via%20Adobe%20Stock.jpeg)