Like the cliff swallows annual springtime return to Capistrano, government announcements and headlines of New World Screwworm scares emerge in late May through early June.

The dynamics of US cattle markets continue to diverge, with funds showing little interest while fundamentals remain bullish short-term, intermediate-term, and long-term.

The US beef industry is vulnerable to a break, though, due to the outlook of continued higher fuel prices due to the US president's War on Iran.

Each spring, the cliff swallows return to Mission San Juan Capistrano in Southern California, an event dating back to the 18th century when it was first noted, inspiring poets, songwriters, and film makers over the centuries. Naturally, the good folks of Texas have taken note of this, and under the belief that anything the Golden State can do the Lone Star State can do better, now sound the alarm annually about the return of the New World Screwworm. Unfortunately, or maybe fortunately, this event has not driven the imagination of artists, though given the screwworms description of “flesh-eating”, I would expect a cheap horror movie to be made in the not-too-distant future and most likely funded by the current US administration to be shown in new ballroom.

Is the screwworm the threat official government release, and expanded upon by media, make it out to be? Let me start this part of the discussion by repeating something I’ve said for decades: Those who actually know the cattle industry – like my late associates John Harrington and Walt Hackney, as well as my good friend Kyle Bumsted – know immediately when analysts and commentators don’t know the industry. When the story broke last week of a calf in southern Texas found to have the screwworm (a second case was reported over the weekend just past), I asked Kyle about it and his response was classic, “So what?”. He went on to talk about treatment and containment solutions, but more importantly the fact it doesn’t change the big picture of real fundamentals.

This is where US cattle markets get interesting. Recall my Market Rule #6 says, “Fundamentals win in the end”. This rule has been challenged over the past couple years as algorithms have become more reliant on headlines while the commercial side of the various markets continue to indicate their view of supply and demand through cash price, basis, and futures spreads. With headlines being intentionally manipulated by those in power for financial gain, this has created a divergence in many markets – including both live and feeder cattle – between fund and fundamental positions. Keep in mind Market Rule #1 reminds us, “Don’t get crossways with the trend”, and Newton’s First Law of Motion applied to markets, “A trending market will stay in that trend until acted upon by an outside force”, with that outside force noncommercial activity.

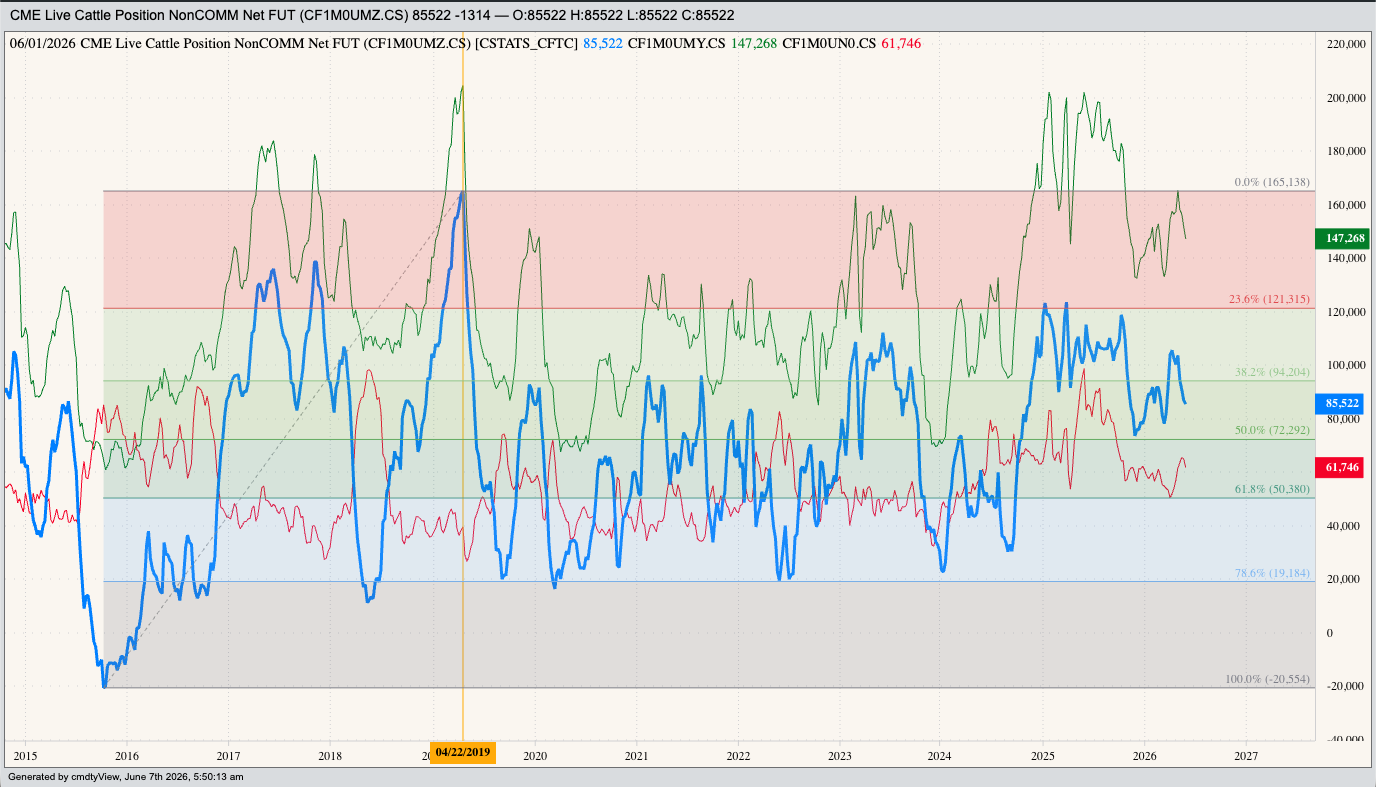

Given this, what has Watson (my name for the algorithm-driven noncommercial (fund) side of markets) been doing in live cattle? The latest Commitments of Traders report, for the week ending Tuesday, June 2, put the noncommercial net-long futures position at 85,522 contracts, a decrease of 1,314 contracts from the previous week. The long-term picture of fund positions is interesting given the range from the record net-short of 20,554 contracts (October 13, 2015) to the record net-long of 165,138 contracts (April 23, 2019). If we drop in standard Fibonacci retracement levels we see the 23.6% line at 121,315 contracts with the 78.6% line at 19,184 contracts and the 50% mark at 72,292 contracts. Since April 2019 the noncommercial net-futures position has generally stayed between the first two lines with activity since December 2025 moving the position within sight of the 50% line. In other words, Watson has largely been noncommittal toward live cattle outside of day-to-day histrionics.

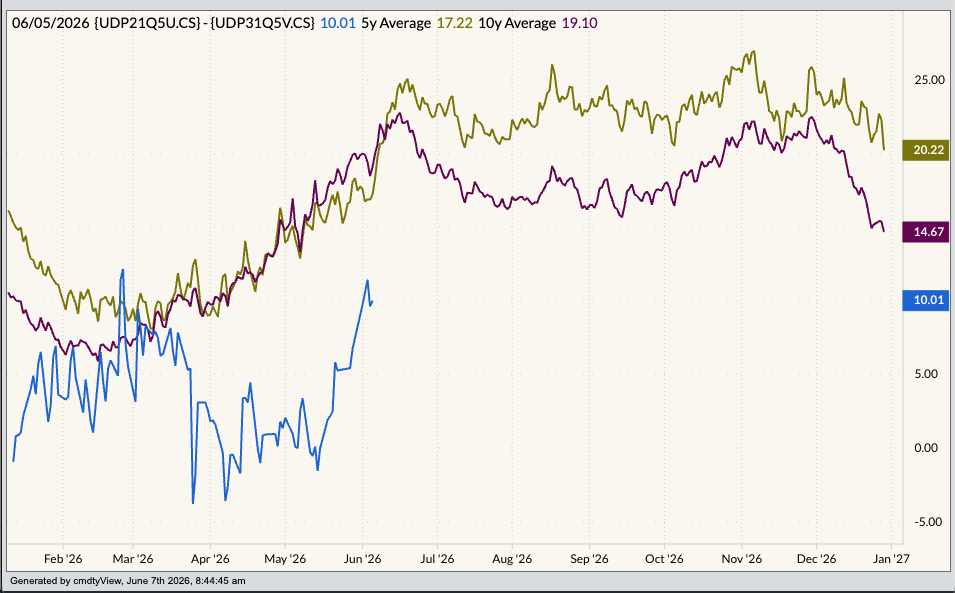

On the other hand, commercial interests haven’t changed their stance with the short-term, intermediate-term, and long-term view of supply and demand still bullish. The close of Friday, June 5 brought reported cash trade at $258 putting national average basis at nearly $8.00 over June futures (LEM26), a neutral-to-strong reading based on previous 5-year average ($3.825) and high ($11.775) weekly closes. Meanwhile, the August (LEQ26) -October ((LEV26) futures spread closed at $7.525 as compared to the previous 5-year high weekly close of $3.35, the October-December (LEZ26) settled at $0.45 (versus $0.575), and the Dec-February 2027 (LEG27) finished at (-$0.325) with the previous 5-year average at (-$3.45) and high of $1.20.

If we break this down to the two key factors – supply and demand – what do we know? According to USDA’s monthly Cattle on Feed reports, taken for what they are (government reports), we see the on-feed numbers have grown slightly during 2026 with the January 1 figure coming in at 11.45 million head (mh) and the May 1 figure up 1% to 11.58 mh. Meanwhile, USDA’s monthly Cold Storage reports showed a December 31, 2025 total beef number of 437.5 million pounds (mp) with the April 30, 2026 figure coming in at 408.3 mp. If we can believe the numbers – a question with ANY government report – then we see US consumer demand has not backed off due to the continued small US herd resulting in tighter supplies, despite increased imports, and higher prices.

Regarding the latter, the latest US boxed beef prices were reported (again by USDA, so, asterisk involved) at $392.70 (choice) and $382.69 (select). While both are still well off record highs established during the autumn of 2025, we can consider prices high. However, a look at the seasonal chart for the spread, select is stronger than normal in relation to boxed based on previous 5-year and 10-year averages. Why? My Blink reaction is US consumers are showing a preference for hamburger over steak, a sign of the economic times regardless of the somewhat questionable May employment number of 172,000 jobs (as compared to the expected 80,000).

As I’ve said over the past couple years, and highlighted since the US president went to war against Iran, US consumers will have to decide between beef and fuel at some point. And with fuel prices not expected to come down significantly any time soon – WTI crude oil, distillates (diesel fuel), and RBOB gasoline forward curves are all in backwardation (inverted) – the US beef market looks vulnerable. As for the screwworm hysteria, it will come and go, replaced with the next set of headlines or US administration announcements.

Until the flies return again next spring.

On the date of publication, Darin Newsom did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Renewable%20Energy%20by%20Yuri%20Hoya%20via%20Shutterstock.jpg)

/A%20close-up%20of%20a%20SpaceX%20sign%20by%20Sundry%20Photography%20via%20Adobe%20Stock.jpeg)