Selling short Occidental Petroleum (OXY) puts has worked for the last 2 months, as seen in my last 2 Barchart OXY articles. This is even though oil and OXY stock have been volatile, but mostly flat. It makes sense to play this again in the next month.

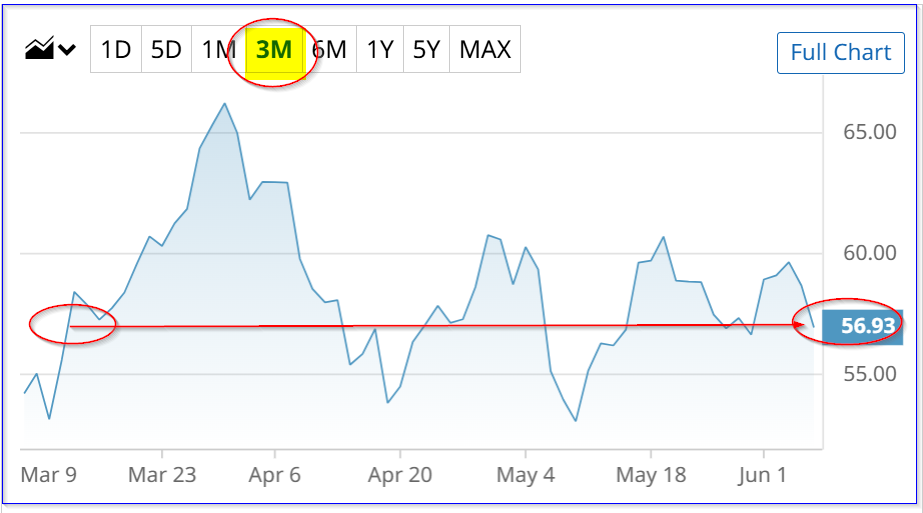

OXY closed at $56.93 on Friday, June 5, down from its recent highs, even as oil prices have been trending higher. The Barchart chart below shows that OXY has been mostly flat over the past three months.

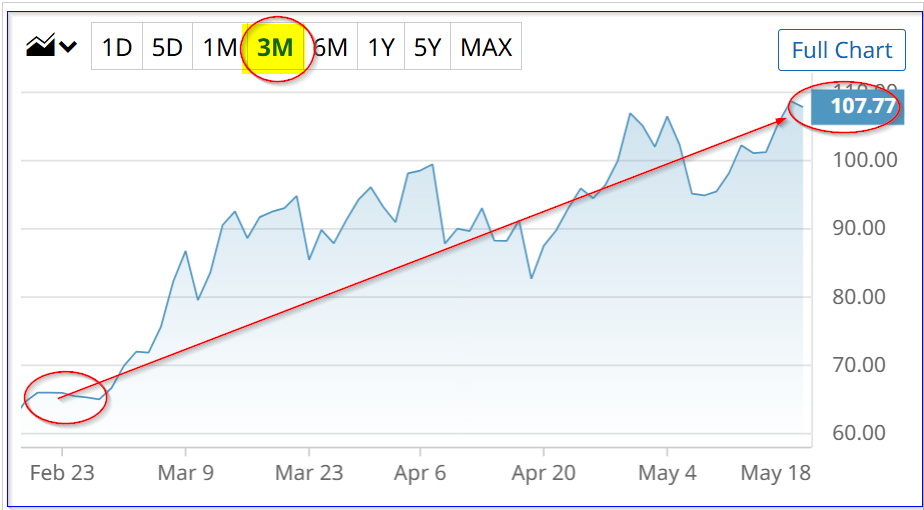

This is despite a continuous upward drift in crude oil futures, as evidenced by the WTI June 26 futures contract (CLM26), shown in the Barchart chart below. That might imply that OXY stock could be due for an upward turnaround.

That means this is ideal for short-sellers of out-of-the-money (OTM) OXY put options. They get to collect income shorting OTM OXY puts, without having to buy OXY stock.

The reason is that the below-market put options' strike prices are never exercised. The investor keeps the original income received from selling short the put.

How It's Worked Out - Shorting Out-of-the-Money (OTM) OXY Puts

You can see this in my last two Barchart articles, where I discussed shorting OXY puts. The first one was on April 20, “Occidental Petroleum Stock Is Off Its Peak - Time to Buy OXY or Short OTM Puts?”

For example, I discussed shorting the $50 OXY put expiring 34 days later on May 22, when OXY was 7% higher at $53.79. The premium was $0.97, so the short-put yield was 1.94% (i.e., $0.97/$50.00).

By May 15, when I wrote my next Barchart article on Occidental Petroleum, OXY was at $56.84. The 5/22/26 expiry put option premium had dropped to just 4 cents, almost worthless. That's exactly what a short-seller wants to see.

In the May 22 Barchart article, “Shorting OXY Puts Is Working - Especially if Oil Keeps Rising,” I discussed shorting the June 18 expiry $52.50 put option and the $55.00 put option.

These options were 3% and 7% out-of-the-money, as OXY was at $56.84. The premiums received were 88 cents and $1.17, respectively. That means the short-seller made an immediate income yield of 1.67% (i.e., $0.88/$52.50) and 3.109% ($1.71/$55.00), respectively. The average of these two yields (doing both put plays) was 2.41%.

Today, these premiums have fallen. For example, the June 18 expiry $52.50 put premium is down from $0.88 to $0.33 at the midpoint. The $55 put has dropped from $1.71 to 97 cents. There is now just one week left on this contract, and the put strike prices are still below OXY's trading price.

As a result, it might make sense for some investors who have done them to roll them over. In addition, new OXY short-put investors can look at shorting OTM puts expiring in 4 weeks.

Shorting New 1-Month OXY Puts

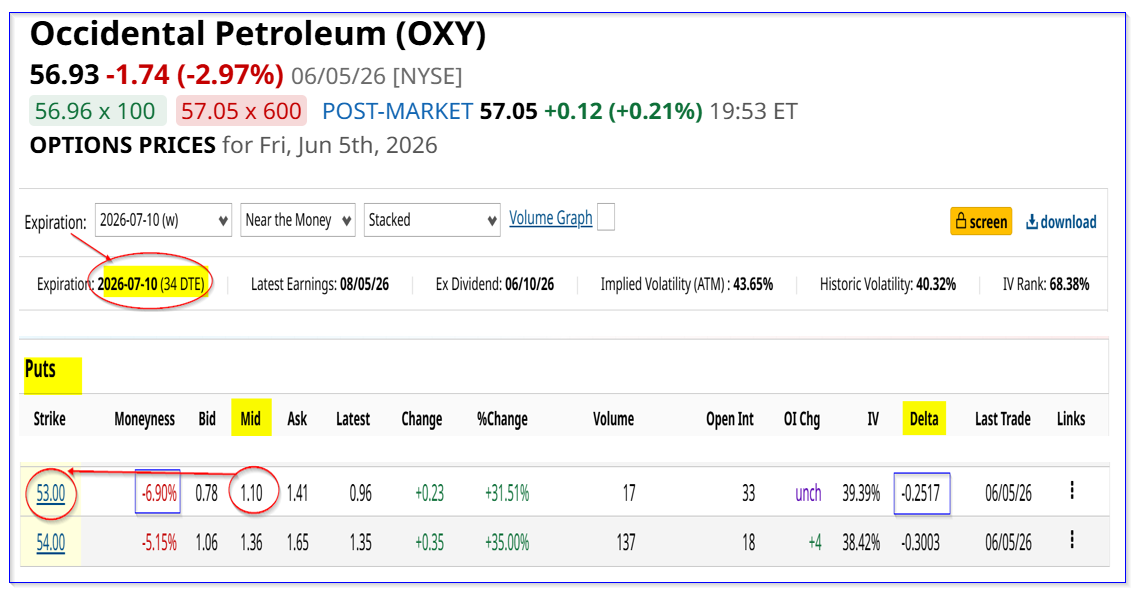

For example, the July 10 expiry OXY option chain, 34 days from now, shows that the $53.00 strike price is 6.9% below OXY's price of $56.93. The midpoint premium is $1.10, as can be seen in the Barchart table below.

This implies the short seller of this put contract earns a 1-month put yield of 2.075% (i.e., $1.10 / $53.00).

This means the investor first secures $5,300 with their brokerage firm in cash or buying power. Then the investor enters a trading order to “Sell to Open” 1 put contract at $53.00.

The $5,300 acts as collateral in case OXY falls to $53.00 and the put option buyer exercises their right to sell their shares at $53.00. That means the short-seller's account will be assigned to buy 100 shares at $53.00, or $5,300.

However, the short-seller's account will immediately receive $110. That is why their investment has an immediate yield of 2.075% (i.e., $110/$5,300).

Moreover, note that even if OXY drops to $53.00, the investor's net debit is only $5,190 (i.e., $5,300 - $110). So, they own OXY shares at a net cost of $51.90, or 8.84% below Friday's close of $56.93.

In addition, the delta ratio (as seen in the Barchart table above) is only 25%. That implies just a low chance for OXY to fall to $53.00 by July 10. This means the investor can make a 2.0% yield this month without too much worry that their account will be assigned to buy OXY.

Conclusion

An investor following these three Barchart articles on OXY will have made the following OTM short-put yields over the last 3 months: 1.94%, 2.41%, and 2.075%. This assumes that none of these contracts have been exercised (i.e., OXY fell to these below-market put strike prices).

So, the total expected return (ER) with this short-put play for the past 3 months is 6.425%. That is way better than buying OXY stock. For example, 3 months ago, on March 6, OXY closed at $54.19. That means a buy-and-hold OXY stock investor would have made a return of 5.06% (i.e., $56.93/$54.19), before any dividends. That's despite oil prices rising over this period.

Even with an investment at the March 5 price of $53.24, the return has been +6.93, slightly better. However, from April 20, when OXY was at $54.48, the return has been 4.50% ($56.93/$54.48-1). The first 2 short-put plays have returned 4.35%, before the July 10 expiry short-put yield of 2.075%.

In other words, it has made sense to short these out-of-the-money (OTM) OXY puts for similar returns. The difference is that the investor has a lower potential buy-in if OXY ever drops to the breakeven points.

On the date of publication, Mark R. Hake, CFA did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/An%20Intel%20sign%20out%20front%20of%20a%20corporate%20office%20by%20wolterke%20via%20Adobe%20Stock.jpeg)

/Alibaba%20by%20testing%20via%20Shutterstock.jpg)

/Alphabet%20(Google)%20Image%20by%20Markus%20Mainka%20via%20Shutterstock.jpg)