Construction firm Sterling Infrastructure (STRL) rallied 9.3% intraday on June 3, as investors turned their attention toward infrastructure firms tied to data center development. Sterling is primely positioned to benefit from artificial intelligence (AI) buildouts.

The company’s Q1 results showed clear signs of this. Sterling’s E-Infrastructure signed backlog rose 123% compared to the prior year's first quarter. Mission-critical projects such as data centers, manufacturing, and semiconductor facilities accounted for more than 90% of the E-Infrastructure backlog at quarter's end. It is also actively constructing on two data center campuses.

About Sterling Infrastructure’s Stock

Sterling Infrastructure is a leading heavy civil construction company that builds, repairs, and reconstructs critical infrastructure across the U.S. The company operates through three main segments: E-Infrastructure Solutions, which provides electrical and telecommunications infrastructure for data centers and energy facilities; Transportation Solutions, covering highways, roads, bridges, airfields, ports, and light rail projects; and Building Solutions, delivering commercial and industrial construction services.

Sterling primarily serves state departments of transportation, transit authorities, airport authorities, port authorities, and private developers. Headquartered in The Woodlands, Texas, the company operates in multiple regions nationwide, delivering complex infrastructure projects that enable economic growth and modernization. It has a market capitalization of $29.37 billion.

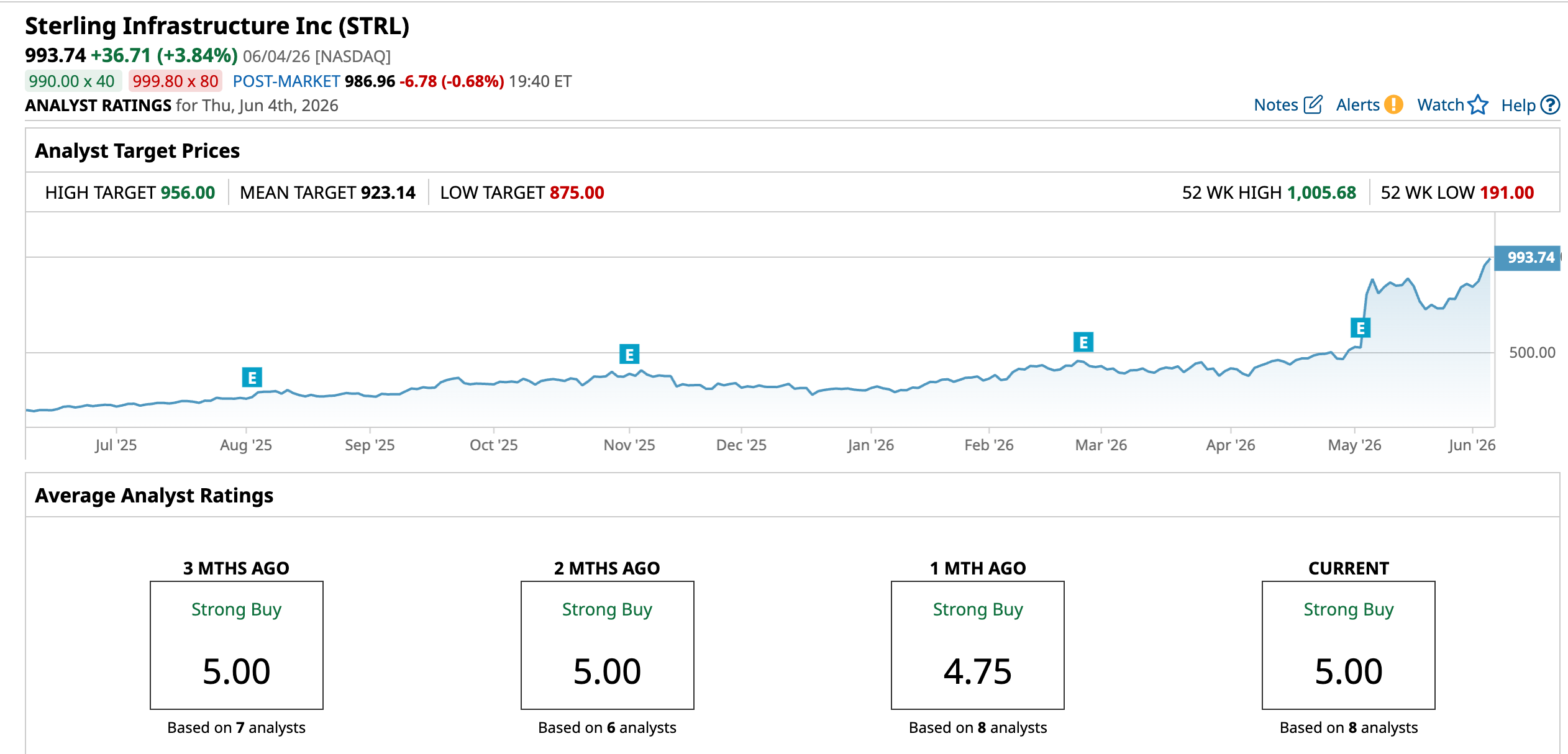

The company benefits from surging demand for data center and semiconductor infrastructure as AI adoption accelerates, with E-Infrastructure revenue jumping and over a significant portion of its backlog tied to mission-critical projects. Over the past 52 weeks, Sterling’s stock has gained 412.74%, while it has been up 224.5% year-to-date (YTD). It reached an all-time intraday high of $1,005.68 on June 4, but is down a marginal 1.2% from that level.

On a forward-adjusted basis, Sterling’s price-to-earnings (non-GAAP) ratio of 51.06 times is significantly higher than the industry average of 19.97 times.

Sterling Infrastructure Crushed Q1 on Data Center Boom

Sterling reported solid results for the first quarter of fiscal 2026, driven by a solid boom in its E-infrastructure segment. The company’s revenue increased by 91.6% year-over-year (YOY) to $825.68 million, considerably higher than the $585.40 million expected by Wall Street analysts. In fact, its E-infrastructure solutions revenue was $597.73 million for the quarter, up 173.9% from the prior-year period. Sterling’s adjusted EPS grew from $1.63 in Q1 2025 to $3.59 in Q1 2026, surpassing the $2.29 EPS that analysts had expected.

The company’s visibility into future revenue also caught investors' attention. By the end of the first quarter, Sterling had a signed backlog of $3.80 billion, up 78%, and a combined backlog of $5.15 billion, up 131%. Moreover, its combined backlog book-to-burn ratio of 3.5x indicates strong demand. The company’s signed backlog, unsigned awards, and future phase opportunities indicate a total addressable work pool of nearly $6.50 billion, up roughly $2 billion from the end of 2025.

Wall Street analysts are robustly optimistic about Sterling’s future earnings. For the current fiscal year, EPS is projected to surge 75.7% annually to $18.03, followed by a 23.1% growth to $22.20 in the next fiscal year. Moreover, analysts expect the company’s EPS to grow by 76.5% YOY to $4.50 for the second quarter of fiscal 2026.

What Analysts Think About Sterling Infrastructure’s Stock

Recently, analysts at KeyBanc raised Sterling’s price target from $889 to $922, while keeping a bullish “Overweight” rating on the stock. Analysts at the firm believe that Sterling has positioned itself as the industry leader in site preparation by leveraging its heavy civil and transportation expertise and resources, and is now developing downstream capabilities through a focused MEP expansion strategy. Demand trends from Sterling Infra also indicate site-preparation activities for larger multi-data-center build-out campuses.

Last month, analysts at Oppenheimer initiated coverage of Sterling with an “Outperform” rating and a $950 price target. As the company expands its services from civil services and site development into inside electrical construction, Oppenheimer analysts believe that the company’s ability to mobilize traditional services to where customers are developing is a critical milestone.

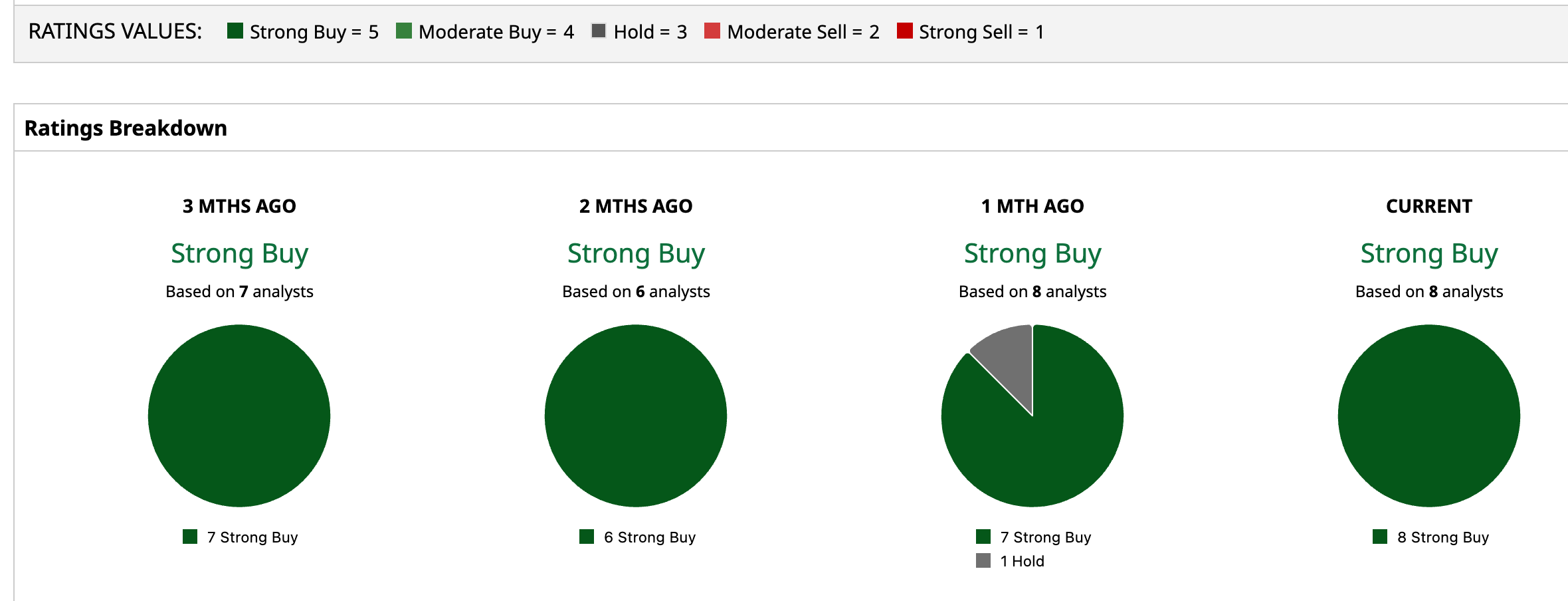

Sterling Infrastructure is gaining much praise on Wall Street, with analysts awarding it a consensus “Strong Buy” rating overall. Eight analysts rating the stock have given it a “Strong Buy” rating. However, the consensus price target of $923.14 represents a 7.1% downside from current levels.

On the date of publication, Anushka Dutta did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20close-up%20of%20the%20Broadcom%20logo%20on%20a%20smartphone%20by%20Timon%20via%20Adobe%20Stock.jpeg)

/An%20Intel%20sign%20out%20front%20of%20a%20corporate%20office%20by%20wolterke%20via%20Adobe%20Stock.jpeg)