/An%20image%20of%20the%20Snowflake%20logo%20on%20a%20corporate%20office_%20Image%20by%20Grand%20Warszawski%20via%20Shutterstock_.jpg)

Snowflake (SNOW) is a stock investors should pay attention to right now. After years of promise, the company's artificial intelligence (AI) strategy has finally hit an inflection point. Product revenue grew 34% year-over-year (YOY) to $1.33 billion in the first quarter of fiscal 2027, beating the consensus estimate of $1.32 billion, while adjusted EPS came in at $0.39 against Wall Street's estimate of $0.32.

The tech stock surged more than 40% between May 28 and June 1. Currently, Snowflake has a market capitalization of $83.4 billion. The ongoing rally in SNOW stock is a sign that Snowflake is becoming a compounding AI story, creating a rare window for long-term investors.

Why Snowflake's AI Momentum Is the Real Deal

Two products are driving the inflection: Snowflake Intelligence and Cortex Code, known internally as "CoCo."

Snowflake Intelligence gives business users a natural language way to query and analyze enterprise data, while CoCo is a general-purpose coding agent built specifically for data and AI workflows.

CoCo launched in February 2026, and more than 7,100 customer accounts adopted the product by the end of fiscal Q1. Notably, accounts using Snowflake Intelligence more than doubled quarter-over-quarter as well. "AI is compounding Snowflake's advantage in data," said CEO Sridhar Ramaswamy on the earnings call.

Customers using CoCo are building pipelines, migrating legacy workloads, and deploying AI agents at dramatically faster speeds. One partner, Infinite Lambda, used CoCo to build a full Customer 360 application in just five hours before a major pitch.

CFO Brian Robins added on the call that CoCo delivered a "step function change" in AI revenue potential and represented the largest single driver to the company's upward guidance revision.

The $6 Billion Amazon Deal Changes the Growth Picture

According to reports, Snowflake's partnership with Amazon (AMZN) has also expanded significantly. Specifically, Snowflake has signed a new five-year, $6 billion agreement with AWS. Under the new arrangement, Snowflake will expand its use of Amazon's Graviton chips along with cloud-based GPUs for AI workloads.

As AI shifts from simple chatbots to task-oriented agentic applications, this deal reflects how computing demands are changing. While graphics processing units are great for training AI models, agentic AI needs powerful general-purpose processors to move large amounts of data across workflows.

Amazon CEO Andy Jassy said on his company's most recent earnings call that Graviton allows companies like Meta (META) “to run the CPU-intensive workloads behind agentic AI with the performance and efficiency they need.” Meta (META) has also committed to hundreds of thousands of Graviton chips.

For Snowflake, the deal is a go-to-market win, given that AWS aims to expand investment and collaboration as part of the agreement. The partnership is already delivering; Snowflake has surpassed $7 billion in lifetime AWS Marketplace sales. The AWS deal was also fully incorporated into Snowflake's guidance raise for the year.

Snowflake's Natoma Acquisition Extends the Agentic Platform

Snowflake has also announced plans to acquire AI startup Natoma for an undisclosed sum. Natoma connects enterprise applications such as email, calendars, and project management tools to Snowflake's AI environment. Basically, Snowflake Intelligence and CoCo users will soon be able to send emails, check calendars, open tickets, and act across SaaS tools, all without leaving Snowflake's governed platform.

Rather than letting AI agents run loose across enterprise systems, Snowflake is building a control layer where every action is subject to security policies, permissions, and audit trails. Natoma brings everyday business applications into that controlled environment.

Ramaswamy described the opportunity bluntly: "The important point is not just convenience, it is control."

The Numbers Make the Bull Case Hard to Ignore

Beyond the headline beat, several metrics stood out for Snowflake in the quarterly report.

The net revenue retention rate climbed to 126%, for example, meaning existing customers are spending significantly more over time. Net new customer additions also rose 38% YOY to 616. The number of customers spending more than $1 million on a trailing 12-month basis reached 79, with 46 crossing that threshold in the quarter compared to just 26 a year earlier. What's more, Snowflake now has 64 customers spending more than $10 million on a trailing 12-month basis.

Management also raised full-year product revenue guidance to $5.84 billion, representing 31% growth. The company lifted non-GAAP operating margin guidance from 12.5% to 13.5% as well.

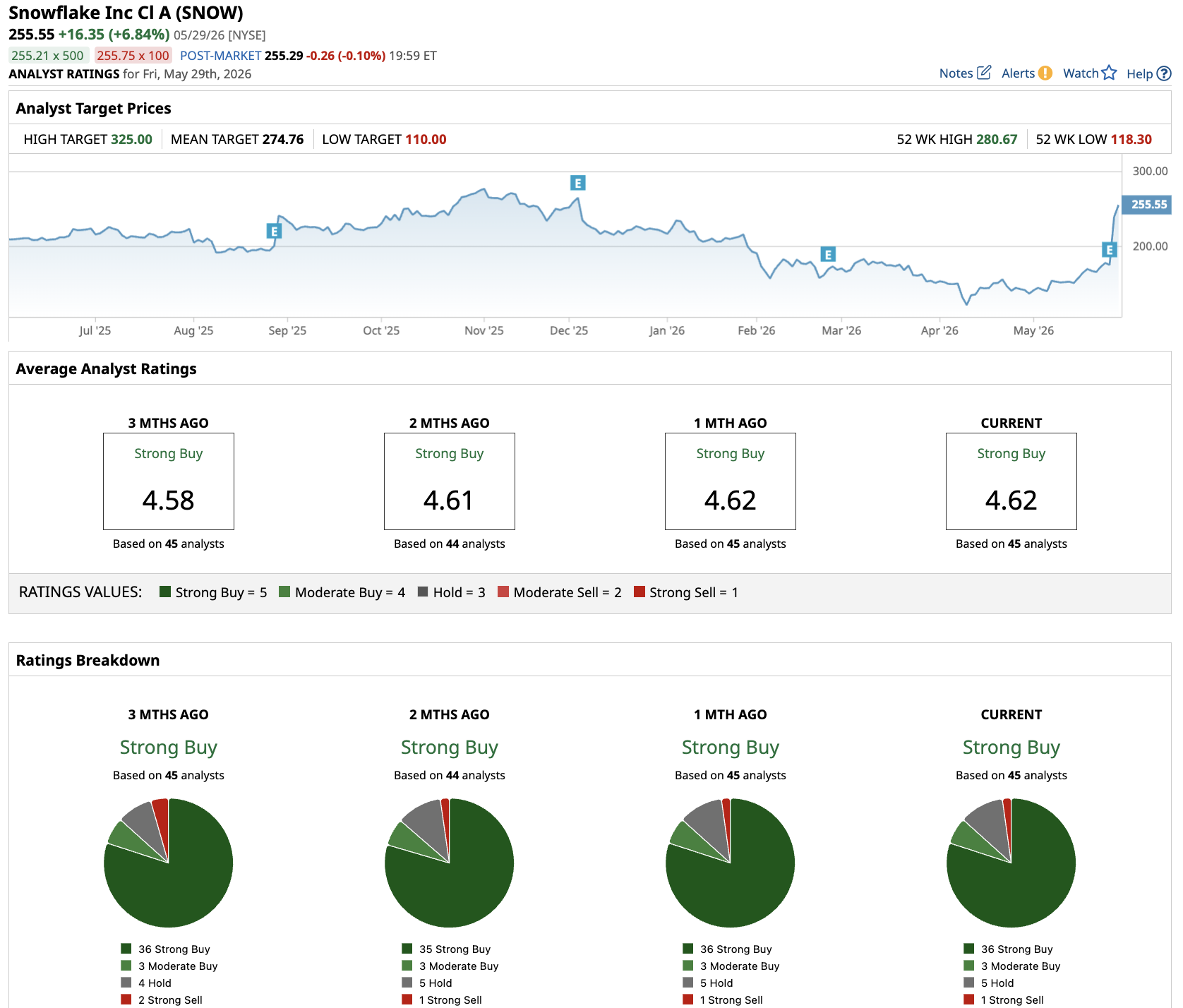

What Do Analysts Think of Snowflake Stock?

Out of the 45 analysts covering SNOW stock, 36 recommend a “Strong Buy” rating, three recommend a “Moderate Buy,” five recommend a “Hold,” and one analyst recommends a “Strong Sell.” The average price target of $281.84 represents potential upside of 15% from current levels.

All told, Snowflake is a company where AI is accelerating every part of the business, from migrations to new workload creation to internal productivity. The combination of an accelerating core platform, two fast-growing AI products, a transformative AWS partnership, and a smart acquisition makes Snowflake one of the more attractive data infrastructure names heading into the back half of 2026.

For investors who believe enterprise AI spending is still in its early stages, SNOW stock deserves a close look.

On the date of publication, Aditya Raghunath did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20close-up%20of%20a%20General%20Motors%20corporate%20sign%20by%20lindaparton%20via%20Adobe%20Stock.jpeg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Zoetis%20sign%20at%20their%20Canadian%20By%20JHVEPhoto.jpeg)

/Microsoft%20headquarters%20By%20Peter.jpeg)

/A%20SoFi%20logo%20on%20an%20office%20building%20by%20Tada%20Images%20via%20Shutterstock.jpg)