/Capital%20One%20Financial%20Corp_%20bank%20exterior-by%20Brett_Hondow%20via%20iStock.jpg)

Based in McLean, Virginia, Capital One Financial Corporation (COF) is a bank holding company best known for its nationwide credit card franchise. Beyond cards, the company offers a broad suite of banking, lending, payments, and financial services, with operations spanning consumer finance, commercial real estate lending, corporate banking, and cash management.

With a market cap of approximately $114.4 billion, Capital One belongs in the large-cap category, an elite group reserved for companies valued at more than $10 billion. Despite its size and diversified business model, the stock has struggled to gain traction.

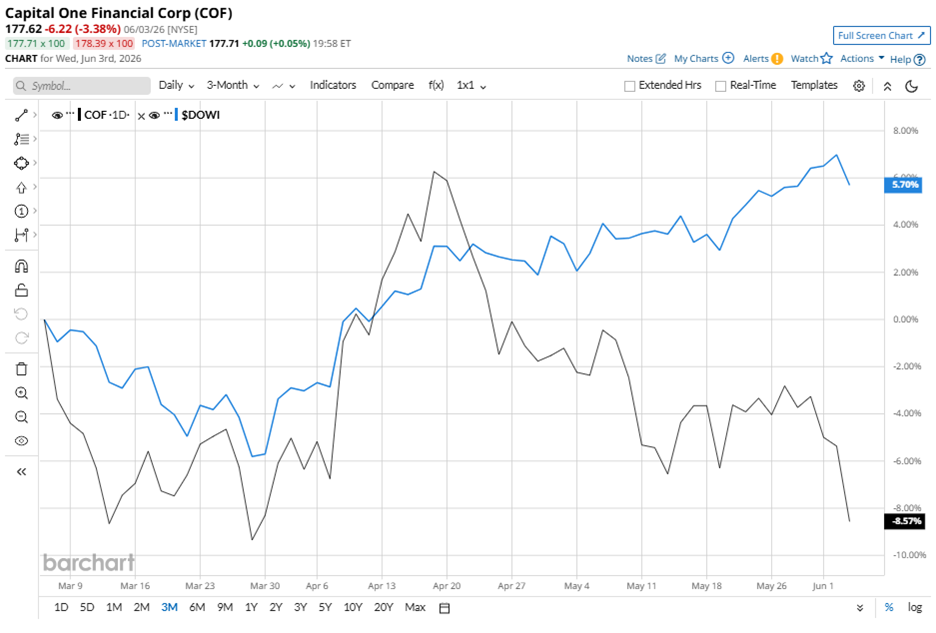

COF stock is currently trading 31.6% below its 52-week high of $259.64 reached in January. Over the past three months alone, the stock has fallen 8.3%. During the same period, the Dow Jones Industrial Average ($DOWI) gained 4.5%, widening the performance gap and underscoring Capital One’s recent underperformance against the broader market.

The contrast becomes even more pronounced when viewed through a longer lens. Over the past 52 weeks, COF stock has declined 9.2%, while the Dow advanced 19.2%. The divergence continues into 2026 as Capital One’s shares are down 26.7% year-to-date (YTD), while the index has climbed 5.5%.

The technical picture reflects the weakness. COF stock has been trading below its 50-day moving average of $189.37 since May, signaling that near-term momentum remains under pressure. The stock has also stayed below its 200-day moving average of $211.44 since Mid-February, indicating that the longer-term trend has yet to regain its footing.

Investor concerns became more apparent on Tuesday, Apr. 21, when Capital One reported its Q1 FY2026 results, owing to which the stock slipped 1.6% that day. Revenue surged 52.3% year over year to $15.2 billion, a strong increase on paper, but the figure still missed Wall Street forecasts of $15.4 billion.

Adjusted EPS grew 8.9% from the year-ago value to $4.42, which also failed to meet analyst estimates of $4.57. Despite the miss, the results revealed several underlying growth drivers. Management credited the addition of Discover’s business, higher purchase volumes, and expanding loan balances for helping lift performance.

However, those gains did not fully offset temporary headwinds from Discover’s earlier credit policy cutbacks, which continue to weigh on card growth. As Capital One works through those challenges, management remains focused on the next phase of growth.

The company plans to reach key integration milestones related to Discover and Brex, increase investments in marketing and technology, and further expand its digital-first banking and payments ecosystem to strengthen its long-term competitive position.

For additional context, Capital One’s rival American Express Company (AXP) has held up considerably better during the market's recent turbulence. Its shares declined only 1.1% over the past 52 weeks and are down 18.8% YTD, making Capital One’s losses look substantially steeper by comparison.

Even so, Wall Street has not abandoned the stock. Among the 23 analysts covering Capital One, the overall rating remains a “Strong Buy,” indicating that many still believe the market might be overlooking the company's longer-term earnings potential.

The optimism also shows up in the average analyst price target of $255.54, which points to potential upside of 43.9% from current levels, given Capital One can successfully execute its integration strategy and convert its growth initiatives into stronger financial results.

On the date of publication, Aanchal Sugandh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Amazon_com%20Inc_%20%20package%20by%20-%20AdrianHancu%20via%20iStock.jpg)

/Salesforce%20Inc%20HQ%20building-by%20JHVEPhoto%20via%20Shutterstock.jpg)

/Dell%20Technologies%20by%20Poetra_RH%20via%20Shutterstock.jpg)

/Intel%20Corp_%20Santa%20Clara%20campus-by%20jejim%20via%20Shutterstock.jpg)